Foreign companies often assume they’re exempt from Indian tax liabilities simply because they are incorporated abroad. However, the concept of "Place of Effective Management" (POEM) challenges this assumption. POEM helps determine a company’s tax residency in India based on where key management and commercial decisions are made, rather than just its registered address.

The introduction of POEM has addressed key challenges faced by CFOs and tax teams, especially when boards are based in cities like London or Singapore, but critical decisions are made in India, such as Mumbai or Bengaluru. This mismatch can lead to a company being considered an Indian tax resident, subject to taxation on global income, compliance obligations, and scrutiny from tax authorities. Many businesses only realize this risk during assessments or audits, which can be costly and time-sensitive.

In this blog, we’ll explain what POEM is, how Indian tax authorities determine it, and what foreign companies with links to India need to know to navigate these rules effectively.

TL;DR

- POEM (Place of Effective Management) helps determine if a foreign company is treated as a tax resident in India.

- A company is resident if it is incorporated in India or its POEM lies in India during a financial year.

- POEM is about substance, meaning India looks at where key management and commercial decisions are actually made, not just where boards meet on paper.

- Foreign companies with Active Business Outside India (ABOI) may keep residency outside India if key business functions stay abroad.

- If POEM is in India, the company may be taxed on its global income, making POEM important for cross-border structuring and compliance.

What is the Place of Effective Management (POEM)?

Place of Effective Management (POEM) is the location where the key decisions that steer a company’s business are made. It’s not just about where papers are signed or where the company is officially registered; it focuses on where the actual decision-making happens.

In India, POEM is used to determine if a foreign company should be treated as an Indian tax resident for a particular financial year. Even if a company is registered in another country, if important decisions are made in India, it could be considered an Indian resident for tax purposes.

The focus here is on the real activities of the company, not just paperwork. Indian tax authorities look at how the company is run in practice, who is in charge, and where key decisions are made. This helps India align with global standards aimed at preventing companies from avoiding taxes by shifting profits to places with lower tax rates.

Example: A company might be registered in Singapore, but if its key decisions are made in Mumbai, India, then under POEM, it may be treated as an Indian tax resident.

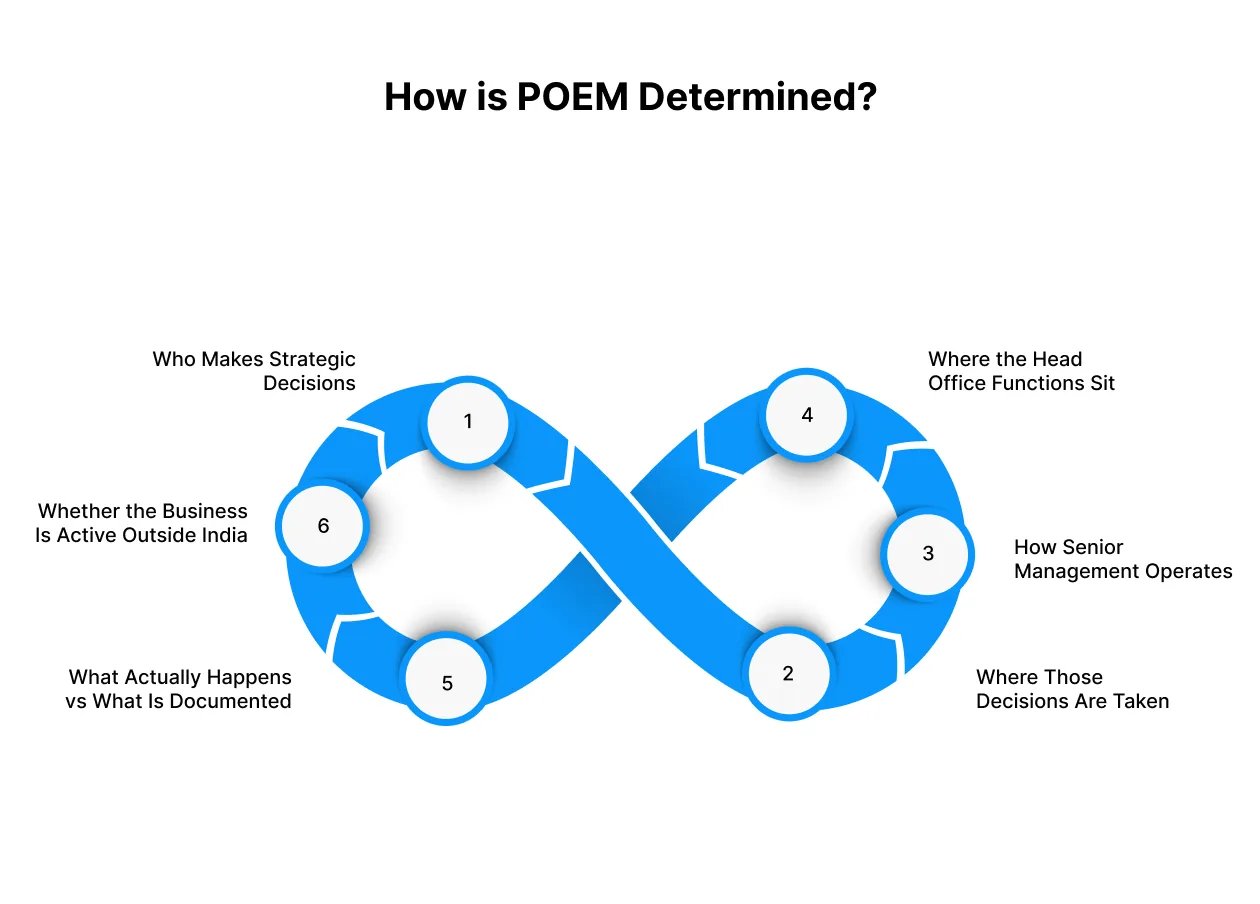

How is POEM Determined?

POEM is not determined by where a company is registered or where paperwork is stored. It is based on how the business is actually run and where important decisions come from. Tax authorities look for the place where leadership sets direction, controls strategy, and manages real operations.

POEM is not determined by where a company is registered or where paperwork is stored. It is based on how the business is actually run and where important decisions come from. Tax authorities look for the place where leadership sets direction, controls strategy, and manages real operations.

1. Who Makes Strategic Decisions

Every company has a group of people who decide on big matters such as investments, contracts, policies, and overall direction. This might be the board, a smaller executive team, or the founders. Identifying who holds this decision-making power is the first step, because POEM follows the actions of these people, not the legal structure.

For example, if a board is named on paper in Dubai but all major calls are made over video meetings led from India, the real decision makers are sitting in India.

2. Where Those Decisions Are Taken

After identifying who makes key decisions, authorities look at where these decisions are actually made. This is about genuine conversations, approvals, and negotiations, not just where minutes are signed. If meetings abroad only formalise choices already made in India, the substance of decision-making is still in India.

For instance, if strategy discussions happen in Mumbai and overseas meetings, simply record the outcome, the relevant activity that happened in India.

3. How Senior Management Operates

Tax authorities also observe where senior executives work from, where they spend their time, and how they direct the business. Routine oversight, policy enforcement, and team management can reveal where the company is truly controlled day to day.

A typical pattern might be a COO running operations from Bengaluru while the company remains legally incorporated abroad.

4. Where the Head Office Functions Sit

Many companies have a registered office in one country and a functional head office somewhere else. For POEM, the question is about the functional head office, which is the place where budgeting, planning, compliance, and reporting come together.

This could include activities like setting annual budgets, approving large contracts, or directing hiring and expansion plans.

5. What Actually Happens vs What Is Documented

Sometimes board minutes, contracts, or organisational charts suggest control from outside India, but communication logs, travel records, and email chains show decisions flowing from India. In such cases, actual conduct carries more weight than formal paperwork.

A company cannot rely on paperwork alone if day-to-day reality points somewhere else.

6. Whether the Business Is Active Outside India

If a foreign company has meaningful business activity outside India, with employees, assets, and income generated abroad, authorities may consider that the company’s POEM is outside India. This depends on real commercial substance, not just incorporation. The goal is to distinguish active multinationals from shell structures.

For example, a manufacturing firm with factories, staff, and sales teams abroad stands on a stronger footing than a passive investment entity with little activity overseas.

Also Read: Understanding TAN and Its Application

Active Business Outside India (ABOI) and Its Role in POEM

Not every foreign company with links to India ends up being treated as a tax resident here. The ABOI framework helps tax authorities separate operating companies from passive or shell structures. If a company shows real commercial activity outside India, its POEM is less likely to be placed in India.

What Counts as Active Business Outside India

A company is viewed as having ABOI when a large share of its income, assets, employees, and payroll is located outside India. The idea is simple: if most of the work, resources, and value creation happen abroad, the strategic heart of the business likely sits there too.

For example, a manufacturing group with factories, sales teams, offices, and payroll abroad shows clear commercial presence outside India.

How ABOI Affects POEM?

When a company meets ABOI conditions, authorities focus on the location of board meetings and senior decision-making. If strategic discussions and approvals happen outside India, the POEM is usually kept outside India as well. This creates clarity for companies that operate globally and are not set up for tax planning.

When ABOI Does Not Apply?

Companies that only hold investments or intellectual property often struggle to qualify for ABOI because they lack active operations. These entities usually have limited staff, minimal payroll, and income generated from passive sources. In such cases, POEM can shift toward the place where the investors or managers actually make decisions.

A simple example is a holding company registered abroad that collects dividends while its directors run everything from India. With no meaningful activity overseas, ABOI would not shield the entity.

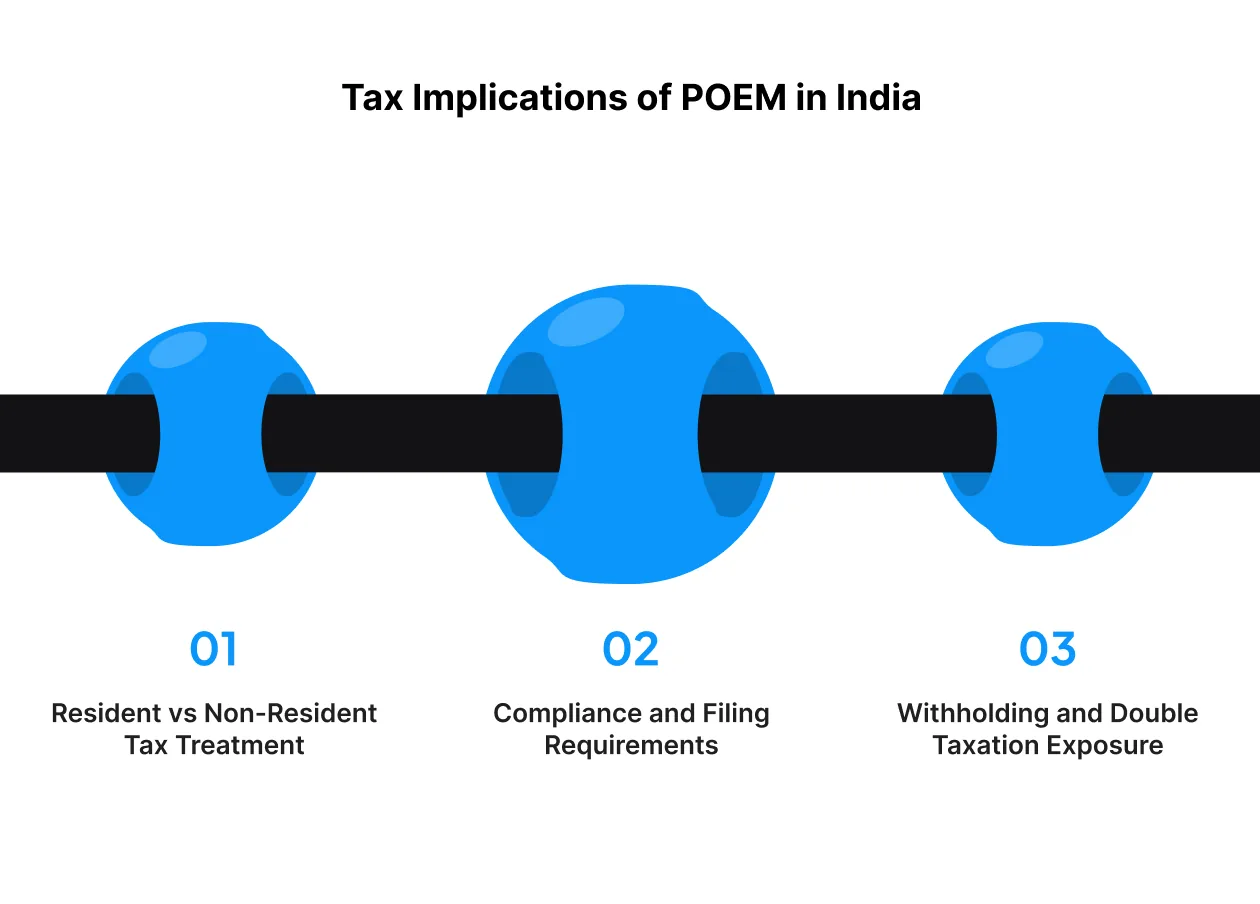

Tax Implications of POEM in India

Once a foreign company’s POEM is found to be in India, its tax position changes in a significant way. POEM is not just a classification test on paper; it determines how much of the company’s income falls under Indian taxation.

Once a foreign company’s POEM is found to be in India, its tax position changes in a significant way. POEM is not just a classification test on paper; it determines how much of the company’s income falls under Indian taxation.

Resident vs Non-Resident Tax Treatment

A non-resident company is taxed only on income that arises from India. Once POEM places a company inside India, it becomes a resident for that financial year. That means its global income, including earnings from foreign operations, may be brought under the Indian tax net.

For example, if a company incorporated in Singapore is effectively managed from India, profits from operations in Southeast Asia could still be examined for Indian tax purposes.

Compliance and Filing Requirements

Tax residency status triggers additional compliance duties. A resident company may need to file Indian corporate tax returns, maintain transfer pricing documentation, and provide disclosures related to overseas subsidiaries and assets. This adds administrative cost and demands stronger coordination between finance teams across jurisdictions.

Withholding and Double Taxation Exposure

A change in residency can also affect withholding taxes and treaty benefits. If the same income gets taxed in India and in another country, the company must rely on double taxation agreements to seek relief. Understanding these treaty rules early reduces the risk of paying tax twice on the same earnings.

Consider a situation where revenue from a European client is taxed in Europe based on source rules, while the same profit is taxed in India due to residency. Without treaty planning, the burden can be heavy.

POEM and Double Taxation Avoidance Agreements

When POEM places a foreign company within Indian residency rules, the company risks being treated as a resident in India and in its country of incorporation at the same time. Double Taxation Avoidance Agreements (DTAAs) are meant to avoid this outcome by providing a structured way to assign residency and determine taxing rights.

To understand how treaties handle POEM-driven dual residency, companies can walk through the following decision checklist.

1. Legal Incorporation Test

Confirm the jurisdiction of incorporation. This establishes the company’s default home country for legal purposes. On its own, this is not enough, but it forms the starting point for treaty analysis.

What to check:

• Certificate of incorporation

• Registered office documents

• Corporate filings in the home country

2. Effective Management Test

Identify where senior leadership sets policy, approves strategy, and supervises core business functions. Most OECD-style treaties place heavy weight on this factor, which often aligns with POEM.

What to check:

• Minutes of strategic meetings

• Location of executive leadership during decision-making

• Evidence of where commercial strategy originates

3. Active Business Presence Test

Evaluate what the company actually does in each country rather than relying on paperwork. Treaties look at the substance, such as employees, assets, and income-generating activity.

What to check:

• Staffing and payroll distribution

• Location of key assets and operations

• Revenue sources and client locations

4. Head Office and Control Functions

Map where centralised functions such as treasury, budgeting, finance, and compliance sit. These often reveal the real nerve centre of the business, even if incorporation sits elsewhere.

What to check:

• Budget approvals and treasury control location

• Location of ERP, accounting, or compliance oversight

• Evidence of contract approvals and risk management

5. Competent Authority Process

If both countries claim residency after applying these tests, the treaty allows authorities to negotiate a final residency through the competent authority mechanism. This process is more detailed and relies on documentary evidence and factual patterns.

What to check:

• Availability of tax residency certificates

• Audit records and statutory filings

• Supporting evidence for residency claims

Once residency is assigned under the treaty, the company can access relief methods such as tax credits, reduced withholding, or exemption of certain income streams. The exact outcome depends on the specific treaty wording and the nature of the company’s cross-border activities.

Also Read: Top Tax Saving Tips for Salaried Individuals

When Tax Residency Creates Planning Stress, Pocketly Can Help

Managing international business structures, tax filings, or compliance reviews can strain cash flow at awkward times. Professional fees, advisory costs, and documentation expenses often pile up before payments arrive. If you ever face a temporary shortfall during these periods, Pocketly offers a straightforward way to stay liquid without unnecessary complications.

Pocketly is a digital lending platform that provides quick, collateral-free loans to support short-term financial needs. You can borrow from ₹1,000 to ₹25,000, with interest starting at 2% per month and a processing fee between 1–8%. Approval is quick, and the funds reach your bank account in minutes.

Here’s how it works:

- Sign up with your mobile number

- Upload Aadhaar, PAN, and complete simple KYC

- Add your bank details

- Choose your loan amount and tenure

- Receive funds directly in your bank within minutes

It’s flexible, paperless, and transparent, with no hidden charges and 24/7 support. When compliance cycles, residency evaluations, or tax-related timelines create short-term financial pressure, Pocketly helps you bridge the gap with ease.

Bottom Line

POEM matters because it shifts the focus from where a company is registered to where decisions actually happen. If strategic control sits in India, the tax system treats the company as a resident, and that brings worldwide income into the Indian tax net. For global businesses operating across borders, it’s a reminder that structure alone isn’t enough; substance drives residency.

As companies expand, it becomes important to map where board decisions are taken, how senior management operates, and how governance is documented. This isn’t just about compliance; it’s about clarity, risk reduction, and better planning.

And while POEM deals with corporate taxation, financial planning at a personal level has its own pressures. Cash flow can get tight during certain months, or delays can throw off your schedule.

For those short-term moments, Pocketly offers a simple way to bridge gaps without disrupting bigger plans. If you ever need small-ticket, quick support, download Pocketly app on iOS or Android and access funds when it counts.

FAQs

1. What is the Place of Effective Management (POEM)?

POEM refers to the location where key management and commercial decisions needed to run a company’s business as a whole are actually made. It helps determine a company’s tax residency based on real decision-making rather than legal registration.

2. Why does POEM matter for income tax in India?

POEM is used to assess whether a foreign-incorporated company should be treated as a tax resident in India. If its POEM is in India during a financial year, it may be taxed in India on its global income.

3. Which companies are affected by POEM rules?

Foreign-incorporated companies that conduct business in multiple jurisdictions or have commercial or management ties to India may be evaluated under POEM rules to determine tax residency status.

4. How is POEM determined by tax authorities?

Authorities examine where strategic, policy-level decisions are made, where senior executives operate, and where the company’s head office functions. The focus is on substance over form, meaning actual conduct carries more weight than documentation.

5. What happens if a foreign company’s POEM is in India?

The company is classified as a resident for income tax purposes in India and is taxed on its worldwide income instead of only its India-sourced income.

6. Does POEM apply every year?

Yes, POEM must be assessed annually because a company’s management structure, decision locations, and business operations may change over time.

7. How does POEM interact with tax treaties?

If POEM results in dual residency, Double Taxation Avoidance Agreements (DTAAs) come into play. Treaty tie-breaker provisions help determine the final tax residency and prevent double taxation.