You check your bank account after a few months and notice the interest earned is lower than expected.

The rate may look decent, but the actual returns often feel underwhelming because the interest rate you see isn’t the interest you actually earn.

Banks calculate interest based on how your balance changes over time, not just the total amount in your account. Factors like daily balance, timing of deposits, and withdrawals all affect the final amount credited.

Without understanding how interest rates are calculated by banks, it becomes difficult to make sense of your earnings or improve them.

This blog explains how bank interest is calculated, what actually reduces your returns, and how to manage your balance more effectively.

Key Takeaways

-

The interest rate you see is only part of the picture, because actual earnings depend on balance, timing, and calculation method.

-

Savings account interest is calculated on the daily closing balance, so even small withdrawals can reduce what you earn.

-

How long your money stays in the account matters as much as the amount, especially when balances keep changing.

-

Different bank products follow different interest methods, which change how returns are earned or paid.

-

Understanding the calculation helps you manage your money better, instead of relying only on the headline rate.

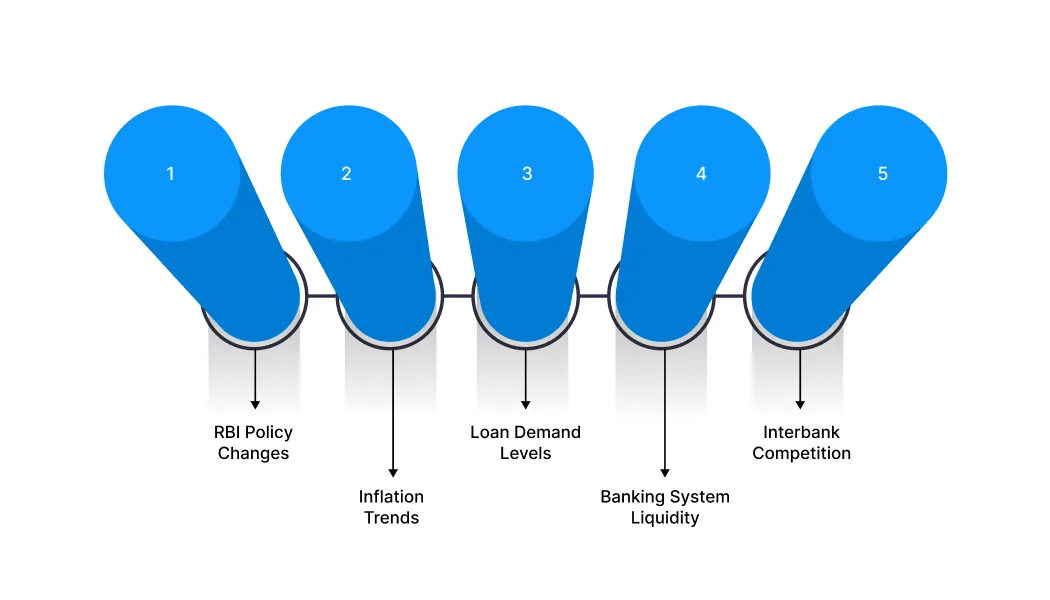

How Banks Decide Interest Rates

Before understanding how interest is calculated, it is important to know how banks decide the rate itself. The percentage you see is not random. It is influenced by multiple economic and internal factors.

Here are the key elements that affect how banks set interest rates:

-

Central bank policies (RBI influence): Banks adjust their rates based on policy rates like the repo rate set by the Reserve Bank of India. When the RBI increases or decreases rates, banks usually follow.

-

Inflation levels: Higher inflation often leads to higher interest rates, as banks need to maintain real returns. Lower inflation can result in reduced rates.

-

Demand for loans: If more people are borrowing, banks may increase interest rates. If demand is low, they may offer better rates to attract borrowers or deposits.

-

Liquidity in the banking system: When banks have excess funds, they may lower interest rates. If funds are limited, rates may increase to attract more deposits.

-

Competition among banks: Banks often adjust their rates to stay competitive. Higher rates can attract more customers, especially for savings accounts and fixed deposits.

For example, if the RBI increases the repo rate, banks may increase both lending and deposit rates. This affects how much you earn on savings and how much you pay on loans.

Interest rates are influenced by broader economic conditions, not just bank policies. Understanding this helps explain why rates change over time.

Also read: Interest Rates in India 2026: How They Affect Loans & Savings

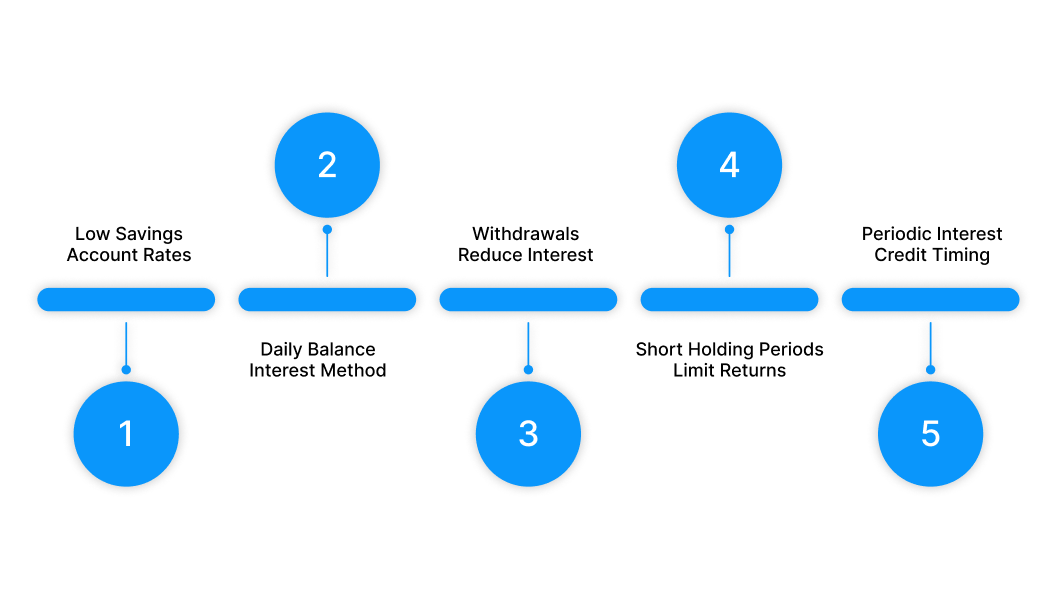

How Banks Calculate Interest in Savings Accounts

Most savings accounts in India follow the daily balance method to calculate interest. This means the interest is based on the amount you have in your account at the end of each day, not just the average monthly balance.

Here is how it works:

-

Interest is calculated daily: At the end of each day, the bank checks your account balance and applies the interest rate for that day.

-

Accumulates over time: The interest earned each day is added up over the month or quarter.

-

Credited periodically: Even though it is calculated daily, the total interest is usually credited monthly or quarterly.

-

Balance changes affect earnings immediately: Deposits increase your interest from that day onward, while withdrawals reduce it from the day they happen.

For example, if you maintain a higher balance for more days in a month, you will earn more interest. If you withdraw funds frequently, your effective earnings will be lower.

In savings accounts, it is not just how much money you have, but how long you keep it in the account that determines your interest earnings.

Bank Interest Formula and What It Means in Practice

Once you understand the daily balance method, the actual calculation becomes straightforward. Banks use a simple formula to determine how much interest you earn over a period.

Interest = (Daily Balance × Interest Rate × Number of Days) ÷ 365

This formula converts the annual interest rate into a daily rate based on how long your money stays in the account.

Here is what each part means:

-

Daily Balance: The amount in your account at the end of each day.

-

Interest Rate: The annual rate offered by the bank (for example, 3% or 4% per year).

-

Number of Days: The number of days your money stays in the account at that balance.

-

365: Used to convert the annual rate into a daily rate.

How to Think About It Simply

-

The bank breaks your annual interest rate into a daily rate

-

Applies that rate to your daily balance

-

Adds up the interest for each day

Even though interest is shown as an annual percentage, it is actually calculated daily based on how long your money stays in the account.

Also read: Credit vs Loan in India: Key Differences & Smart Choice (2026)

Simple Example of How Bank Interest Is Calculated

The formula becomes much easier to understand when you apply it to a real situation.

Example

-

Account balance: ₹10,000

-

Interest rate: 4% per year

-

Number of days: 30

Step-by-step calculation

-

Convert the annual rate into a daily rate

4% ÷ 365 = 0.01096% per day -

Calculate daily interest

₹10,000 × 0.01096% = ₹1.096 per day -

Calculate total interest for 30 days

₹1.096 × 30 = ₹32.88

Total interest earned = ₹32.88

What This Shows

-

Interest builds slowly because it is calculated daily

-

Higher balance or more days increases earnings

-

Frequent withdrawals reduce the total interest

Even a small change in how long money stays in your account can impact your final interest, because the calculation is based on daily balance, not just the total amount.

If you are comparing short-term borrowing options, understanding how interest builds over time can help you choose a smaller, more manageable loan through platforms like Pocketly.

How Interest Calculation Changes Across Different Accounts

Not all bank accounts calculate interest in the same way. The method changes depending on the type of product, which directly affects how much you earn or pay.

Here is how the main types compare:

Savings Account

-

Calculation method: Daily balance

-

Interest type: Simple interest (calculated daily, credited periodically)

-

Returns: Lower compared to other options

Best for liquidity and everyday use, but not for maximising returns.

Fixed Deposit (FD)

-

Calculation method: Compound interest

-

Interest type: Compounded quarterly, monthly, or annually

-

Returns: Higher than savings accounts

Loans (Personal, Home, etc.)

-

Calculation method: Reducing balance method

-

Interest type: Charged on outstanding principal

-

Impact: You pay interest instead of earning it

As you repay the loan, the interest reduces because the principal decreases.

Key Difference

-

Savings account → interest based on daily balance

-

Fixed deposit → interest grows through compounding

-

Loans → interest is a cost, calculated on remaining principal

The way interest is calculated depends on the product. Understanding this helps you choose where to keep your money or how to manage borrowing more effectively.

How to Increase Your Bank Interest Earnings

Once you understand how interest is calculated, small changes in how you manage your account can improve your returns.

Here is what actually makes a difference:

-

Keep a higher balance for longer periods: Since interest is calculated daily, maintaining a stable balance increases total earnings

-

Avoid frequent withdrawals: Every withdrawal reduces your balance immediately, lowering interest from that day onward

-

Deposit money earlier in the cycle: The earlier funds are added, the more days they earn interest

-

Choose accounts with better rates: Even a small difference in interest rate can impact your earnings over time

-

Move idle funds to better options when needed: If money is not required immediately, shifting it to higher-yield options can improve returns

For example, depositing money at the beginning of the month and leaving it untouched will generate more interest than adding the same amount later or withdrawing it frequently.

In simple terms, maximising interest is less about chasing higher rates and more about managing balance and timing effectively. And when the need is immediate rather than long-term, choosing a short-term option like Pocketly can help you manage the gap without taking on more credit than necessary.

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

How Pocketly Fits When the Need Is Small and Time-Sensitive

Once you understand how banks calculate interest, it becomes easier to look at borrowing more carefully too. The same factors still matter. The amount, the rate, and the repayment period all shape the final cost.

That is why borrowing should not be judged only by how quickly the money arrives. It should also be judged by how much interest builds over time and whether the loan structure matches the actual need.

Pocketly fits into this situation when the requirement is short-term and limited.

Here is how it helps in this context:

-

Smaller loan amounts keep borrowing aligned with the actual need instead of creating excess debt

-

Shorter repayment cycles reduce the chance of carrying interest for longer than necessary

-

Interest starts from around 2% per month, with processing fees typically ranging from 1% to 8%, depending on the profile and loan amount

-

Cost is visible upfront, so you can understand the repayment impact before making a decision

If your requirement is small and immediate, check your eligibility on Pocketly, review the total borrowing cost, and choose a short-term option that fits your need. Download the Pocketly app today on Android or iOS!

FAQs

Q: How are interest rates calculated by banks on savings accounts?

Banks calculate interest using the daily balance method, where interest is applied to your account balance at the end of each day. The total is then credited monthly or quarterly.

Q: What formula do banks use to calculate interest?

Banks typically use the formula: Interest = (Balance × Rate × Time) ÷ 365. This converts the annual rate into a daily calculation.

Q: How can I manage borrowing costs better for short-term needs?

Keeping the loan amount small and the repayment period short can help reduce total interest. Options like Pocketly are designed for this, where borrowing stays aligned with short-term needs instead of long tenures.

Q: Do all banks use the same method to calculate interest?

Most banks use the daily balance method for savings accounts, but rates and credit frequency may vary. Other products like FDs and loans use different calculation methods.

Q: Can I increase my bank interest without changing the rate?

Yes, maintaining a higher and stable balance can improve your earnings. Timing deposits and avoiding frequent withdrawals also helps.