Every entrepreneur dreams of growing their business, but reality often hits in the form of tight cash flow, unexpected expenses, or missed opportunities. You know your business has potential, yet without the right funds at the right time, even the best ideas can stall.

The problem is that taking a business loan feels complicated. Interest rates, repayment schedules, eligibility criteria, and endless paperwork can make even seasoned business owners hesitant. Pick the wrong loan, and you could end up trapped in debt or paying far more than necessary.

The solution is simpler than most think. With a clear roadmap, knowing which loan suits your needs, how to prepare your documents, and how to approach lenders, you can access funds quickly and confidently.

This blog will guide you step by step through the process of taking a business loan, helping you discover growth, cover urgent expenses, and scale your business without financial stress.

TL;DR

- A business loan provides the funds needed to grow, cover expenses, or manage cash flow without dipping into personal savings.

- Eligibility depends on your business type, credit score, revenue, and proper documentation like financial statements and tax returns.

- Choose the right loan type: term loan, line of credit, or invoice financing—based on your business needs, repayment capacity, and flexibility.

- Follow a step-by-step approach: assess requirements, prepare documents, submit application, get approval, receive funds, and manage repayment responsibly.

- Avoid common mistakes like over-borrowing, ignoring hidden fees, or skipping lender comparisons to ensure safe, effective borrowing for business growth.

Understanding Business Loans

A business loan is a financial product meant to provide companies with the funds they need to start, operate, or expand their operations. Unlike personal loans, which are based primarily on individual creditworthiness, business loans consider both the business’s financial health and the owner’s credit profile.

Business loans come in different types, each suited for specific business needs:

- Term Loans: A lump sum borrowed upfront and repaid over a fixed period with interest. Ideal for purchasing equipment, investing in infrastructure, or expanding operations.

- Working Capital Loans: Short-term loans intended to cover day-to-day operational expenses, like paying suppliers or managing payroll during cash flow gaps.

- Business Lines of Credit: Flexible credit that allows firms to borrow, repay, and borrow again up to a set limit. Interest is only charged on the amount used, making it ideal for fluctuating cash needs.

- Invoice Financing: Loans secured against outstanding invoices. This helps businesses access immediate cash instead of waiting for clients to pay.

- Equipment or Asset Financing: Loans specifically for purchasing machinery, vehicles, or other assets, usually secured against the asset being financed.

Understanding the type of loan your business requires helps ensure that you borrow responsibly, avoid unnecessary debt, and use the funds to drive growth effectively.

Example: A café looking to expand its seating area may take a term loan for renovations, while the same café might use a business line of credit to manage slow months in cash flow.

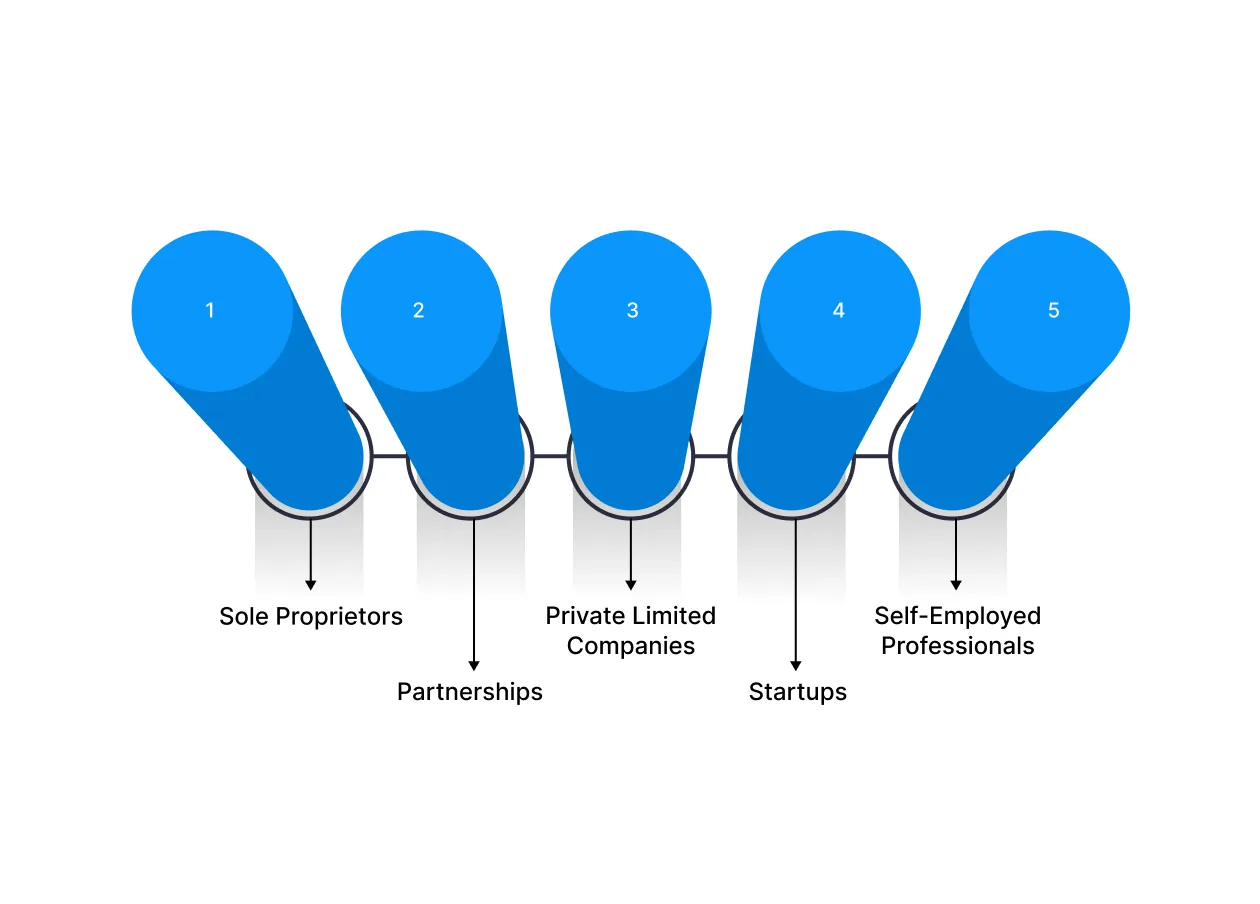

Who Can Apply for a Business Loan?

Business loans are not limited to one type of entrepreneur. Different business structures have specific eligibility criteria, but almost anyone running a legitimate business can apply.

Sole Proprietors

Individual business owners can apply using their personal credit score and business financials. Some lenders may ask for collateral depending on the loan type.

Example: A local bakery run by a single owner secures a ₹5 lakh working capital loan to buy ingredients for a high-demand festive season.

Partnerships

Partnership firms need business registration documents, KYC of all partners, and financial statements. Lenders consider the creditworthiness of each partner.

Example: Two friends running a café get a ₹10 lakh term loan to expand their seating area and purchase new kitchen equipment.

Private Limited Companies

Registered private limited companies often have access to higher loan amounts. Lenders evaluate balance sheets, profit & loss statements, and tax returns to approve the loan.

Example: A software company takes a ₹50 lakh loan to develop a new SaaS product and hire additional developers.

Startups

Startups may face stricter scrutiny due to limited operational history, but government-backed schemes and NBFCs offer tailored loans with lower collateral requirements.

Example: A tech startup, operating for six months, secures a ₹15 lakh government-backed loan to develop a mobile app for small businesses.

Self-Employed Professionals

Freelancers, consultants, and independent contractors can qualify by showing income proof, GST returns, and bank statements.

Example: A freelance graphic designer takes a ₹2 lakh loan to purchase high-end computers and software licenses for client projects.

Also read: Understanding Cash Flow: Definition, Types, and Analysis

Preparing for a Business Loan Application

Before applying for a business loan, preparation is key. Lenders need to see that your business is financially healthy and that you have a clear plan for the funds. Careful preparation increases your chances of approval and can help you secure better terms.

1. Check Your Credit Score

Your personal and business credit scores are often the first thing lenders evaluate. A strong credit history shows that you are responsible with borrowed money, while a low score can result in higher interest rates or rejection.

- Tip: Obtain your credit report from major bureaus and review it for errors. Correcting mistakes beforehand can improve your approval chances.

2. Organise Financial Statements and Documents

Lenders require proof of your business’s financial health. Commonly requested documents include:

- Balance sheets and profit & loss statements

- Bank statements (typically last 6–12 months)

- Tax returns and GST filings

- Business registration and legal documents

Having these documents ready ensures a smooth application process and reduces delays.

3. Determine the Loan Amount and Purpose

Calculate exactly how much funding you need and specify its purpose. Borrowing too little may not meet your needs, while borrowing more than necessary can increase debt and repayment pressure.

- Example: A retailer needing ₹5 lakh for inventory should clearly state that purpose, rather than applying for a generic “business expansion” loan.

4. Prepare a Business Plan (Optional but Recommended)

A detailed business plan demonstrates how the loan will be used to bring in revenue or improve operations. It reassures lenders that you have a strategy to repay the loan.

- Tip: Include financial projections, marketing plans, and a repayment strategy in your plan.

Careful preparation not only improves your chances of getting approved but also sets a foundation for responsible borrowing.

Choosing the Right Type of Business Loan

Not all business loans are the same. Choosing the right type depends on your purpose, repayment capacity, and the urgency of funds. Picking the wrong loan can lead to higher costs or repayment stress, so it’s important to understand the main options.

| Loan Type | Key Features | Ideal For | Typical Terms |

| Term Loan | Fixed amount borrowed upfront, repaid in EMIs over a set period | Businesses needing a large, one-time capital infusion for expansion or equipment | 1–5 years, fixed or floating interest |

| Business Line of Credit | Flexible credit limit; borrow, repay, and borrow again as needed | Businesses with fluctuating cash flow or short-term working capital needs | Revolving, interest only on the borrowed amount |

| Invoice Financing | Borrow against unpaid invoices | Companies are waiting for client payments to maintain operations | Short-term, usually 30–90 days |

| Working Capital Loan | Short-term loan for daily operations like salaries, rent, and inventory | Startups or SMEs with seasonal or temporary cash flow gaps | Typically under 12 months |

| Equipment Financing | Loan specifically for buying machinery or tech | Businesses investing in equipment without dipping into savings | Tied to asset life, often secured by the equipment |

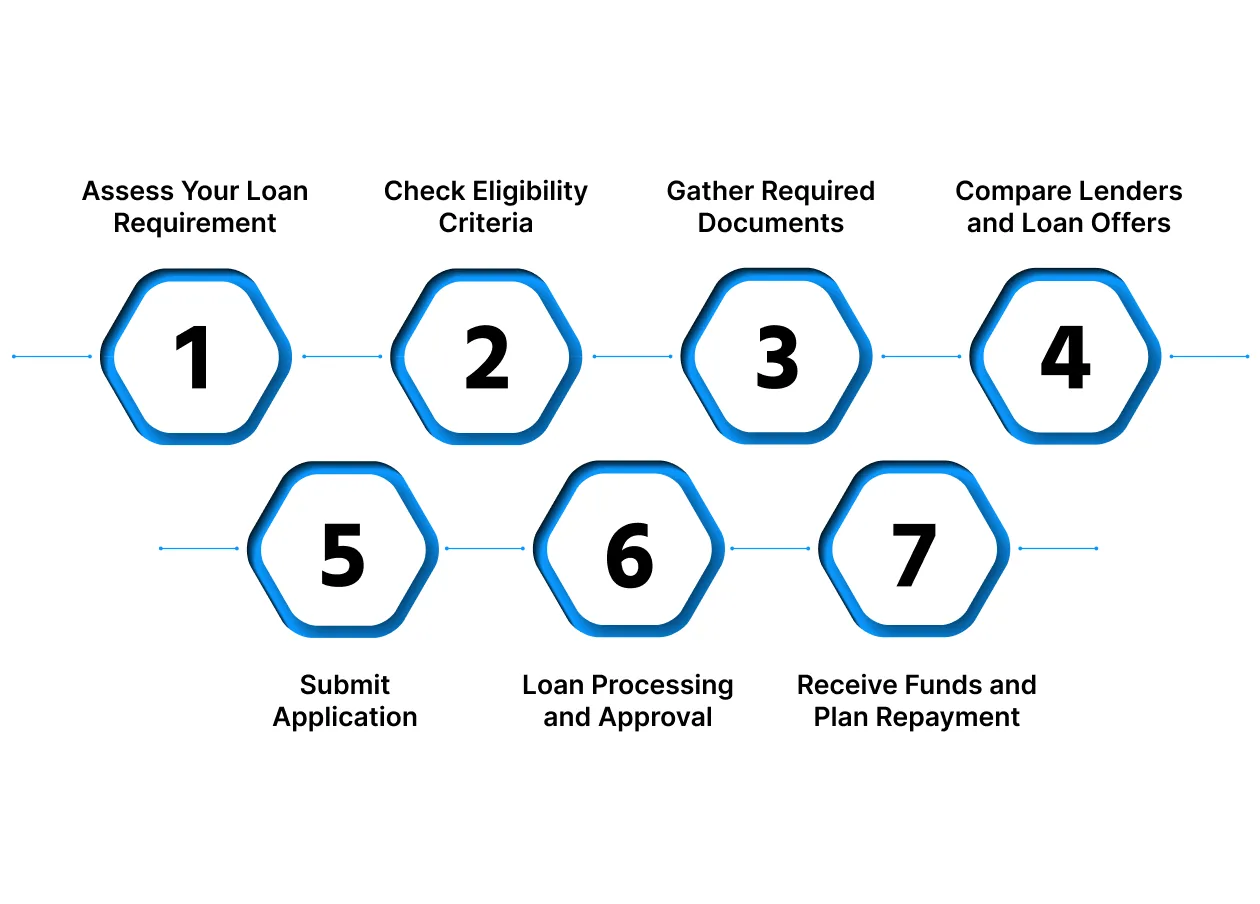

How to Apply for a Business Loan Step by Step

Applying for a business loan can appear complex, but breaking it into clear steps makes the process manageable. Here’s a practical approach that increases your chances of approval:

Step 1: Assess Your Loan Requirement

Determine the exact amount you need and the purpose, whether it’s for expansion, working capital, equipment, or debt consolidation. Knowing this helps you select the right loan type and avoid overborrowing.

Example: A bakery needs ₹5 lakh to buy a new oven and renovate the shop, so it applies for a term loan rather than a revolving line of credit.

Step 2: Check Eligibility Criteria

Different lenders have varying requirements like business vintage, revenue, credit score, and documentation. Ensure your firm meets these criteria before applying.

Example: Banks often require at least 2 years of operational history, while NBFCs may approve loans for startups.

Step 3: Gather Required Documents

Prepare documents such as financial statements, business registration certificates, tax returns, bank statements, and personal identification. Organised paperwork speeds up approval.

Example: A small retail store collects GST registration, 6 months of bank statements, and profit-loss statements before applying.

Step 4: Compare Lenders and Loan Offers

Interest rates, processing fees, repayment terms, and flexibility differ across banks, NBFCs, and fintech lenders. Compare multiple alternatives to find the most cost-effective solution.

Example: One NBFC offers 12% interest with instant approval, while a bank offers 10% but takes 3 weeks for processing.

Step 5: Submit Application

Apply online or offline, depending on the lender’s process. Ensure all documents are accurate to avoid delays.

Step 6: Loan Processing and Approval

Lenders assess creditworthiness, business stability, and repayment capacity. Quick KYC-based platforms may provide instant approvals, while traditional banks take longer.

Step 7: Receive Funds and Plan Repayment

Once approved, funds are transferred to your business account. Set up a repayment schedule that aligns with cash flow to avoid defaults.

Tip: Keep repayment capacity in mind; borrowing more than necessary can lead to unnecessary stress and higher interest costs.

Also Read: Understanding How Positive Cash Flow Works and Why It's Important

How to Boost Your Chances of Getting a Business Loan

Getting a business loan approved isn’t just about meeting eligibility requirements; it’s about presenting your business as credible, financially responsible, and low-risk. Lenders are looking for assurance that their funds will be repaid on time, so taking the right steps beforehand can make all the difference.

1. Maintain Strong Credit Scores

Both your personal and business credit scores matter. A high score signals reliability and reduces perceived risk. Pay bills on time, clear outstanding debts, and avoid defaults to keep your scores in top shape. This can also help you access better interest rates.

2. Organise Your Financial Documents

Lenders expect complete, accurate, and up-to-date financial records. This includes balance sheets, profit-and-loss statements, bank statements, and tax returns. Well-maintained records reflect transparency, demonstrate consistent revenue, and show your ability to manage cash flow effectively.

3. Limit Multiple Applications

Applying to multiple lenders at once may appear desperate and can hurt your credit. Focus on lenders suited to your business type, size, and loan needs to improve approval chances and reduce unnecessary credit checks.

4. Prepare a Solid Loan Proposal

A clear, detailed loan proposal builds confidence with lenders. Include the purpose of the loan, financial projections, repayment plan, and timelines. A structured plan shows you’ve thought through the business strategy and can manage the borrowed funds responsibly.

5. Manage Existing Debt Carefully

High existing debt can signal risk to lenders. Maintain manageable debt levels and ensure timely repayments. Demonstrating financial discipline strengthens your credibility and makes your business appear less risky.

6. Choose the Right Loan Type

Different loans serve different purposes; term loans, business lines of credit, working capital loans, and invoice financing all have distinct uses. Selecting the right one ensures your application aligns with your actual funding needs.

7. Build a Relationship with Your Lender

A strong banking relationship can improve approval odds. Regular communication, timely repayments on current accounts, and engagement with your bank foster trust and can help secure more favourable terms in future applications.

By addressing these key areas, you can improve your loan approval chances, secure better terms, and position your business as reliable and financially savvy.

Short on Funds? Pocketly Can Bridge the Gap

Even the most carefully planned business budgets can face sudden cash flow challenges, whether it’s urgent inventory needs, unexpected equipment repairs, or missed client payments. In these situations, Pocketly provides quick, short-term funding to help you keep operations running smoothly without derailing your business plans.

- Borrow Only What You Need: Loan amounts range from ₹1,000 to ₹25,000, letting you access the exact funds required without taking on unnecessary debt.

- No Collateral or Guarantor Required: Pocketly’s loans are completely collateral-free. You don’t need assets or co-signers, making it accessible to small business owners and startups.

- Fast Approval Process: A quick KYC verification allows for instant decision-making. Say goodbye to long bank queues and paperwork delays.

- Instant Fund Transfer: Once approved, the money is transferred directly to your bank account, ensuring immediate access for urgent business needs.

- Flexible Repayment Options: Choose repayment terms that fit your cash flow. Pocketly lets you plan EMIs without putting unnecessary strain on your monthly finances.

- Transparent Pricing: Interest rates start from 2% per month, with processing fees between 1% and 8%. No hidden charges, so you know exactly what you’re paying.

- Available Anytime, Anywhere: Apply, track, and manage loans through the Pocketly mobile app, 24/7, giving you control and convenience wherever your business takes you.

Pocketly acts as a financial safety net, helping businesses handle short-term funding gaps while keeping long-term goals on track. Used responsibly, it ensures cash flow issues don’t stall growth.

Conclusion

Securing a business loan can feel daunting, but it doesn’t have to be complicated. By understanding the types of loans available, assessing your eligibility, and preparing the necessary documents, you can approach lenders confidently and increase your chances of approval.

It’s all about planning ahead, choosing the right loan type for your business needs, and staying mindful of repayment terms. When used responsibly, a business loan can provide the financial boost you need to manage cash flow, invest in growth, or seize new opportunities without derailing your long-term plans.

Download the Pocketly app now on iOS or Android to explore flexible business loan options, access funds quickly, and manage repayments with clear, transparent terms. With Pocketly, your business can stay financially agile and ready for any growth opportunity.

FAQs

1. What is a business loan?

A business loan is borrowed capital provided by banks or NBFCs to help businesses manage cash flow, invest in growth, or fund operations. Repayment is usually done in EMIs with interest over a fixed period.

2. Who is eligible for a business loan?

Eligibility depends on your business type, age, revenue, credit score, and operational history. Generally, banks and NBFCs require a registered business, financial statements, and proof of income.

3. What documents are needed to apply for a business loan?

Common documents include: business registration, bank statements, income proof, tax returns, identity and address proof of the owner, and financial statements. Some lenders may also require a business plan.

4. How much can I borrow through a business loan?

Loan amounts vary depending on your business size, revenue, and lender policies. Small businesses can often borrow from ₹50,000 to several lakhs, while larger companies may access higher limits.

5. How long does it take to get a business loan approved?

Approval timelines differ by lender. Banks may take a few days to weeks, while digital lenders or NBFCs can provide approvals within 24–72 hours if all documents are in order.