Money today moves faster than ever. UPI, digital credit, and fintech apps have changed how young Indians spend, save, and borrow. But convenience without understanding often leads to confusion, missed opportunities, and financial stress.

Financial awareness means more than knowing a few terms.

It is the skill of managing money wisely, staying safe online, and knowing your financial rights.

It is what helps you make decisions confidently, not impulsively.

In this guide, we will explore simple, practical ways to build financial awareness in 2025, from budgeting and credit to digital safety and responsible borrowing.

Key Takeaways

- Financial awareness is a daily habit, not a one-time lesson. Seeing where your money goes, setting goals, and checking progress monthly keeps you confident and in control.

- Safety is part of awareness. Always verify lenders, protect your UPI PINs, and report anything suspicious through official RBI or NPCI portals.

- Credit isn’t bad; careless credit is. Borrow only for real needs, read all costs before agreeing, and repay on time to build your financial reputation.

- Learning keeps you secure. Follow trusted sources like RBI, SEBI, and NPCI to stay updated. The more you know, the smarter and safer your financial decisions become.

What “Financial Awareness” Really Means in 2025

Financial awareness means understanding how money moves, how choices affect your future, and how to stay financially safe.

In 2025, being financially aware matters more than ever. Digital payments, instant loans, and investment apps have made money decisions faster, but not always easier.

The challenge today is not access, but awareness, knowing what to do and what to avoid. Let us look at what financial awareness truly covers and how it differs from other money concepts.

Financial awareness vs literacy vs education: what is the difference?

These three terms are often used interchangeably, but they are not the same.

| Term | Meaning | Example |

| Financial education | Learning basic money concepts through formal study or resources. | Reading about budgeting or saving online. |

| Financial literacy | Understanding and applying those concepts in real life. | Creating a budget and following it. |

| Financial awareness | Recognising financial risks and opportunities in daily life, and acting wisely. | Knowing how to avoid scams or choose fair credit. |

Financial awareness, therefore, is literacy in action, knowledge plus behaviour.

The India context: digital finance and the need for safety

India’s financial system has gone digital faster than most countries. From UPI and online wallets to instant credit apps, everything is app-first and quick.

But with this convenience comes risk. Every UPI PIN entered, every new app downloaded, and every payment made online requires awareness to ensure safety and informed decisions.

Financial awareness in India today is about balance: using technology confidently, but with caution.

Now that we understand what financial awareness means, the next step is simple: seeing your money clearly. That’s where budgeting and cash-flow awareness come in.

Also Read: Understanding Financial Literacy: Importance And Benefits

Step One: See Your Money Clearly (Budgeting & Cash Flow)

You cannot control what you cannot see. That is why every form of financial awareness starts with visibility, knowing how money enters and leaves your life.

Budgeting is not about restriction. It is a map that helps you understand your habits, spot silent leaks, and plan your spending with intention.

One-page budget, income, and expense buckets

Start simple. Write down your monthly income, salary, allowance, freelance payments, or side earnings. Then list your fixed expenses (rent, bills, EMIs) and variable expenses (food, transport, shopping).

Group them into three clear buckets:

- Essentials – what you must pay for (needs)

- Goals – what you want to build (savings, investments)

- Lifestyle – what you enjoy (wants)

When you see your money divided this way, awareness becomes effortless.

Spotting leaks and finding quick savings

Small, frequent expenses often go unnoticed, that extra coffee, daily delivery fee, or unused subscription. Review your spending weekly to catch these leaks.

A simple question works wonders: “Do I still use this or need this?”

Cancel or reduce what adds little value. Even ₹100 saved weekly builds a habit stronger than any budgeting app.

Setting money goals that actually work

Financial awareness grows when your money has purpose. Set short-term goals (clearing small debts, buying a gadget, building an emergency fund) and long-term goals (education, travel, savings).

Keep them specific, realistic, and measurable. For example: “Save ₹500 weekly for three months” is better than “save more.” When goals feel achievable, discipline feels natural, not forced.

Once you can see your cash flow clearly, awareness becomes real.

The next step? Building protection, a safety net that prevents emergencies from turning into financial setbacks.

Also Read: Understanding Personal Finance and Budgeting for Financial Needs

Step Two: Build a Financial Safety Net

Financial awareness is not only about growing money, it’s also about protecting it. Unexpected events like medical bills, job delays, or family emergencies can drain savings fast. A safety net prevents those shocks from turning into financial crises.

You do not need a large amount to begin. Awareness here means consistency, saving small amounts regularly before trouble appears.

Building a small emergency fund

Start by setting a simple target: aim for one month of expenses as your first milestone.

For students or freelancers, even ₹5,000–₹10,000 can make a big difference in emergencies.

Gradually grow this buffer to three months’ expenses over time. This small cushion means you can handle a delay or a repair without borrowing unnecessarily.

Where to keep it: liquid and low-risk

An emergency fund should be easy to access and safe from market swings. Keep it in a separate savings account, not your main spending one. Options like liquid mutual funds or recurring deposits also work for slightly better returns.

Avoid locking this money in long-term schemes. The goal is quick access, not profit.

Automate tiny contributions that add up

Set up an automatic transfer right after payday, even ₹300 or ₹500 weekly. Small, regular amounts grow faster than you think. Automation builds awareness through habit: you save without deciding each time.

Once your safety net is in place, you can face financial surprises with calm, not panic.

The next part of awareness is understanding something most people fear — debt. Handled wisely, it can help you grow. Handled carelessly, it can trap you.

Also Read: Understanding the Basics of Financial Planning and Its Importance

Step Three: Know Your Credit and Debt

In 2025, credit is easier to get than ever, but that makes awareness even more important. Before borrowing, every financially aware person should understand one thing clearly:

Borrowing is not bad. Borrowing blindly is.

Knowing how credit works means understanding the cost, the commitment, and the long-term effect on your financial profile.

Good vs bad debt: learn to tell the difference

Good debt helps you build value: education, skill development, or small business needs. It contributes to your future income or stability.

Bad debt funds short-term wants: like impulse shopping or luxury upgrades. It feels rewarding today, but limits your options tomorrow.

Financial awareness means asking one question before borrowing: “Will this expense improve my future or just my present?”

Reading interest, processing fees, and repayment timelines

Every loan has a cost beyond the principal. Before signing up, check:

- Interest rate (monthly or annual)

- Processing fee (a one-time charge)

- Late payment penalty

If a loan charges 2% per month and a 5% processing fee, the real cost is higher than it appears. Awareness means reading these numbers, not just the headline offer.

Always repay on time, not only to avoid extra charges but to build a reliable record for future needs.

Why your credit score matters

Your credit score is your financial reputation. Lenders use it to decide if you qualify for a loan and at what rate.

A score above 750 is considered healthy. You can check your report for free through official sites like TransUnion, CIBIL, or via regulated credit apps.

To build and maintain a good score:

- Pay bills and EMIs on time

- Avoid taking multiple loans at once

- Keep your credit card utilisation below 30%

Financial awareness means using credit responsibly, understanding it as a tool, not a trap.

When you see borrowing and repayment clearly, you stay in control of your money and your future choices. The next step in building awareness is learning how to grow your money mindfully, without unnecessary risk or complexity.

Also Read: Simple Money Management Tips for Personal Finances

Step Four: Grow Your Money Mindfully

Financial awareness is not about chasing every investment trend. It is about understanding how your money grows, what risks you are taking, and whether those choices match your goals.

You do not need to be an expert investor. You only need to know the basics: save first, invest steadily, and stay consistent.

Saving regularly before investing

The best investment habit begins with saving. Before you start a SIP or buy a plan, ensure you have your emergency fund and essential expenses covered.

Set aside a fixed portion of your income, even 10%, before spending.

Automate this process if possible. When saving becomes automatic, investing feels natural, not forced.

Basic investment awareness: simple, long-term, consistent

Start with what you understand. For beginners, mutual funds, index funds, or recurring deposits are simple options. Avoid anything promising guaranteed high returns or “no-risk profits.”

Consistency matters more than timing. Even small monthly investments grow over the years through compounding. Review progress annually, not daily. Awareness means patience, not panic.

Staying consistent beats chasing trends

Many new investors lose money because they switch constantly, buying when the market rises, selling when it falls. True awareness is emotional control.

Stick to your plan. Adjust only when your goals or income change.

Remember: steady beats clever in long-term wealth building.

With this mindful growth mindset, the next challenge is equally important: protecting what you already have, especially online.

Also Read: Best Trading and Investing Apps for Students and Beginners

Step Five: Stay Safe in the Digital Financial World

In 2025, financial awareness is inseparable from digital safety. Almost every financial activity now happens online: UPI, credit apps, trading platforms, and payment links.

Convenience comes with risk, and awareness is your best defence.

UPI hygiene and QR safety

UPI makes payments instant, but also invites mistakes and scams. Follow these simple habits:

- Never share your UPI PIN with anyone.

- Check names carefully before approving payment requests.

- Avoid scanning QR codes from unknown sources.

Always verify transaction notifications directly through your banking app. The NPCI regularly updates safety guidelines, stay informed from official sources, not social media forwards.

Spotting fake lending and investment apps

Thousands of fake apps mimic real ones to trick users. Financial awareness means verifying before you download.

Check if the lender or app is listed on the RBI’s regulated entities page or has a registered NBFC partner.

Be sceptical of any app that:

- Promises instant loans without KYC

- Demands access to contacts or photos

- Pushes you to repay through personal accounts

If an offer sounds too easy or too urgent, it is probably unsafe.

Reporting fraud quickly

If you suspect a scam, act fast.

Contact your bank immediately to freeze the transaction.

You can also report through:

- The RBI’s Complaint Management System (CMS)

- The National Cyber Crime Reporting Portal

- Your bank’s helpline or branch

Document everything: screenshots, messages, transaction IDs. Quick reporting often increases the chance of recovering funds.

Staying digitally aware keeps your finances secure. The next step in building complete financial awareness is understanding your rights and protections as a consumer, knowing who regulates what, and where to turn for help.

Also Read: Refinance: Definition, How It Works, Types, and Example

Step Six: Know Your Rights and Where to Get Help

True financial awareness means knowing not only how to manage money but also where to go when things go wrong. In India, several regulators protect different parts of the financial system.

Understanding who handles what helps you act fast and confidently in case of a problem.

Regulators and their roles

Here is a quick guide:

| Regulator | Area of Responsibility | Example |

| RBI (Reserve Bank of India) | Banks, NBFCs, digital lending, and payments | Complaints about loans, credit cards, or UPI apps |

| SEBI (Securities and Exchange Board of India) | Stock markets, brokers, and investment platforms | Issues with demat accounts or fake investment offers |

| IRDAI (Insurance Regulatory and Development Authority of India) | Insurance companies and policies | Policy claim delays or wrong product information |

| PFRDA (Pension Fund Regulatory and Development Authority) | Pension schemes (NPS) | Contribution or withdrawal disputes |

These regulators also run official awareness campaigns, like the RBI’s “Financial Literacy Week” or SEBI’s “Investor Awareness Programmes.” Bookmark their verified sites for updates, not unverified blogs or influencers.

Filing complaints: RBI Ombudsman & CMS portal

If you face issues with a regulated financial service, like wrong loan charges or payment errors, use official channels. The RBI Integrated Ombudsman Scheme covers banks, NBFCs, and prepaid wallet providers.

You can file a complaint online through the RBI Complaint Management System (CMS). It’s free, simple, and completely digital.

Before filing, always try to contact your service provider once. If unresolved within 30 days, escalate it through CMS. Awareness is not only about prevention, but it is also about knowing your rights to resolution.

“Your Money, Your Right” 2025 initiative

As part of India’s push for transparent finance, the RBI and Press Information Bureau launched the “Your Money, Your Right” campaign.

It helps people track unclaimed deposits, dividends, and refunds easily. You can check whether you have unclaimed funds through the official RBI site, not through forwarded links.

Awareness of rights protects you from losing what is already yours. Once you know how to protect your interests, the next challenge is maintaining awareness, keeping your financial learning active and consistent.

Also Read: Self-Regulation in RBI's FinTech Framework Explained

Step Seven: Keep Awareness Alive (Monthly Habits)

Financial awareness is not a one-time task. Like physical fitness, it stays strong only when you maintain it regularly.

The good news? You can stay financially aware in less than half an hour a month.

Monthly 15-minute money review

Pick one fixed date each month, for example, the first Sunday, and review:

- Your income and expenses for the previous month

- Any upcoming bills, renewals, or goals

- Whether your emergency fund is still intact

This small ritual keeps you connected with your finances and prevents unpleasant surprises.

Learn one new concept each month

Choose one small topic to read about, like credit utilisation, compound interest, or UPI safety.

Follow official sources such as:

- RBI’s Financial Education Site

- SEBI Investor Awareness Portal

- NPCI UPI Safety Hub

Awareness builds gradually, one clear idea at a time.

Keep your data and documents secure

Store important financial documents digitally, but safely. Use strong passwords and two-factor authentication for apps. Review app permissions every few months.

Your awareness is only as strong as your digital safety. When you make awareness a monthly habit, confidence becomes natural.

You no longer fear bills, credit, or new tools; you understand them. And that is the true goal of financial awareness: control without anxiety.

Also Read: Difference Between Private Finance and Personal Finance

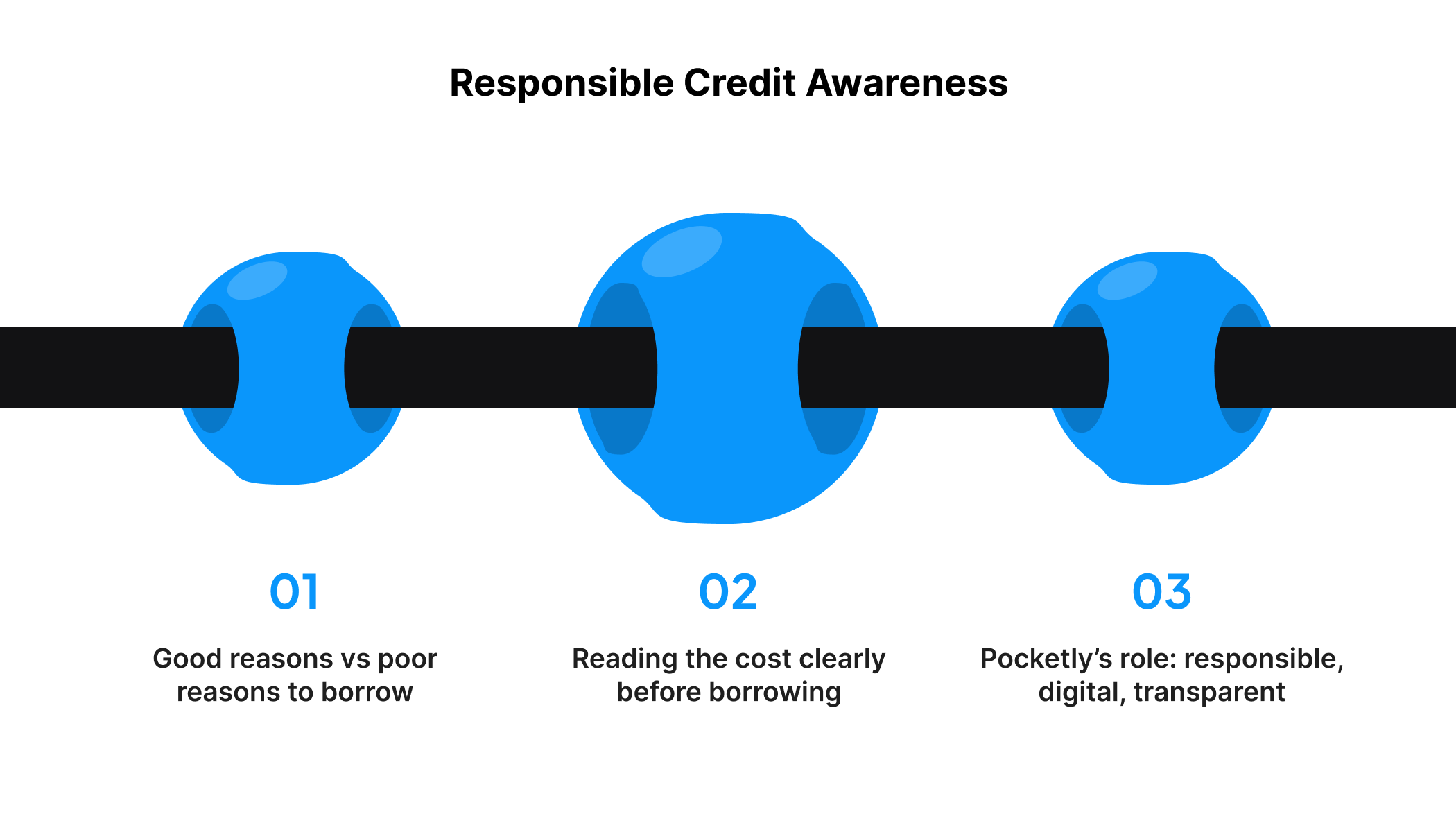

Step Eight: Responsible Credit Awareness

Being financially aware means knowing when credit helps and when it hurts. Used correctly, short-term loans can solve immediate problems without damaging your long-term stability. Used carelessly, they create cycles of stress and debt.

Financial awareness gives you the clarity to know the difference.

Good reasons vs poor reasons to borrow

Good reasons include essential, time-sensitive needs, like medical expenses, education fees, or urgent travel. These are productive uses that prevent bigger financial setbacks later.

Poor reasons include lifestyle upgrades, impulse shopping, or unnecessary subscriptions. If something can wait, it’s better to save first than borrow.

When you connect credit with purpose, you stay in control, not dependent.

Reading the cost clearly before borrowing

Every loan has two parts: what you borrow and what you pay to borrow it. Understanding this difference is financial awareness in action.

Pocketly’s transparent example makes it simple:

- Loan amount: ₹10,000

- Interest rate: 2% per month

- Processing fee: 1–8% (depending on loan size and tenure)

- Tenure: short-term, flexible repayment

That means you always know your total cost before you borrow, no hidden surprises. Being aware of costs is what separates smart borrowing from regretful debt.

Pocketly’s role: responsible, digital, transparent

Financial awareness includes knowing how to borrow wisely. Sometimes, even with good planning, you might face an unexpected expense or short-term gap.

That is where Pocketly can help.

Key Features

- No collateral required, 100% digital and paperless.

- Interest rates start from 2% per month.

- Processing fee: between 1% and 8%, depending on loan amount and tenure.

- No hidden charges, every cost is shown upfront.

- Flexible repayment, repay early anytime to save on interest.

Pocketly’s goal is simple: to support financially aware users who borrow responsibly and value transparency.

Conclusion

Financial awareness is not a subject you learn once. It is a habit that shapes how you earn, spend, save, and protect your future.

In 2025, awareness means being informed, alert, and confident, whether you are managing UPI, checking your credit score, or deciding when to borrow.

Start by seeing your money clearly, building your safety net, and protecting yourself online. Over time, these small actions turn into lifelong confidence with money.

And if you ever face a genuine short-term gap, do it the smart way, use transparent, RBI-compliant platforms like Pocketly.

Take charge of your finances. Stay aware, stay secure, and move forward with confidence.

Download the Pocketly App

FAQs

1. What is the first step to becoming financially aware?

Start by tracking your money, noting what you earn, spend, and save each month. Awareness begins with visibility. Once you know your flow, you can start improving it through budgeting and goal setting.

2. How do I verify if a lender or app is legitimate?

Check whether it is registered with the Reserve Bank of India (RBI) or works with an RBI-licensed NBFC. Visit the RBI’s official website, not third-party blogs, for the list of authorised entities. Avoid apps that demand unnecessary permissions or pressure you to borrow instantly.

3. How often should I check my credit report?

Check your credit score and report at least twice a year. You can do this for free through official agencies like TransUnion, CIBIL, Equifax, or Experian. Reviewing regularly helps you spot errors and maintain a healthy score.

4. How can students improve financial awareness early?

- Start budgeting your monthly allowance.

- Learn about digital payment safety and UPI hygiene.

- Build small savings habits using jars or simple apps.

- Follow RBI and SEBI educational resources online.

Small, consistent awareness in college builds confidence for adult financial life.

5. What are reliable sources to learn more about financial awareness?

Refer only to official and verified sources, such as:

- RBI Financial Education Site: for money management basics

- SEBI Investor Education Portal: for investing and fraud awareness

- NPCI UPI Safety Hub: for digital payment protection

- Press Information Bureau: for government campaigns and alerts

Bookmark them and read one resource every month; awareness grows with steady learning.