Running a business often feels like juggling flaming torches; there’s always something that needs funding, whether it’s paying suppliers, upgrading equipment, or seizing a growth opportunity. For many entrepreneurs in India, the challenge isn’t just earning revenue; it’s finding the right kind of financial support at the right time.

Picking the wrong loan can lead to high interest, rigid repayments, or even unnecessary stress, turning what should be a growth opportunity into a financial headache. The key is understanding your options so you can make decisions that actually help your business thrive.

In this blog, we’ll break down the main types of business loans available in India, how each works, and when to use them. By the end, you’ll know exactly which loan suits your needs, helping your business stay flexible, funded, and ready to grow.

TL;DR

- Discover the 8 types of business loans in India and what each is best for, from short-term cash flow to long-term growth.

- Working capital loans, overdrafts, and invoice discounting help businesses manage daily operations without cash crunches.

- Term loans and equipment finance enable expansion and investment in machinery or infrastructure.

- Letters of credit and government-backed schemes offer safer, structured ways to handle trade and funding support.

- POS loans and merchant cash advances provide instant, flexible funds tied to sales, keeping your business agile.

Understanding the Different Types of Business Loans

Business loans are financial tools designed to meet the specific needs of a business, whether it’s keeping operations running smoothly, investing in growth, or handling unexpected expenses. They are not just about borrowing money; they are about choosing the right support at the right time.

Think of them as “financial instruments with purpose”. Each loan type has its own rules, benefits, and ideal use case, so understanding the differences can help you avoid unnecessary costs and make smarter financial decisions.

For example, a startup looking to buy new machinery might choose an equipment loan, while a retailer managing monthly supplier payments might benefit more from a working capital loan. Choosing the right loan ensures your business gets the funding it needs without creating financial strain.

It’s not just about access to funds; it’s about making borrowing work strategically to support your business goals.

Why Knowing the Right Business Loan Matters?

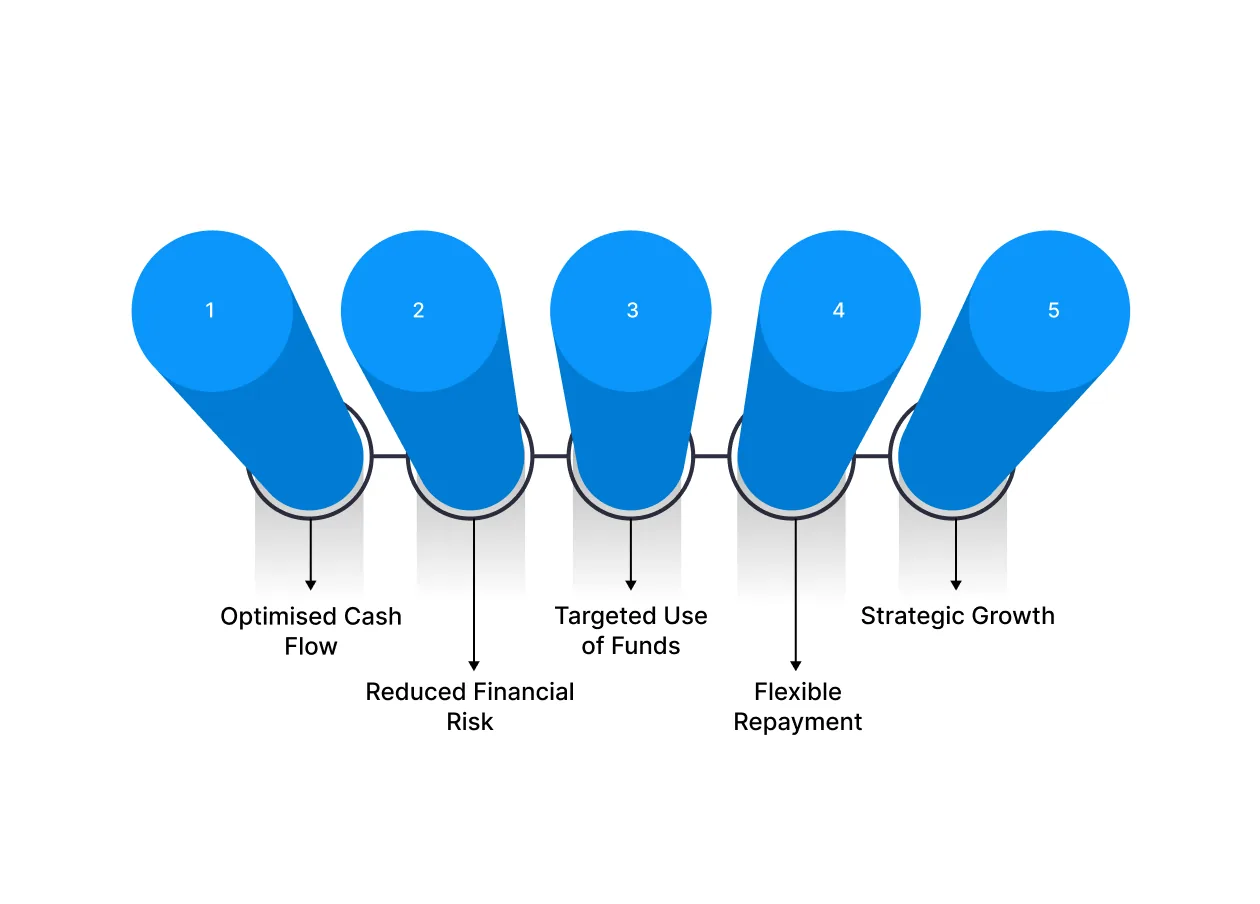

Choosing the right business loan can significantly influence your company’s growth and financial health. Here’s why it matters:

- Optimised Cash Flow: Selecting a loan that matches your business needs ensures you have funds available when required without straining daily operations.

- Reduced Financial Risk: The wrong loan can lead to high-interest costs, missed payments, or repayment stress. Picking the right type minimises financial strain.

- Targeted Use of Funds: Different loans are designed for specific purposes, such as equipment purchase, working capital, or expansion. Using the correct loan ensures funds serve their intended goal.

- Flexible Repayment: Some loans, like overdrafts or working capital loans, adjust to your cash flow. Knowing your options allows for repayment plans that suit your business cycle.

- Strategic Growth: Understanding which loans support short-term needs versus long-term growth helps you plan investments and scaling effectively.

By knowing your options, you’re not just borrowing money; you’re borrowing smartly to strengthen your business foundation.

8 Types of Business Loans in India You Should Know

Understanding the different types of business loans helps you choose one that aligns with your financial needs, repayment capacity, and business goals. Here’s a detailed breakdown:

1. Working Capital Loan

A working capital loan provides businesses with short-term funds to manage everyday operations such as payroll, rent, and inventory purchases. It helps maintain smooth cash flow, especially during periods when revenue is uneven or delayed. Interest is generally charged only on the amount borrowed, making it a flexible option for businesses with immediate liquidity needs.

For example, a small retailer experiencing slower sales during the off-season could use a working capital loan to pay suppliers and cover salaries, then repay the loan once sales pick up.

2. Term Loan (Short & Long-term)

A term loan is a structured loan with a fixed repayment schedule over a specified period. Short-term loans typically last up to one year, while long-term loans can extend from 5 to 10 years. These loans are best suited for funding capital expenditures, expansion projects, or larger investments.

For example, a manufacturing company may take a 5-year term loan to purchase new machinery for scaling up production and improving efficiency.

3. Letter of Credit (LC)

A Letter of Credit is a bank guarantee that ensures payment to suppliers once agreed-upon conditions are met. LCs are widely used in domestic and international trade to reduce payment risk and build trust between buyers and sellers.

For example, an exporter might use a letter of credit to guarantee payment to an overseas supplier while waiting for shipment and customs clearance.

4. Bill/Invoice Discounting

Invoice discounting allows businesses to access cash immediately by selling unpaid invoices to a lender at a discount. This improves liquidity without waiting for clients to settle payments, making it useful for companies with long payment cycles.

For example, a B2B service provider with 60-day invoices could use invoice discounting to access funds instantly and manage operational expenses without disruption.

5. Overdraft Facility

An overdraft facility gives a pre-approved credit limit linked to your current account. Businesses can withdraw funds up to the limit as needed, and interest is only charged on the amount used. This provides flexibility for short-term cash flow fluctuations.

For example, a restaurant may use an overdraft to cover additional inventory purchases during festive seasons and repay it as revenue comes in.

6. Equipment Finance or Machinery Loan

Equipment finance loans help businesses acquire machinery, vehicles, or technology equipment without putting pressure on cash reserves. Typically, the purchased equipment acts as collateral, and repayments are spread over a fixed tenure.

For example, a logistics company might buy delivery vans through an equipment finance loan, repaying the principal and interest over three years while immediately increasing delivery capacity.

7. Loans under Government Schemes

Government-backed schemes like MUDRA, CGTMSE, and Stand-Up India provide accessible credit with lower interest rates and simpler approval processes for MSMEs, startups, and women entrepreneurs.

For example, a handicraft startup could secure a MUDRA loan to expand production capacity and hire additional staff without high collateral requirements.

8. POS Loans / Merchant Cash Advance

POS loans, or merchant cash advances, provide short-term financing based on daily card sales through a POS terminal. Repayment is linked directly to sales, offering a flexible way for small retailers to access funds quickly.

For example, a café might take a POS loan to purchase a new coffee machine, repaying the loan gradually as daily card transactions occur.

Each loan serves a distinct purpose. Choosing the right type ensures you meet immediate needs, maintain smooth operations, and plan for sustainable growth.

Also Read: Simple Money Management Tips for Personal Finances

How to Choose the Right Business Loan: A Step-by-Step Guide

Choosing the right business loan is critical to ensure your funds are used effectively and repayments stay manageable.

Follow these steps:

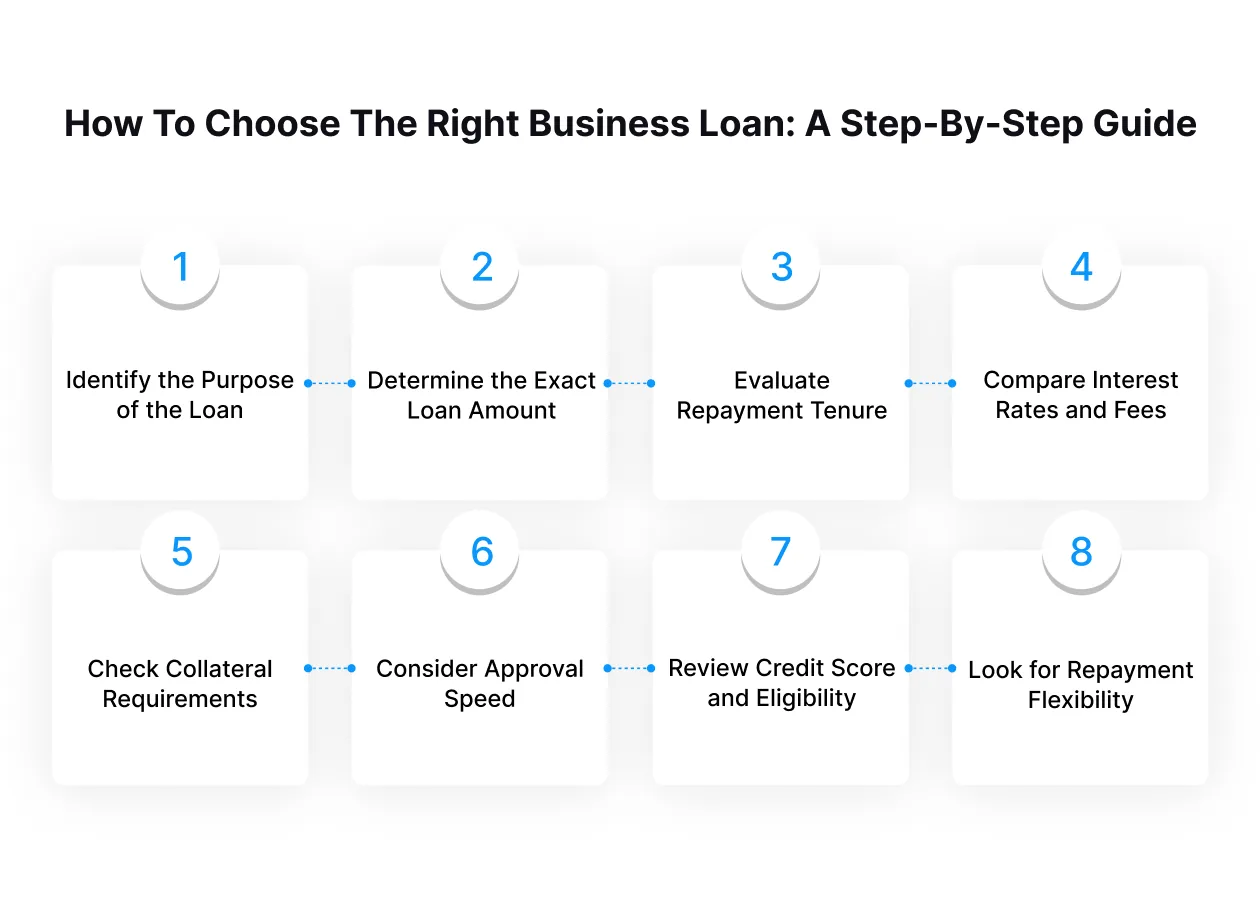

Step 1: Identify the Purpose of the Loan

Decide whether the loan is for working capital, expansion, equipment purchase, or trade financing. Picking a loan aligned with your needs ensures your funds are used efficiently.

Example: A retailer needing to stock up for the festive season may opt for a working capital loan, while a manufacturer buying new machinery would consider equipment finance.

Step 2: Determine the Exact Loan Amount

Calculate how much money you truly need. Borrowing too much increases interest costs, while borrowing too little may leave your business underfunded.

Example: If your expansion project costs ₹10 lakh, taking a ₹15 lakh loan could lead to unnecessary interest payments.

Step 3: Evaluate Repayment Tenure

Check the options for short-term versus long-term repayment. Choose a tenure that balances manageable EMIs with your business cash flow.

Example: A seasonal business may prefer a short-term loan of 6 months to cover festival inventory, while a startup buying expensive machinery may opt for a 5-year term loan.

Step 4: Compare Interest Rates and Fees

Look at interest rates, processing charges, and prepayment penalties. This helps you minimise borrowing costs and avoid hidden fees.

Example: Two lenders may offer ₹5 lakh term loans: one at 12% interest with 2% processing fees, the other at 14% but with no prepayment charges. Choosing wisely can save tens of thousands annually.

Step 5: Check Collateral Requirements

Understand whether the loan is secured or unsecured. This affects eligibility and the risk to your business or personal assets.

Example: A small business without property might choose an unsecured POS loan, whereas a company with land assets may opt for a secured term loan at a lower interest rate.

Step 6: Consider Approval Speed

Some loans disburse quickly while others take weeks. For urgent financial needs, fast approval can be a deciding factor.

Example: A café needing funds to repair kitchen equipment might choose a POS loan or merchant cash advance, which can be approved within 24 hours.

Step 7: Review Credit Score and Eligibility

Your personal and business credit scores influence interest rates and approval chances. Ensure you meet the lender’s criteria before applying.

Example: A startup with limited credit history may struggle to get a bank overdraft but can access funds via government-backed schemes designed for new businesses.

Step 8: Look for Repayment Flexibility

Check if the loan allows prepayment, partial payment, or revolving credit. Flexibility helps you manage cash flow and reduce long-term financial pressure.

Example: A manufacturer with fluctuating revenue may choose a business line of credit that allows borrowing and repayment as needed, avoiding fixed EMIs during lean months.

Also Read: How to Manage Monthly Expenses Smartly in 2025

Common Mistakes to Avoid When Taking Business Loans

Even experienced business owners sometimes make simple mistakes when choosing or managing loans. Avoiding these pitfalls ensures your borrowing supports growth instead of creating financial stress.

1. Borrowing More Than Needed

Risk: Taking more funds than required increases interest costs and ties up capital that could be used elsewhere. Excess borrowing can lead to unnecessary financial stress.

Mitigation: Assess your working capital and project expenses carefully. Only borrow what’s essential for operations, growth, or specific projects.

2. Ignoring Hidden Fees and Charges

Risk: Many loans come with processing fees, prepayment penalties, or insurance costs that inflate the total repayment. Overlooking these can make a seemingly affordable loan expensive.

Mitigation: Review the loan agreement thoroughly and request a complete breakdown of all fees. Factor them into your total cost calculations before committing.

3. Choosing Inflexible Repayment Terms

Risk: Fixed EMIs or short repayment periods can strain cash flow, especially for seasonal or variable-income businesses. Missing payments can trigger penalties or affect your credit score.

Mitigation: Look for loans with flexible repayment options, such as step-up EMIs or grace periods, that align with your cash inflows.

4. Not Comparing Lenders or Loan Options

Risk: Going with the first available lender may result in higher interest rates, slower approval, or less favourable terms. This can limit your financial flexibility.

Mitigation: Compare multiple lenders, considering interest rates, repayment flexibility, collateral requirements, and processing timelines to choose the most suitable option.

5. Failing to Plan for Repayment

Risk: Without a clear repayment plan, businesses risk default, mounting debt, and damage to their creditworthiness. Unexpected expenses can derail repayment if not anticipated.

Mitigation: Develop a detailed repayment schedule based on projected cash flow. Include a buffer for emergencies and operational fluctuations to stay on track.

How Pocketly Supports Your Credit Management

Managing credit effectively requires planning, but unexpected expenses or cash gaps can still disrupt even the best strategies. Pocketly provides short-term credit support that complements your proactive credit management, helping you stay on track without compromising your financial health.

Here’s how Pocketly helps:

- Flexible short-term loans: Access amounts from ₹1,000 to ₹25,000 when urgent needs arise. Whether it’s an unexpected medical bill, emergency repair, or sudden business expense, Pocketly ensures you have the cash to handle it without stress.

- Fast digital access: Quick KYC verification and instant approval mean you can get funds in minutes. No more long queues or paperwork; apply and receive funds directly through the app.

- Transparent terms: Interest rates start around 2% per month, with clear processing fees. Pocketly provides upfront information, so you know exactly what to expect, avoiding hidden costs or surprises.

- Prevent missed payments: Cover EMIs, credit card dues, or other urgent obligations on time. Avoiding missed payments protects your credit score and maintains your financial credibility.

Download the Pocketly app to access short-term credit that supports your financial goals and keeps your credit profile healthy.

Conclusion

Understanding the different types of business loans is key to making smarter financial decisions for your company in 2026. Whether you need to manage daily cash flow, invest in machinery, or expand your operations, the right loan can help your business grow without unnecessary stress.

Smart borrowing isn’t about taking the largest loan available; it’s about choosing the option that fits your needs and repayment capacity. When you match your business goals with the right financing solution, you gain flexibility, stability, and confidence in your financial planning.

For moments when urgent funding is needed, short-term business loans or government-backed schemes can provide quick support.

Ready to take control of your finances? Download the Pocketly app today on [Android] or [iOS] and experience a smarter way to manage your money.

FAQs

1. What are the main types of business loans in India?

The most common types include Working Capital Loans, Term Loans (short & long-term), Letter of Credit, Bill/Invoice Discounting, Overdraft Facility, Equipment/Machinery Loans, Government-backed Loans, and POS Loans or Merchant Cash Advances. Each serves a different business need.

2. How do I choose the right business loan for my company?

Consider your purpose (growth, cash flow, equipment), repayment ability, collateral availability, interest rates, and flexibility. Align the loan type with your business size, revenue stability, and financial goals.

3. Can startups get business loans without collateral?

Yes. Certain loans like Working Capital Loans, POS Loans, and many government-backed schemes (e.g., MUDRA, Stand-Up India) offer collateral-free options for startups and MSMEs.

4. What is the difference between a term loan and an overdraft facility?

A term loan provides a fixed amount for a specific period, with structured EMIs. An overdraft facility is flexible, allowing you to withdraw funds up to a limit and pay interest only on the used amount, making it ideal for short-term cash needs.

5. Are government-backed business loans easier to get than private bank loans?

Government-backed loans often have simplified documentation, lower interest rates, and guarantees, making them more accessible for MSMEs and startups. However, approval still depends on eligibility and business viability.