Ever wonder how some families manage to grow and preserve their wealth across generations while others struggle with financial instability? It’s not about luck or having a high income; it’s about the habits they’ve built and followed over time. Old money isn’t just a status symbol; it’s a mindset, rooted in disciplined spending, long-term thinking, and consistent wealth preservation.

The temptation to splurge on fleeting trends and focus on instant gratification often leads to financial stress, debt, and an inability to build lasting wealth. Old money habits, however, prioritise slow, steady growth and careful decision-making, ensuring wealth is maintained through generations.

If you’re ready to break free from the cycle of fleeting financial success and start building lasting wealth, the solution lies in adopting these time-tested habits. In this blog, we’ll dive into the old money habits that can help you take control of your finances and set yourself up for long-term prosperity.

Key Takeaways

- Old money habits revolve around conscious financial decisions that prioritise long-term wealth, stability, and sustainability over instant gratification.

- Building a solid savings habit and consistently investing in quality items instead of fleeting trends are core practices of old money families.

- Avoiding lifestyle inflation means living within your means, even as income increases, ensuring financial growth remains steady.

- The mindset of thinking generationally allows for better financial decision-making, promoting wealth accumulation across generations.

- Adopting these habits, regardless of your current wealth, can lead to financial peace, resilience, and long-term success.

What “Old Money” Really Means

“Old money” refers to wealth passed down through generations, built up over time and managed with a focus on long-term preservation. It’s not just about the amount of money, but how it’s maintained with careful investment, conservative spending, and a focus on legacy rather than status.

Families with old money typically avoid flashy displays of wealth. Instead, they focus on creating stability and financial security for future generations. The wealth isn’t about immediate luxury, but about ensuring enduring financial health through steady investments and strategic wealth management.

So, what sets old money apart from new?

- Old money: Wealth passed down across generations, prioritising legacy over immediate luxury.

- New money: Wealth recently acquired, often through entrepreneurial success, technology, or entertainment, with an inclination towards visible displays of wealth.

- Old money mentality: Focuses on long-term preservation, conservative financial management, and living within means.

Timeless Wealth Habits: How Old Money Builds Long-Term Financial Success

Old money families have mastered the art of building and preserving wealth over generations. While these habits may seem timeless, they can be applied to anyone looking to create financial security. Here are the key habits that contribute to lasting wealth:

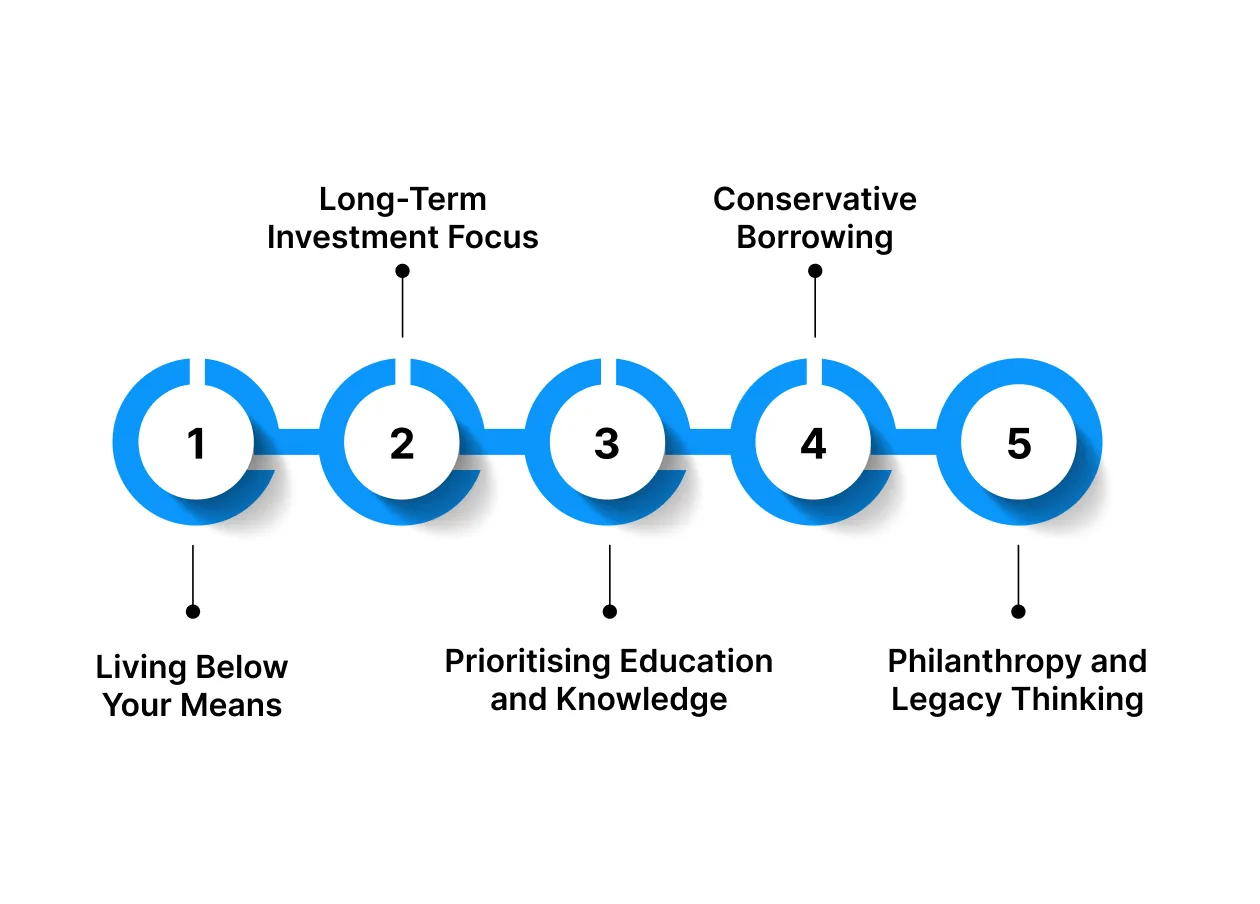

Living Below Your Means

Living below your means is a key habit of old money families. Even with significant wealth, they prioritise saving over spending. The idea is to avoid lifestyle inflation, where increased income leads to equally increased spending. Instead of indulging in expensive luxuries, old money individuals focus on value, choosing purchases that align with their long-term financial goals.

For example, instead of buying a new luxury car every few years, they may prefer to keep a well-maintained vehicle for several years. By living below their means, they free up more money for savings, investments, and future opportunities, ultimately building and maintaining wealth over time.

Long-Term Investment Focus

Old money families favour long-term investment strategies that offer steady growth over time. They focus on assets that appreciate in value, such as real estate, stocks, and bonds. Instead of chasing quick returns, their goal is to preserve and grow wealth slowly and consistently.

For instance, an old-money family might choose to invest in property in an up-and-coming area, knowing that its value will increase over time. Similarly, they might hold a diversified portfolio of stocks and bonds, allowing their investments to compound and grow without the pressure to sell prematurely.

Prioritising Education and Knowledge

Education, both formal and financial, is a cornerstone of old-money families. They understand that knowledge is a powerful tool for preserving and expanding wealth. By prioritising continuous learning, they stay informed about market trends, investment opportunities, and wealth management strategies.

For example, instead of relying solely on financial advisors, old money families often educate themselves about investing, estate planning, and tax laws. This allows them to make informed decisions that align with their values of long-term growth and sustainability.

Conservative Borrowing and Debt Management

Old money families tend to avoid debt and prefer to pay for big purchases with savings. They maintain a low level of borrowing, ensuring that they don’t overextend themselves financially. By doing so, they protect their wealth and maintain a stable financial foundation.

For example, instead of taking out a loan to purchase a luxury item, old money individuals would save up the necessary funds over time. This conservative approach to borrowing ensures that they don’t accumulate high-interest debt that could potentially erode their wealth in the long run.

Philanthropy and Legacy Thinking

Philanthropy is a core value of old-money families. They believe that wealth should be used for the greater good, not just personal gain. By giving back to their communities and supporting causes they care about, old money families leave a lasting legacy that extends beyond their immediate family.

For example, many old-money families establish charitable foundations or contribute to educational and healthcare initiatives. This focus on philanthropy ensures that wealth serves a greater purpose, benefiting future generations and leaving a positive impact on society.

Old Money Mindset vs Modern Money Habits

The way wealth is managed can differ greatly between old money families and those with newer sources of income. While both groups may have similar financial goals, their approach to money and spending is often quite different.

Here's how the old money mindset contrasts with modern money habits:

| Aspect | Old Money Mindset | Modern Money Habits |

| Spending Style | Thoughtful, modest, needs‑based spending. Focused on long‑term value. | Impulse or status-driven spending is often influenced by trends. |

| Wealth Visibility | Quiet, understated lifestyle. Wealth is not flaunted. | Flashy displays of wealth to showcase success and status. |

| Investment Approach | Long-term, stable returns. Focus on preserving and growing wealth. | Short-term gains and speculative investments, often chasing trends. |

| Financial Goals | Preserve wealth across generations, prioritise legacy. | Focused on maximising immediate lifestyle or personal payoff. |

| Attitude Toward Debt | Minimise debt, especially consumer debt. Debt is used sparingly for growth. | Embrace debt more freely, using it for lifestyle upgrades and consumption. |

| Lifestyle Inflation | Avoid lifestyle inflation. Wealth grows slowly and steadily over time. | Lifestyle inflation is common. As income grows, so do the living expenses. |

| Philanthropy | Giving back quietly, with a focus on long-term impact. | Giving is often tied to visibility or social causes. |

Also Read: How to Manage Monthly Expenses Smartly in 2025

Real Examples of Old Money Habits That Build Lasting Wealth

Old money habits are more than just principles; they’re living, breathing practices that have stood the test of time. These families don’t just build wealth; they protect it, grow it, and pass it on with careful strategy and discipline.

Here’s how some of the most enduring wealth legacies continue to thrive by following these habits:

The Walton Family

The Waltons, heirs to the Walmart empire, live by a principle of restraint despite their wealth. They avoid flashy displays of wealth, focusing instead on reinvestment into their business and maintaining a modest lifestyle.

This strategy isn’t just about saving; it’s about the long-term vision of making wealth sustainable across generations. Their wealth isn’t about instant gratification but about securing a future built on steady growth.

Core Habit: Long-term investments and reinvestment into core business operations, avoiding lifestyle inflation.

The Rothschild Family

The Rothschilds, once a banking dynasty, have thrived by following old money principles for over two centuries. Their approach to wealth focuses on diversification, spreading assets across industries such as real estate, mining, and finance.

By prioritising long-term growth and a low-risk investment strategy, they’ve not only preserved their wealth but have ensured it continues to expand. Their wealth is quiet, but the strategy behind it is formidable: slow, steady, and strategic diversification.

Core Habit: Diversification and steady growth, with a focus on wealth preservation across generations.

The Koch Family (Koch Industries)

With a fortune built on Koch Industries, the Koch family embraces a mindset of reinvestment and sustainability. Their wealth management strategy involves maintaining a focus on business efficiency and long-term growth rather than short-term profits.

The Kochs continue to prioritise innovation and operational excellence, ensuring that their wealth is not just preserved but perpetually expanding. Their habit of reinvesting in their industries, while staying true to their roots, ensures a continued legacy.

Core Habit: Reinvestment in business operations, fostering long-term innovation and growth.

The Kennedy Family

The Kennedys are known for their political legacy, but their financial habits exemplify old money values as well. Through strategic investments in real estate and an unwavering focus on education, they have built a foundation for enduring wealth.

The Kennedys’ commitment to philanthropy is also a hallmark of their approach; they give back in ways that align with their values, ensuring their legacy isn’t just financial but also rooted in societal impact.

Core Habit: Strategic real estate investments, education, and philanthropy designed for long-term societal impact.

The Koch Foundation

The Koch Foundation represents a modern example of how old money habits translate into long-term, impactful giving. Focused on causes that promote sustainability and individual freedom, the Kochs ensure their wealth isn’t just about accumulating assets, but also about using it to shape a lasting legacy.

Their focus on high-impact philanthropic efforts demonstrates that old money habits aren’t just about personal wealth; they’re about leaving a broader societal footprint.

Core Habit: Strategic, long-term philanthropy aimed at creating sustainable, societal impact.

Also Read: Simple Money Management Tips for Personal Finances

Common Mistakes to Avoid When Adopting Old Money Habits

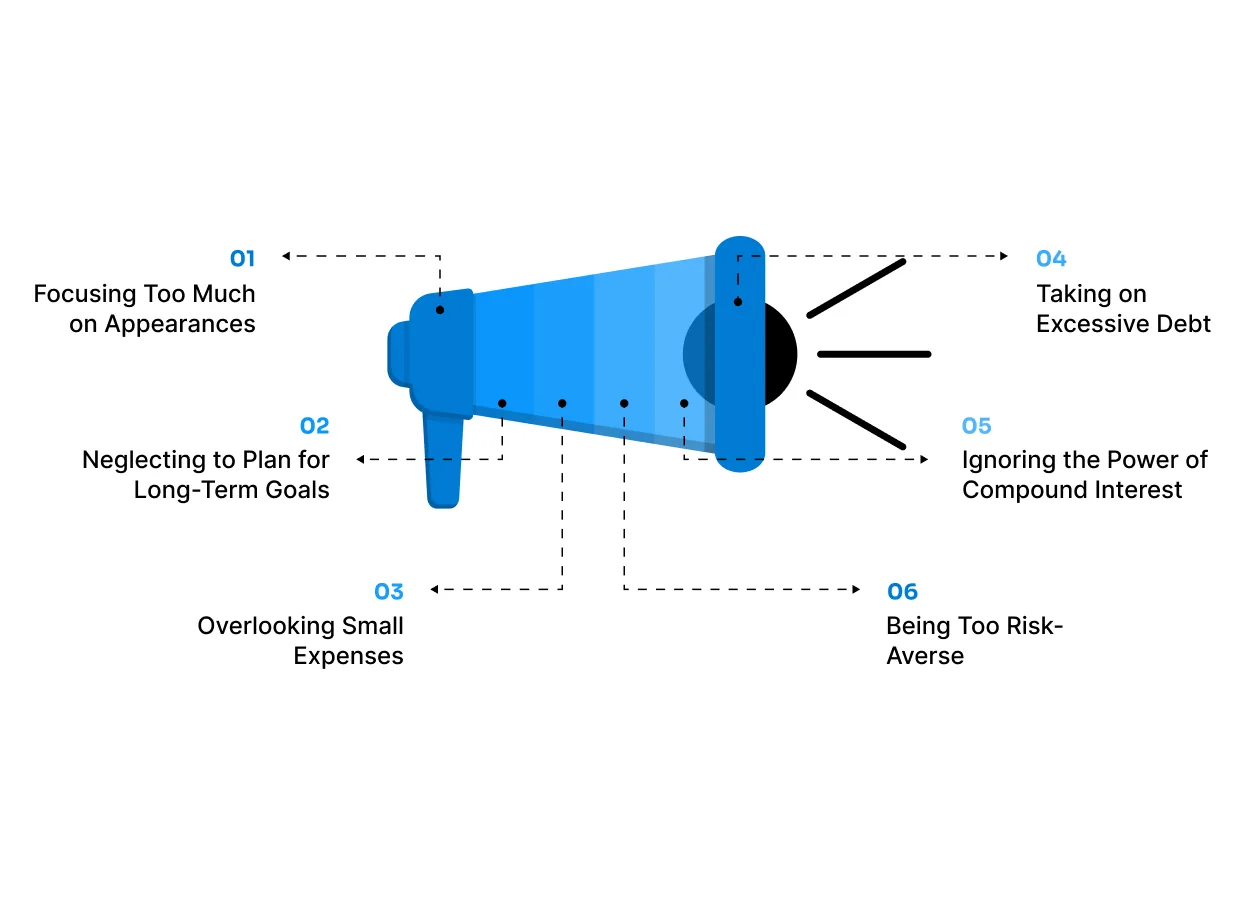

While old money habits are tried and tested, it’s easy to make mistakes when trying to implement them in your own life. Here are the common pitfalls to watch out for:

Focusing Too Much on Appearances

Emulating the "old money" lifestyle by purchasing luxury goods or showcasing your wealth can lead to lifestyle inflation. Rather than focusing on what others see, concentrate on building wealth quietly through consistent saving and investing. True wealth is about securing financial freedom, not seeking validation through visible displays.

Example: Buying an expensive sports car for status might seem appealing. However, investing that money could grow your wealth over time, instead of it depreciating immediately.

Neglecting to Plan for Long-Term Goals

Old money habits rely on long-term thinking and planning. Without clear financial goals, it’s easy to lose sight of your objectives. Develop a comprehensive plan for savings, investments, and wealth preservation. This ensures you stay focused and consistent, paving the way for financial security.

Example: Without a structured retirement plan, you might spend impulsively now. Later, you could find yourself scrambling to save, which leads to stress as you near retirement.

Overlooking Small Expenses

Small, everyday expenses can quietly undermine your financial goals. While large expenditures are easy to track, small, recurring costs like daily coffees or spontaneous purchases can add up. Build awareness of these expenses and adjust your budget accordingly. This prevents them from draining your resources.

Example: Spending ₹200 a day on coffee adds up to ₹6,000 a month. That’s ₹72,000 a year. This could be invested in a high-growth mutual fund for long-term returns.

Taking on Excessive Debt

Taking on too much debt can hinder your ability to build wealth. Old money families avoid excessive borrowing and debt accumulation, focusing on savings and investments instead. By carefully managing and minimising your debt, you maintain financial stability. This ensures that your wealth grows over time.

Example: Using credit cards with high interest rates for everyday expenses can lead to growing debt. Budgeting for these expenses and paying off balances monthly avoids accumulating interest.

Ignoring the Power of Compound Interest

Compound interest is a powerful tool for wealth-building. Failing to invest early and regularly, or opting for low-growth options, limits potential returns. Starting early, even with small amounts, ensures your wealth grows steadily over time. This maximises the benefits of compound interest for long-term financial success.

Example: Investing ₹5,000 a month at 7% return from age 25 could result in over ₹5 million by 65. Waiting until 40 drastically reduces that amount due to fewer years of compound growth.

Being Too Risk-Averse

Old money habits prioritise stability, but it’s important to take calculated risks. Avoiding all investments due to fear can prevent wealth growth. Balancing risk and reward is key. Taking well-researched, calculated risks accelerates financial progress while maintaining a stable foundation.

Example: Avoiding the stock market due to perceived risk prevents you from benefiting from long-term growth. A balanced portfolio of stocks and bonds helps manage risk while growing wealth.

How Pocketly Can Help You Manage Unexpected Expenses

Even with a well-managed budget, life can throw financial challenges your way. Whether it's a sudden medical bill, an emergency repair, or an unexpected fee, these expenses can disrupt your financial plans. Having a reliable financial backup during such times is crucial for maintaining stability.

Pocketly is here to provide that support. As a digital lending platform, we offer quick, easy access to funds without the hassle of traditional bank loans. Whether you're a student, a working professional, or self-employed, Pocketly ensures you can manage short-term financial gaps without the stress.

- Quick and Flexible Loans: Borrow amounts ranging from ₹1,000 to ₹25,000, perfect for handling sudden expenses.

- Affordable Rates: Our interest rates start at just 2% per month, with processing fees ranging from 1-8%, ensuring transparency and fairness.

- Completely Digital Process: Skip the paperwork. Our entire KYC process is online, so you get the funds you need quickly and securely.

- Flexible Repayment Options: Whether you're salaried or a student, choose the repayment option that suits your cash flow, whether in full or in EMIs.

How to Apply for a Pocketly Loan:

Download: Get the Pocketly app from the Google Play Store or Apple App Store.

KYC: Complete the simple, digital KYC process with your basic details.

Choose: Select the loan amount that fits your needs (up to ₹25,000).

Disbursal: Once approved, funds are transferred directly to your bank account instantly.

Conclusion

Embracing old money habits is not just about emulating wealth; it’s about cultivating a mindset that values long-term financial stability and thoughtful spending. By prioritising savings, investing wisely, and avoiding lifestyle inflation, you create a strong foundation for future success.

True financial security isn’t built on immediate gains, but on disciplined, intentional choices that pay off over time. When you focus on lasting wealth and sustainable practices, you can achieve financial freedom, regardless of your starting point.

Life’s financial hurdles are inevitable, but with the right habits, you’ll be equipped to handle them.

Ready to implement smarter financial strategies? Download the Pocketly app today on Android or iOS and discover how quick, hassle-free loans can help you stay on top of your finances.

FAQs

1. What are old money habits?

Old money habits are the financial behaviours and mindset practices used by families that preserve and grow wealth over generations, such as living below your means, long‑term planning, and disciplined saving.

2. How are old money habits different from typical money habits?

Old money habits focus on long‑term wealth preservation and modest spending, while many modern money habits centre on consumption and short‑term lifestyle upgrades.

3. Can anyone adopt old money habits?

Yes, principles like conscious spending, saving consistently, investing wisely, and avoiding lifestyle inflation can be applied by anyone to improve financial stability.

4. What is the mindset behind old money wealth?

The old money mindset emphasises thinking in generations rather than seasons, valuing quality over status, and making financial decisions that support sustainability and long‑term growth.

5. Do old money habits guarantee wealth?

No habit can guarantee wealth, but adopting old money practices can significantly increase financial resilience, reduce reckless spending, and help build lasting wealth over time.