As you enter your 30s, you’re likely balancing career growth, personal goals, and family responsibilities. But have you considered how your financial future might unfold if you don’t start building wealth now? If you’re delaying saving and investing, the longer you wait, the more difficult it becomes to achieve long-term financial security.

It’s easy to get caught up in day-to-day expenses and lifestyle choices, but your 30s are the perfect time to lay the groundwork for your financial future. The good news is, it’s never too late to start, and with the right approach, you can still make significant progress toward financial independence.

In this blog, we’ll explore practical steps you can take now to build wealth in your 30s. From smart budgeting to long-term investing, we’ll show you how to take control of your finances and set yourself up for a secure future.

TL;DR

- Your 30s are the perfect time to build wealth, due to compound interest, career growth, and fewer financial commitments.

- Set clear financial goals, from paying off debt to planning for retirement, and create a budget to consistently save and invest.

- Eliminate high-interest debt quickly, as it holds you back from saving and investing for the future.

- Start investing early with low-cost options like index funds and retirement accounts to benefit from long-term growth.

- To increase wealth faster, focus on growing your income through career advancement, side hustles, and passive income investments.

Why Your 30s Are the Best Time to Start Building Wealth?

Building wealth in your 30s offers unique advantages. Here’s why this decade is the perfect time to focus on your financial future:

Building wealth in your 30s offers unique advantages. Here’s why this decade is the perfect time to focus on your financial future:

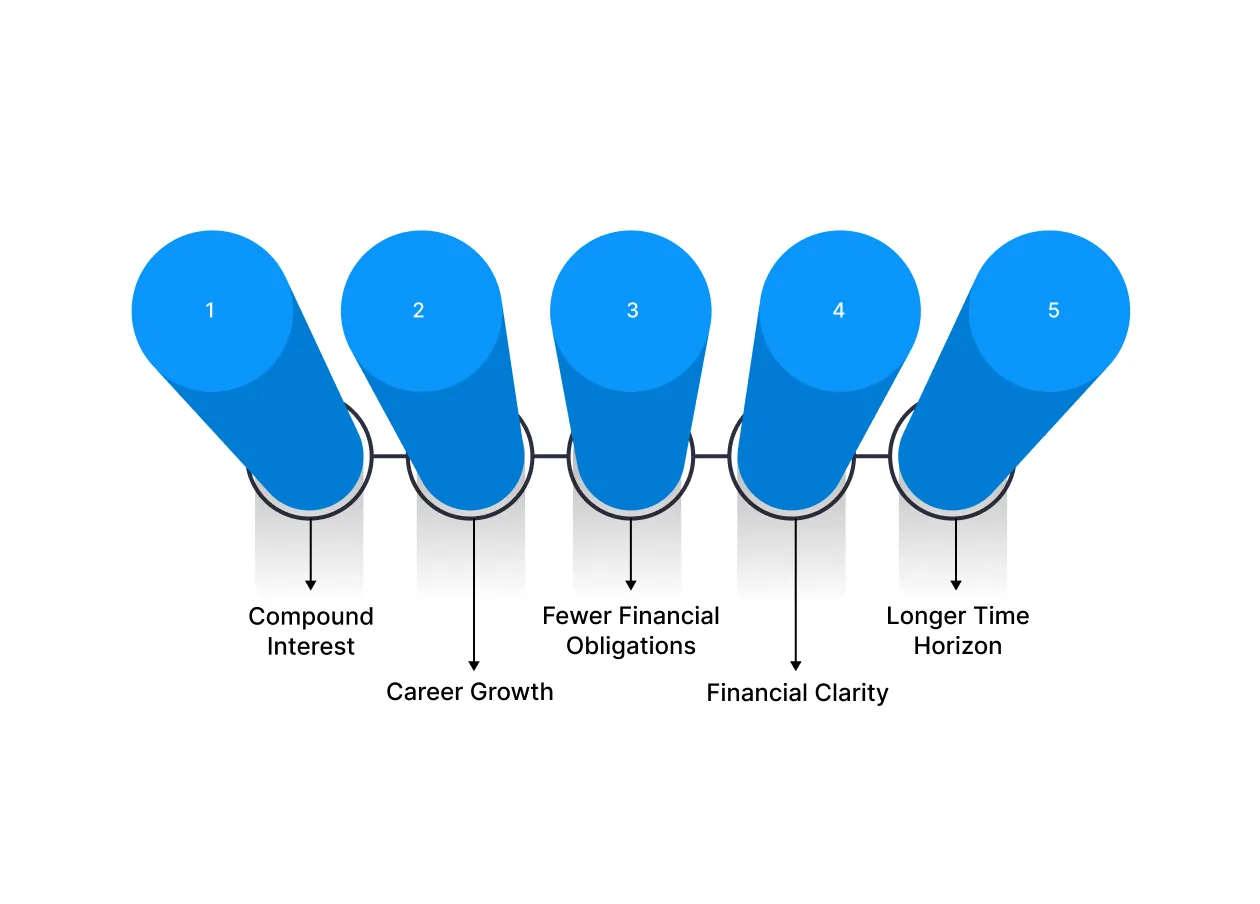

- Compound Interest: The earlier you start investing and saving money, the more you benefit from compound interest. Money invested now has more time to grow.

- Career Growth: By your 30s, you’ve likely gained valuable skills and expertise, which can lead to higher-paying job opportunities. This makes it easier to save and invest more.

- Fewer Financial Obligations: Compared to later years, your 30s might involve fewer long-term financial commitments, such as mortgage payments or children’s education costs. This gives you more freedom to allocate funds towards wealth-building.

- Financial Clarity: By this stage, you have a clearer sense of your goals, whether it’s buying a home, securing retirement, or achieving financial independence. This clarity helps you make more informed, strategic decisions.

- Longer Time Horizon: The sooner you start, the more time you have to take calculated risks with investments, which increases the potential for long-term growth.

By capitalising on these advantages, you set yourself up for financial success later in life, making your 30s a critical period for wealth-building.

1. Set Clear Financial Goals for the Future

Building wealth in your 30s requires more than just saving; it’s about setting clear, actionable financial goals that will influence your decisions and keep you on track. Whether your pursuits are short-term, like paying off debt, or long-term, like retiring comfortably, having a plan is key.

Here’s how to break down your goals:

- Short-Term Goals (1–3 years): Focus on building an emergency fund, paying off high-interest debt, and establishing up a basic budget. These goals help ensure you’re financially stable before tackling bigger aspirations.

- Medium-Term Goals (3–7 years): Think about saving for a down payment on a house or starting to invest for retirement. The goal here is to develop a solid foundation that can grow as your career and life evolve.

- Long-Term Goals (7+ years): Your long-term goals may include retirement savings, financial independence, or a large investment in a business or property. These goals are driven by your current income and investments, and the sooner you start, the better your chances of achieving them.

By clearly defining these goals, you’ll know exactly where to focus your efforts and how to allocate your resources for maximum growth.

2. Create a Budget That Helps You Save and Invest

Building wealth starts with mastering your cash flow. A well-structured budget ensures that you're not only covering your immediate needs but also prioritising savings and investments for the future. The key is finding a balance between living comfortably and securing long-term financial goals.

Here’s how to create a budget that supports wealth-building:

- Track Your Income and Expenses: Start by analysing your monthly income and categorising your expenses, fixed (rent, utilities, insurance) and variable (entertainment, dining out, travel). Use budgeting apps or spreadsheets for accuracy.

- The 50/30/20 Rule: Devote 50% of your income to essentials, 30% to lifestyle spending, and 20% to savings and investments. Adjust these percentages depending on your goals and current financial situation.

- Pay Yourself First: Treat your savings as a non-negotiable expenditure. Set up automatic transfers to your savings or investment accounts as soon as you get your income. This reduces the temptation to spend what you should be saving.

- Cut Back on Unnecessary Expenses: Regularly review your budget for areas where you can cut back. Small savings, like cancelling unused subscriptions or cooking more at home, can add up over time.

- Reevaluate Periodically: Your budget isn’t static. As your income rises or your financial priorities shift, reassess your budget to ensure you're still on track for your wealth-building goals.

A solid budget is the first step in managing your finances effectively, ensuring you’re saving consistently and investing for the future.

Also read: Understanding the Basics of Financial Planning and Its Importance

3. Eliminate High-Interest Debt

One of the biggest barriers to building wealth is high-interest debt. Whether it’s credit card balances, personal loans, or payday loans, these debts can drain your finances and make it harder to save or invest. The sooner you pay off high-interest debt, the more money you can redirect into wealth-building strategies.

Here’s how to eliminate high-interest debt effectively:

- List All Your Debts: Make a list of all your debts, including the interest rates and outstanding balances. This will give you a clear view of what you owe and the impact on your financial situation.

- Pay Off High-Interest Debt First: Focus on paying off debts with the highest interest rates first. This will save you money in the long run. If you have multiple high-interest debts, consider the debt avalanche method, where you target the highest-interest debt while making minimum payments on others.

- Consider Debt Consolidation: If you have several high-interest debts, consider merging them into a single loan with a lower interest rate. This can make your payments more manageable and reduce the total interest you pay.

- Avoid New Debt: While paying off existing debt, make sure to avoid taking on new high-interest debt. Resist the temptation to make large, spurious purchases on credit.

- Refinance Loans if Possible: If you have large loans, such as student loans or a car loan, explore options to refinance at a lower interest rate. This can cut your monthly payment and save you money over time.

By eliminating high-interest debt, you free up more money to save and invest, speeding up the process of building wealth in your 30s.

4. Start Investing Early for Long-Term Growth

One of the most effective ways to accumulate wealth in your 30s is to begin investing early. The sooner you invest, the longer your money has to grow due to the power of compounding. Whether you’re new to investing or looking to optimise your current strategy, the key is consistency and long-term thinking.

Here’s how to get started:

- Beginning with Low-Cost Index Funds and ETFs: If you're new to investing, begin with index funds or exchange-traded funds (ETFs). These provide broad market exposure with minimal fees and are less risky than individual stocks.

- Contribute to Retirement Accounts: In India, National Pension Scheme (NPS) and Employees’ Provident Fund (EPF) are great options to save for retirement, offering tax benefits and compounding growth. Contributing regularly ensures you're building a retirement fund for the long term.

- Systematic Investment Plans (SIPs): Consider investing in mutual funds via SIPs. This strategy help you to invest a fixed amount every month, building wealth gradually while averaging out market volatility.

- Diversify Your Investments: Don't put all your money in one asset class. Expand your investment portfolio by investing in stocks, bonds, real estate, and gold. This spreads risk and increases potential returns over time.

- Reinvest Earnings: Always reinvest dividends and returns to benefit from compounding. Even small returns will grow significantly over the years.

By starting your investments early and consistently, you ensure that your wealth will keep on to grow long after your 30s, setting the stage for a secure and prosperous financial future.

5. Grow Your Income with Side Hustles and Investments

Building wealth isn’t just about cutting back on expenses; it’s also about increasing your income. Whether through career growth, side hustles, or smart investments, boosting your income in your 30s can accelerate your journey to financial independence.

Here’s how to grow your income:

- Upskill and Seek Career Advancement: Invest in improving your skills to enhance your career prospects. Pursue certifications, advanced degrees, or attend workshops that can lead to higher-paying job opportunities and promotions.

- Start a Side Hustle: If your main job doesn’t generate enough income to meet your goals, consider starting a side hustle. Freelancing, online consulting, blogging, or starting an e-commerce store are just a few ways to create additional revenue streams.

- Explore Passive Income Opportunities: Look for ways to earn passive income, such as real estate investments, dividend-paying stocks, or peer-to-peer lending. These sources of income can increase over time, requiring little effort once established.

- Invest in High-Return Assets: Invest in assets that can provide higher returns over time. Equity mutual funds, stocks, and cryptocurrencies (if you’re comfortable with the risks) can boost your wealth faster than traditional savings accounts.

- Monetise Your Skills and Expertise: Share your knowledge through online courses, webinars, or ebooks. Platforms like Udemy allow you to develop and sell content based on your expertise, earning passive income.

By actively growing your income, you increase the amount available for saving and investing, setting you up for faster wealth accumulation in your 30s.

6. Protect Your Wealth with Insurance

As you build wealth in your 30s, it’s crucial to protect it from random events that could derail your financial progress. Insurance provides a safety net, to assure that you’re financially secure even in the face of unforeseen conditions such as health issues, accidents, or loss of income.

Here’s how to protect your wealth with insurance:

- Health Insurance: Health insurance is required to cover medical expenses, which can be expensive and financially draining. With adequate health coverage, you prevent medical bills from consuming your savings or derailing your investment goals.

- Life Insurance: If you have dependents, life insurance ensures that your loved one is financially secure in case of your untimely demise. Term life insurance offers affordable coverage, while whole life insurance can be an investment as well.

- Disability Insurance: If you’re unable to work due to illness or injury, disability insurance ensures that you still get a portion of your income, protecting your savings and allowing you to continue contributing to your financial goals.

- Home Insurance: If you own a home, property insurance protects your biggest asset from risks such as fire, theft, or natural disasters. This ensures that any loss won’t significantly impact your wealth.

- Auto Insurance: Protect your vehicle and yourself by investing in comprehensive auto insurance. It covers both third-party liabilities and damages to your own vehicle, preventing unexpected costs from affecting your finances.

By securing the right types of insurance, you safeguard the wealth you’re building and ensure that unexpected events don’t set you back financially.

Also read: 6 Simple Budgeting Tips for Better Money Management

How to Stay on Track: Pitfalls to Avoid While Building Wealth

While your 30s are a great time to focus on building wealth, there are common pitfalls that can derail your progress. Avoiding these mistakes will help you remain on track and ensure you’re building a solid financial foundation for the future.

While your 30s are a great time to focus on building wealth, there are common pitfalls that can derail your progress. Avoiding these mistakes will help you remain on track and ensure you’re building a solid financial foundation for the future.

Here’s what to watch out for:

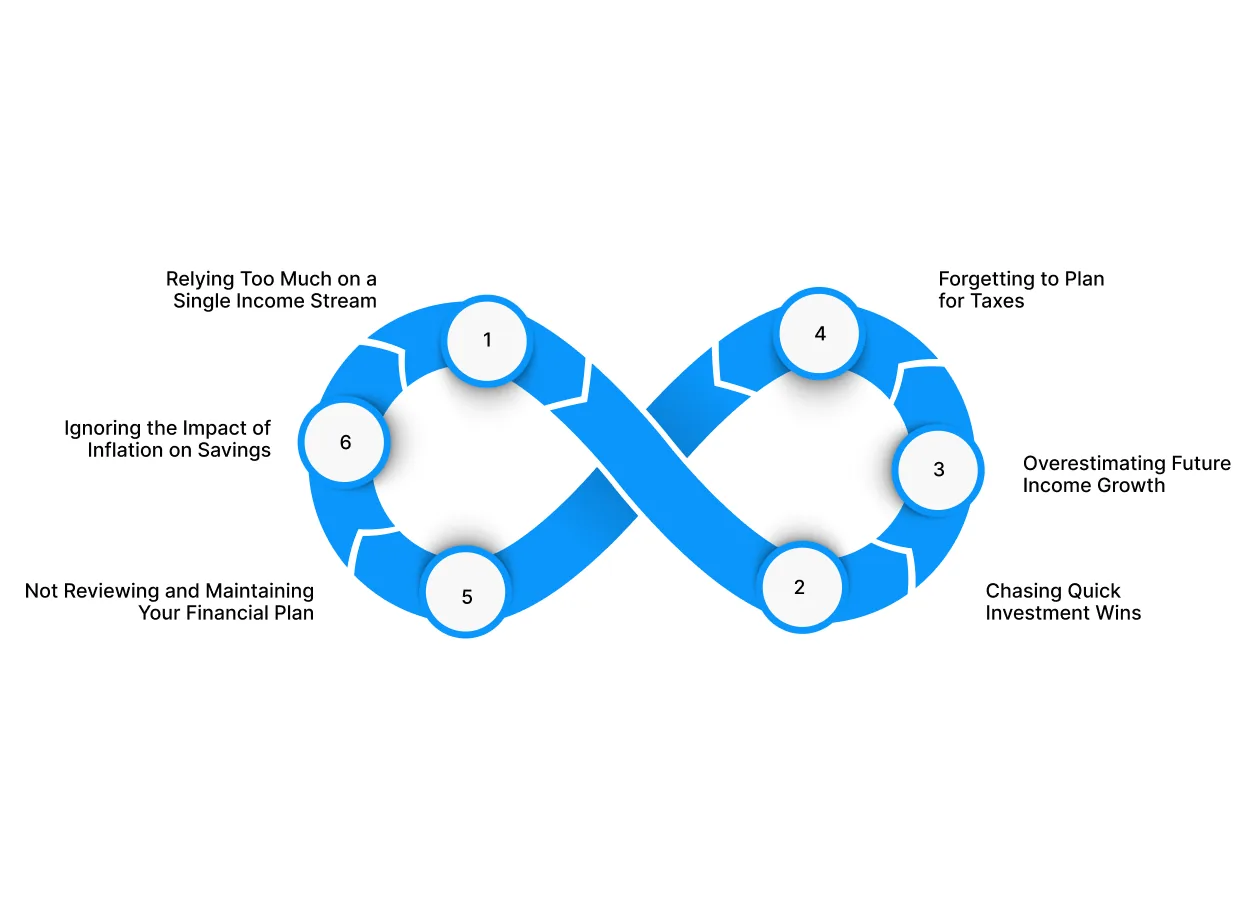

1. Relying Too Much on a Single Income Stream

In your 30s, relying solely on your primary job for income can limit your wealth-building potential. While salary increases can help, they often aren’t enough to achieve significant wealth. Diversifying income sources through side hustles, investments, or passive income streams is key to growing wealth faster.

Instead of depending entirely on your salary, consider exploring ways to generate additional income, whether through freelance work, online businesses, or investments in real estate or stocks. Having multiple income streams helps you build wealth more securely and quickly.

2. Chasing Quick Investment Wins

The lure of quick returns can be strong, especially when you hear stories of people making large profits from speculative investments. However, chasing short-term gains through high-risk investments like day trading or betting on volatile stocks can lead to significant losses and set you back financially.

Instead, focus on building a varied investment portfolio with a long-term strategy. Stick to low-risk, consistent investments such as index funds, retirement accounts, and real estate to grow wealth steadily.

3. Overestimating Future Income Growth

It’s easy to assume that your income will continue to rise at a predictable pace as you progress in your career. However, salary increases can slow down, or you may face unexpected career changes. Relying too much on future income growth can cause you to overspend or neglect important financial planning, especially if you don’t plan for possible job loss or income reduction.

Instead, make financial decisions based on your current income level, and be conservative with your spending and investing. Always plan for potential setbacks and have a backup plan for economic uncertainty.

4. Forgetting to Plan for Taxes

While it’s important to save and invest, neglecting taxes can eat into your wealth in the long run. Investments in certain accounts, like mutual funds or stocks, can be liable to capital gains tax, and your salary is taxed regularly as well.

Ensure that your financial strategy includes tax planning to minimise your liabilities. Use tax-saving tools like 80C deductions, consider tax-efficient investment options like ELSS funds, and speak with a financial advisor about how to structure your portfolio to minimise tax burdens.

5. Not Reviewing and Maintaining Your Financial Plan

Your financial goals and circumstances can change rapidly in your 30s. Not regularly reviewing your wealth-building strategy means you might miss opportunities or fail to adjust for changes in your life, such as marriage, children, career shifts, or unexpected expenses.

Set a financial review schedule, whether monthly or quarterly, to assess your progress, revise goals, and make adjustments to your budget, investments, and savings plans as needed.

6. Ignoring the Impact of Inflation on Savings

Inflation gradually decreases the purchasing power of your money, making it essential to factor it into your savings and investment strategy. Keeping money in a savings account or low-interest instruments can mean your money loses value over time.

Invest in assets that rise faster than inflation, such as stocks, bonds, or real estate. Diversifying your portfolio with inflation-resistant assets ensures your wealth keeps up with the rising cost of living.

Facing Financial Hurdles in Your 30s? Pocketly Offers Quick Solutions

Building wealth in your 30s requires focus, strategy, and discipline. However, unexpected expenses or financial gaps can sometimes derail your progress. Whether it’s a sudden cash flow issue, an urgent bill, or an unexpected investment opportunity, Pocketly is here to help you stay on track with quick, hassle-free financial solutions.

Here’s why Pocketly is the perfect partner for your financial journey:

- Borrow only what you need: Loans from ₹1,000 to ₹25,000, designed to meet your needs without overextending your finances.

- No collateral required: No need for physical assets or guarantors, making it easier to access funds quickly.

- Fast approval: Instant KYC verification and quick decision-making ensure you get the funds you need without delays.

- Instant transfer: Funds are directly credited to your bank account as soon as the loan is approved.

- Flexible repayment options: Choose a repayment plan that suits your budget and cash flow.

- Clear, transparent pricing: Interest rates starting at 2% per month and processing fees between 1% and 8%.

- Available 24/7: Access funds at any time through the easy-to-use Pocketly app.

With Pocketly, you can continue building your wealth without worrying about sudden financial setbacks. So, when life throws challenges your way, Pocketly gives you the flexibility and support you need to keep moving forward.

Conclusion

Building fortune in your 30s is a crucial step toward protecting your financial future, but it requires a long-term approach and consistent effort. By focusing on smart savings, debt management, and investing early, you set yourself up for success in the years to come.

Regularly reviewing your finances and adjusting as your goals evolve will help you stay on track. If you find yourself facing unforeseen financial challenges, don't panic; small adjustments now can help prevent larger setbacks later. Quick solutions like short-term loans can help you bridge gaps without disrupting your wealth-building progress.

Start building your wealth today, and remember, every small step counts toward a more prosperous and secure future. If you need quick financial support, download the Pocketly app today on iOS or Android for easy access to funds and keep your financial goals intact.

FAQs

1. What’s the best way to build wealth in your 30s?

The best approach is a combination of consistent saving, investing early, eliminating high-interest debt, and increasing your income through side gigs or career advancement.

2. How much should I save in my 30s?

Ideally, aim to save 20–30% of your income in your 30s. As your income grows, you should increase this percentage to maximise your wealth-building potential.

3. Is it too late to start investing in my 30s?

It’s never too late to start investing. The earlier you begin, the better, as compounding works more effectively over time. Even starting in your 30s gives you a good advantage.

4. Should I prioritise debt repayment or investing first?

Paying off high-interest debt should be the priority. Once you clear high-interest loans or credit card debt, you can allocate more funds to investing for long-term wealth growth.

5. Which investment option is best for long-term wealth?

A diversified portfolio of equities, index funds, and retirement accounts like PPF or NPS typically offers good long-term returns. The key is to stay invested over time and avoid trying to time the market.