Do you ever reach the end of the month, look at your balance, and genuinely wonder, “Where did all my money go?” You remember a few big payments, but not the quiet stream of food orders, quick cab rides, late-night online shopping, and “free trial” subscriptions that never got cancelled.

That is where the real problem hides. It rarely feels like you are being careless. Each spend feels small, deserved, or urgent in the moment. The stress only appears later, when UPI declines at the shop, rent feels heavier than it should, or you end up borrowing a little “just this once” from friends or family. Over time, this pattern chips away at savings, delays goals, and keeps you stuck in the same month-end scramble.

The good news is that this is a pattern you can change. With a clear understanding of why wasteful spending habits form, and a few practical systems that work in real life (not just on spreadsheets), you can protect your cash flow without cutting out everything you enjoy. In this blog, we will unpack what wasteful spending really looks like, how to spot it early, and the habits that help you finally break the cycle.

TL;DR

- Wasteful spending is about small, unintentional purchases that accumulate and disrupt cash flow (e.g., food delivery, unused subscriptions, cabs for short distances).

- The habit forms through low awareness, digital convenience, emotional triggers, and peer influence, often leading to overspending.

- Breaking the cycle involves tracking every spend for 30 days, categorising purchases, setting weekly spending limits, and introducing intentional guardrails like 24-hour purchase pauses.

- Benefits of cutting wasteful spending include smoother month-end cash flow, reduced reliance on credit, timely bill payments, and lower financial anxiety.

- For unexpected costs, Pocketly provides quick, small loans to bridge cash flow gaps without penalties or borrowing from friends.

What Does Wasteful Spending Really Mean?

Wasteful spending isn’t about enjoying life or buying things you care about. It’s when money leaves your account without intention or lasting value.

It usually shows up in small, repeatable behaviours like:

- Ordering food often despite having groceries at home

- Taking cabs for short distances

- Keeping subscriptions you don’t use

- Buying discounted items that sit unused

These expenses don’t feel serious in the moment. They feel convenient, quick, or justified. The issue is the cumulative impact.

There’s a simple distinction:

- Intentional spending: planned, meaningful, adds value

- Wasteful spending: unplanned, passive, driven by habit or impulse

Wasteful spending hides in convenience, boredom, and frictionless payments. And it’s hard to catch because each transaction looks small until the month-end balance tells a different story.

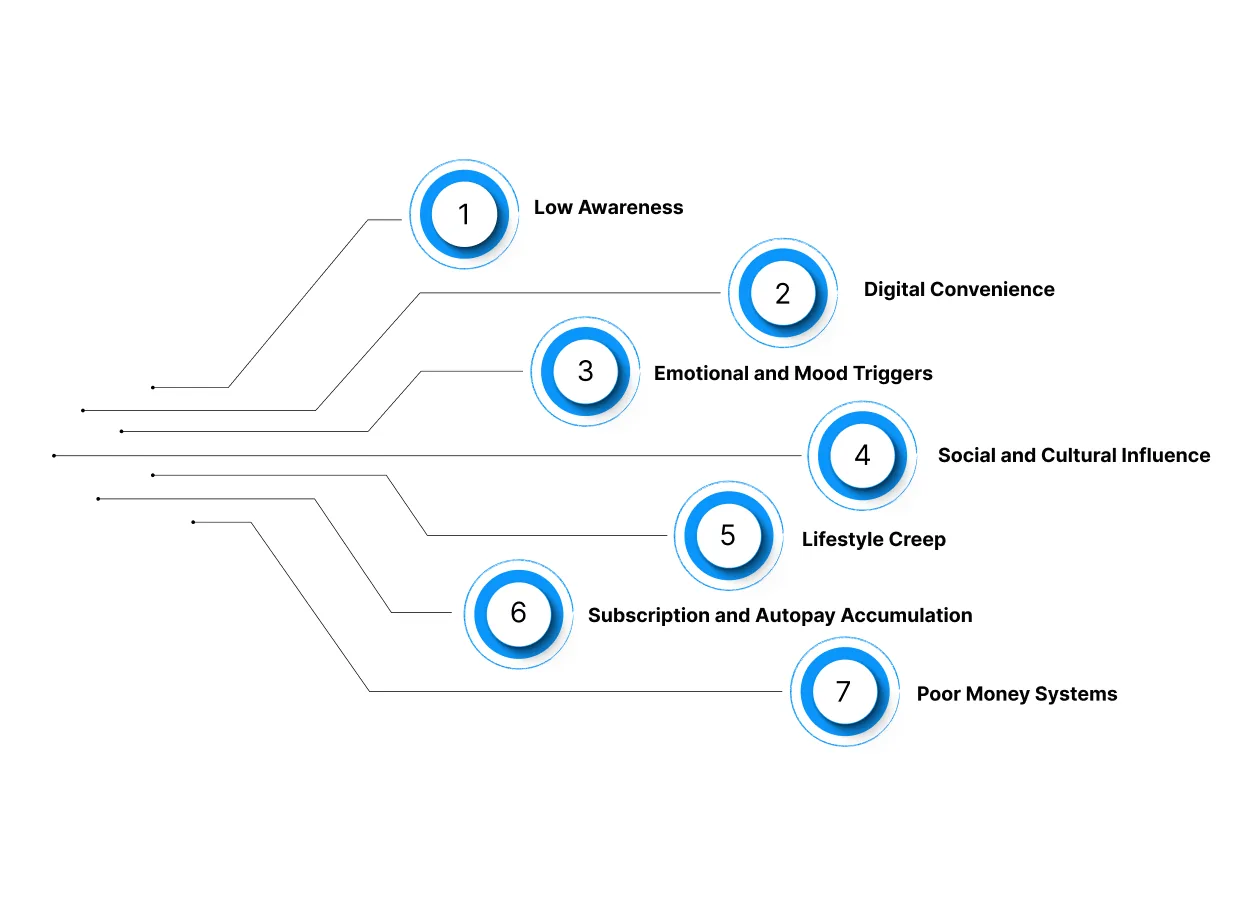

Why People Spend Money Wastefully? A Behavioural Model

Wasteful spending rarely comes from a single bad choice. It usually emerges from multiple behavioural layers that interact quietly in day-to-day life. When we map those layers, the pattern becomes easier to understand and eventually change.

1. Low Awareness (Visibility Layer)

Money leaks when people don’t know where it’s going.

Drivers include:

- No expense tracking

- No monthly review of bank statements or UPI history

- Payments spread across cash, UPI, cards, BNPL (difficult to add up mentally)

When you have no visibility, you don’t notice patterns until the month-end balance dips.

2. Digital Convenience (Friction Layer)

Spending used to require effort. Now it’s instant.

Examples:

- One-tap checkout on e-commerce apps

- Food delivery apps with saved addresses and cards

- Cab apps that remove cash handling

- UPI that eliminates payment hesitation

- BNPL that delays the pain

Lower friction equals higher frequency.

3. Emotional and Mood Triggers (Psychology Layer)

People often spend to change how they feel or avoid discomfort.

Common triggers:

- Stress → comfort food or treats

- Boredom → online browsing and buying

- Fatigue → food delivery instead of cooking

- Bad day at work → impulse shopping

These purchases often feel justified in the moment and invisible later.

4. Social and Cultural Influence (Social Layer)

Spending behaviours are shaped by peers and environments.

Examples:

- Eating out to participate in social plans

- Gifting during festivals and birthdays

- Travel plans for group trips

- Upgrading gadgets to match peer standards

Here, money moves not for personal value but social belonging.

5. Lifestyle Creep (Earnings Layer)

As income increases, spending increases automatically.

Typical pattern:

- More cabs, fewer buses

- More eating out, fewer home-cooked meals

- More gadgets and accessories

- Premium subscriptions over free ones

The shift is quiet and often goes unnoticed.

6. Subscription and Autopay Accumulation (Commitment Layer)

Subscriptions are sticky by design.

Common cases:

- OTT platforms

- Music apps

- Fitness or coaching apps

- Cloud storage upgrades

- Free trials that convert silently

Since the payment is automatic, the user feels no immediate loss.

7. Poor Money Systems (Structure Layer)

Without systems, money flows based on emotion instead of intention.

Missing systems often include:

- No savings rule

- No weekly caps

- No category limits

- No bill calendar

- No emergency buffer

The absence of structure allows wasteful behaviour to become the default.

Signs You Have a Wasteful Spending Habit (Self-Assessment Checklist)

Many people assume they’re good with money until they review their month-end balance. This quick scorecard helps you assess whether wasteful spending is affecting your cash flow.

Check how many apply to you:

- You often wonder where your money went despite no major purchases

- You run out of money or feel stressed before the salary date

- You order food despite having groceries at home

- You pay for subscriptions you rarely use

- You rely on cabs for short, repeatable distances

- You frequently borrow small amounts to cover the last week of the month

- You skip or delay bills because “there isn’t enough right now”

- You don’t have a monthly savings or emergency buffer

- You buy discounted items that end up unused

- You feel guilt or regret after discretionary purchases

- You have multiple BNPL or credit transactions for low-value items

- You avoid checking your bank balance or UPI history

- You haven’t reviewed your expenses in the last 30 days

Interpretation:

- 0–3 checks: Spending is mostly intentional

- 4–7 checks: Spending inconsistencies are disrupting cash flow

- 8+ checks: Wasteful spending habits are likely hurting financial stability

This scorecard is not about blame. It’s about visibility. Wasteful spending becomes harder to break when you don’t know what the pattern looks like. Visibility is the first step toward change.

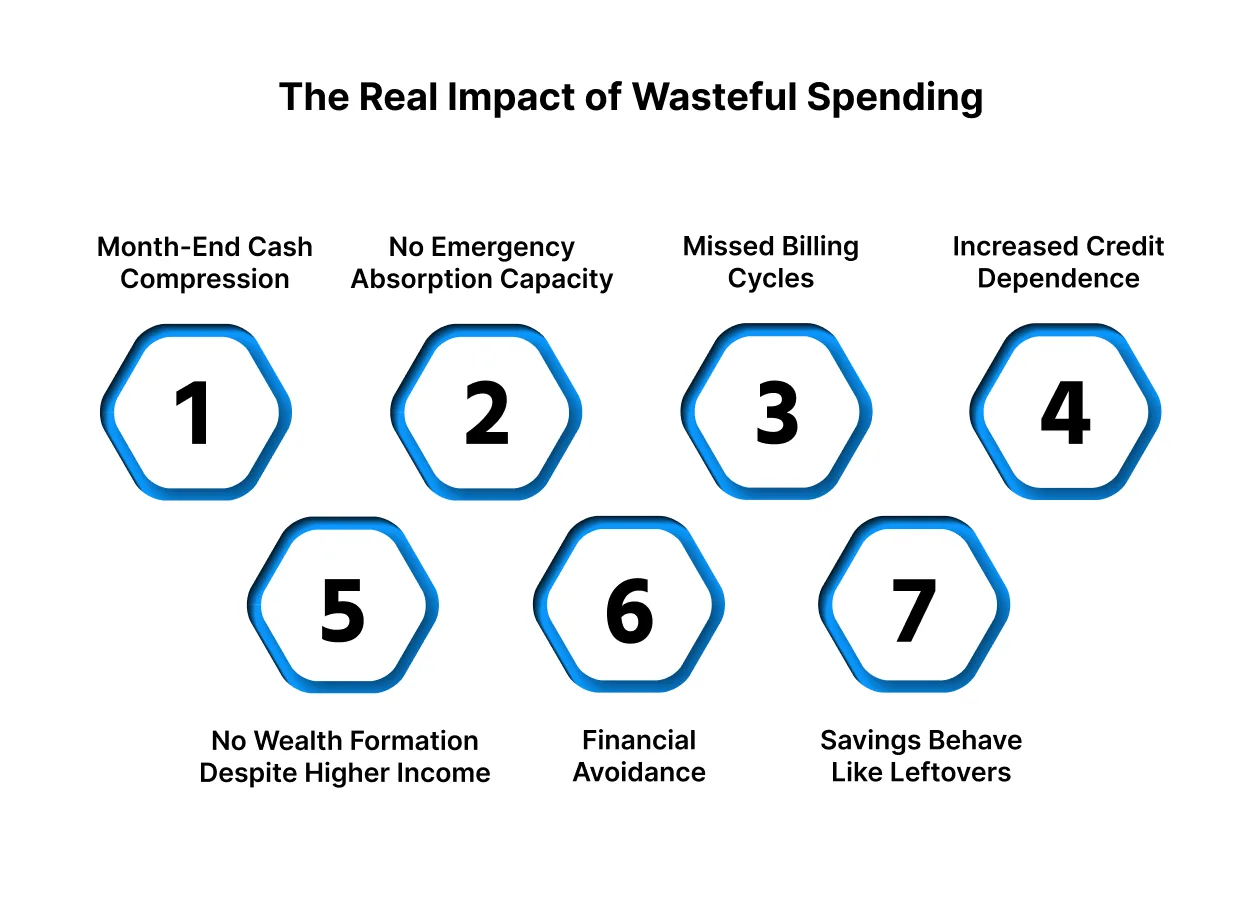

The Real Impact of Wasteful Spending

Wasteful spending rarely feels urgent at the transaction level because the amounts are small. The impact appears at the system level, how money flows through the month, how bills get prioritised, how credit gets used, and how stress accumulates.

Below are the key risks and how to counter them with practical systems instead of vague advice.

Risk 1: Month-End Cash Compression

Cash flow dries up before salary hits. Essentials (rent, bills, groceries) start competing with leftover discretionary expenses from earlier in the month.

Side effects: borrowing small amounts from friends, pushing payments, skipping outings, or reducing essentials.

Mitigation Logic: Break the month into weekly spending buckets instead of one 30-day pool. Weekly caps create smaller decision windows and prevent overspending in the first 10 days. This works better than monthly budgets because corrections happen faster.

Risk 2: No Emergency Absorption Capacity

When an unplanned cost appears (minor medical issue, travel, repairs), there’s no buffer. The expense feels larger than it actually is because there’s no cushion.

Side effects: high-cost borrowing, using credit for essentials, or delaying the problem until it gets worse.

Mitigation Logic: Build a micro-buffer instead of chasing a “perfect emergency fund.” Starting with ₹500–₹2,000 per month builds resilience over time. Small buffers matter because most emergencies at the individual level are small (transport, health check, minor repairs).

Risk 3: Hidden Penalties and Missed Billing Cycles

Bills get pushed to week 4 or into the next month due to low liquidity. Late utility bills, phone bills, and credit card dues silently increase the cost of living.

Side effects: reconnection charges, late fees, and credit score impact (in case of cards).

Mitigation Logic: Move fixed expenses to auto-pay (or calendar reminders) at the start of the month. Automation protects recurring obligations from discretionary spending and reduces penalty leakage.

Risk 4: Increased Credit Dependence for Small Categories

Credit cards, BNPL, or instant loans start covering tiny amounts (food delivery, cabs, shopping). This shifts the mental model from “Do I have the money now?” to “I’ll deal with it later.”

Side effects: repayment clusters later in the month, shrinking future liquidity.

Mitigation Logic: Reserve credit for planned, high-utility purchases. For everyday micro-spends, use balance-linked modes (UPI/cards without credit) so spending pressure remains tied to reality.

Risk 5: No Wealth Formation Despite Higher Income

Income grows, spending grows faster. This is classic lifestyle creep: better phone, better commute, more takeout, more subscriptions, all justified individually.

Side effects: no savings, no investments, delayed goals (travel, upskilling, relocation).

Mitigation Logic: Use a pay-yourself-first rule (e.g., 10%–20% auto-transfer to savings/investments on salary day). Behaviourally, removing money from the pool early reduces lifestyle creep without forcing extreme restrictions.

Risk 6: Financial Avoidance and Decision Paralysis

People stop checking their bank balance, UPI history, or statements because it triggers discomfort. Avoidance leads to delayed action, which worsens everything else.

Side effects: poor decisions made under stress, missed opportunities, and unresolved debt patterns.

Mitigation Logic: Run a 10-minute weekly review. Not a spreadsheet. Just a simple look at transactions, upcoming bills, and remaining balance. Visibility reduces anxiety and improves decisions over time.

Risk 7: Savings Behave Like Leftovers (Instead of Design)

Savings are treated as “whatever is left at the end of the month,” which often rounds down to zero.

Side effects: dependency on salary cycles, no progress on medium/long-term goals.

Mitigation Logic: Convert savings from “residual” to pre-allocated. If money moves out on Day 1, everything else adapts. If money stays in the account, spending expands to fill it.

Common Triggers That Lead to Wasteful Spending

Wasteful spending isn’t random. It follows predictable triggers that influence behaviour throughout the month. Mapping these triggers helps you detect when you’re most vulnerable to spending without intention.

Here are the most common trigger buckets:

1. Convenience Triggers

Convenience is one of the strongest drivers of wasteful spending today. With food delivery apps, cabs, and one-tap checkout, spending takes less than a few seconds. Most people don’t realise how often they choose convenience over intention. Cooking feels slow, walking feels tiring, and comparing prices feels like effort, so we default to the easiest option.

For example, if you check your UPI history at the end of the month, you might notice that short cab rides, quick snacks, and weekday takeaways cost more than you expected. None of these choices feels unnecessary at the time, but together they create a pattern. When convenience becomes the default, spending becomes automatic, not deliberate.

2. Emotional Triggers

Spending is often an emotional response rather than a rational choice. People buy things to relieve stress, boredom, frustration, or fatigue. A long workday can justify food delivery, a dull weekend can lead to online shopping, and a small bad moment can trigger a “treat yourself” purchase. These habits feel harmless individually, but they quietly shape financial behaviour.

If you look at your spending during stressful weeks, you might notice you order more food or shop more late at night. The emotional relief is temporary, but the financial impact extends into the end of the month. When emotions drive spending, money moves without value; it just fills a feeling for a moment.

3. Social Triggers

We underestimate how much our spending is influenced by the people around us. Eating out with colleagues, saying yes to group trips, or buying gadgets because friends upgraded are all examples of social spending. The goal isn’t the purchase itself, it’s belonging, matching, or avoiding missing out.

For example, you might not be interested in a new phone until everyone in your group discusses their upgrades. Or you might not plan to dine out, but join colleagues after work because it feels natural. These moments aren’t wrong, but when they happen frequently, they override personal budgets and priorities. Social spending feels justified in the moment, but becomes expensive over time.

4. Timing Triggers

Spending behaviour shifts depending on where you are in the salary cycle. At the beginning of the month, people feel financially comfortable, which leads to higher discretionary spending, eating out, shopping, subscriptions, and outings. By the third or fourth week, the same person feels restricted and stressed, even though their income hasn’t changed.

If you compare Week 1 to Week 4 on your bank statements, you’ll often see a clear difference. The first week is optimistic; the last week is about survival. This timing trigger is how small indulgences add up and create month-end pressure. Without weekly pacing, cash flow becomes uneven and unpredictable.

5. Interface Triggers

Digital interfaces remove friction in a way that encourages spending. Saved cards, auto-fill details, fast UPI, and “Buy Now, Pay Later” options reduce the hesitation that used to exist with cash. The harder it is to feel the transaction, the easier it is to repeat it.

Paying in cash forces awareness because you see money leaving your hand. UPI doesn’t. BNPL goes one step further by delaying the pain completely. Over time, this disconnect makes it difficult to connect daily choices with monthly outcomes. The design encourages speed, not reflection, and that leads to habitual spending.

6. Identity Triggers

Sometimes spending isn’t about the item; it’s about who we believe we are. People buy products to match their identity: coffee shop regular, tech enthusiast, fitness person, fashion person, or travel person. These identity cues can feel harmless, but the cost adds up when the identity needs regular reinforcement.

For example, someone who sees themselves as a “productivity person” may visit cafés daily for the experience, not the coffee. A “fitness person” may buy multiple supplements or gear without using most of them. Identity-driven spending feels rational because it supports a self-image, but it doesn’t always support financial stability.

Also Read: 6 Simple Budgeting Tips for Better Money Management

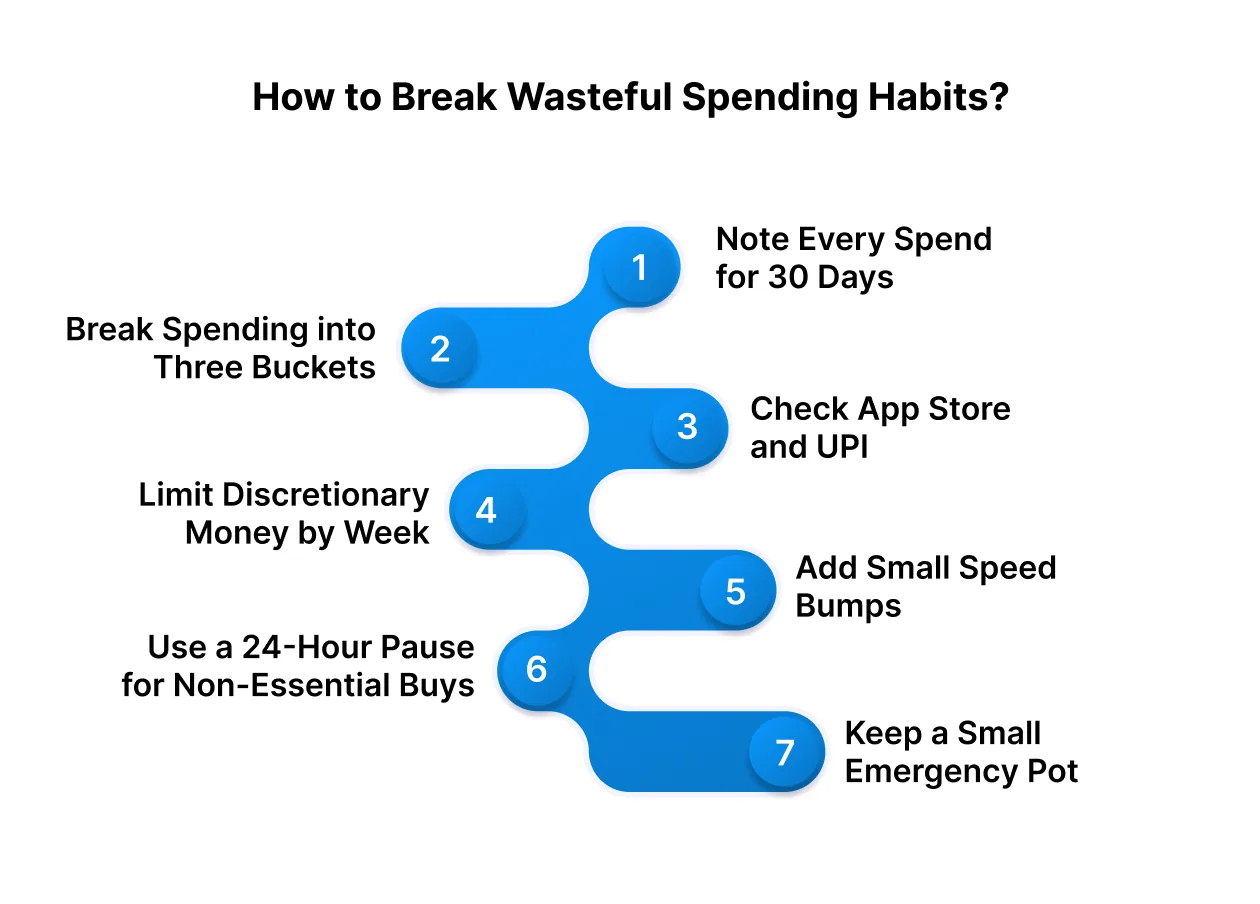

How to Break Wasteful Spending Habits?

Changing wasteful spending isn’t about cutting joy or living like a monk. It’s about introducing visibility, intention, and small guardrails so your money lasts through the month without stress. Here’s a process that works in real life, not just on paper.

Step 1: Note Every Spend for 30 Days

Most people underestimate how much they spend on small conveniences because they disappear into UPI history, auto-debits, and QR payments. Writing down every transaction for one month gives you an accurate record of how your money actually moves, not how you assume it moves. The goal is clarity, not restriction.

Example: After a full month of tracking, you notice ₹1,200 on tea and snacks from office canteens, ₹1,800 on cabs under 3 km, and ₹1,200 on mid-week takeaways. Each line item looks harmless alone, but together they cross ₹4,000.

Step 2: Break Spending into Three Buckets

Data becomes useful only when it’s categorised. Sort your transactions into:

- Essentials: expenses needed for basic functioning (rent, utilities, groceries, commute to work)

- Preferences: things that improve life or bring you joy but are optional (movies, coffee shops, clothing, travel)

- Waste: recurring spends with low value or low intention (unused apps, late-night cravings, delivery because groceries are untouched)

This framework reveals habits without shaming them.

Example: Paying ₹3,500 for rent share and ₹900 for electricity goes under Essentials. A weekend movie and food festival goes under Preferences. An auto-renewed ₹499 course you never opened lands under Waste.

Step 3: Check App Store and UPI for Silent Renewal Charges

Auto-renewals are engineered to be forgettable. They don’t demand attention; they demand your card. Reviewing them once every quarter can prevent silent drain. Look at App Store/Play Store subscriptions, UPI autopay, and net banking mandates.

Example: You discover you’re paying for four OTT platforms but only watch two, plus ₹129 for cloud storage and ₹699 for a fitness trial converted to paid. After cancelling three items, you save roughly ₹1,000/month without cutting any experience you actually care about.

Step 4: Limit Discretionary Money by Week

Monthly budgets are too wide to control behaviour. People feel rich in Week 1 and financially cornered in Week 4. Moving discretionary spending to weekly blocks forces pacing, which protects the end of the month from shortages

.

Example: If you allow ₹6,000/month for outings, food delivery, and shopping, convert it to ₹1,500/week. If you burn ₹1,300 by Thursday, you know you have ₹200 for the weekend. If you overspend one week, the next week adjusts. This keeps cash flow steady instead of lopsided.

Step 5: Add Small Speed Bumps to Convenience Apps

Spending often flows through the path of least resistance. Adding friction slows down autopilot behaviour. You don’t remove the option; you make it intentional instead of reflexive.

Examples:

- Remove saved cards from food delivery apps

- Turn off promo notifications that trigger cravings late at night

- Move food apps into a folder instead of the home screen

- Unlink BNPL from shopping apps

These tiny speed bumps often reduce unplanned orders because the impulse fades faster than the friction.

Step 6: Use a 24-Hour Pause for Non-Essential Buys

Impulse shopping is driven by emotion + instant availability. A 24-hour pause strips away the emotional push and reveals genuine interest. If you still want something the next day, buy it. If not, you saved money without feeling deprived.

Example: You see a ₹2,499 Bluetooth speaker on discount. Add to cart and leave it. The next day, check if you still want it. Many people realise they’re reacting to discounts, not needs.

Step 7: Keep a Small Emergency Pot

Most personal emergencies are not catastrophic. They’re routine inconveniences: a cracked charger, a clinic visit, a tyre puncture, or last-minute travel. Without a buffer, these small events trigger credit usage, BNPL, or borrowing, which disturbs next month’s cash flow.

Example: Saving ₹500–₹1,000/month builds ₹2,000–₹4,000 within a few months. When your phone screen guard breaks, and you need a ₹700 replacement, you pay from the pot instead of taking short-term credit or delaying essentials.

Benefits of Reducing Wasteful Spending

Cutting waste isn’t about restriction. It improves how money moves through your life. Here are the changes most people notice once wasteful spending drops:

| Benefit | What Improves |

| Smoother month-end cash flow | Money lasts across the month; fewer last-week shortages |

| Lower credit dependence | BNPL, credit cards, and small loans stop being fallback options |

| More room for meaningful spending | Extra money shifts to travel, learning, fitness, and hobbies |

| Emergency buffer starts forming | ₹1,000–₹2,000/month builds a cushion for small urgent expenses |

| Bills and EMIs get paid on time | No penalties, reconnection charges, or credit score impact |

| Reduced financial anxiety | Clear visibility removes stress about balances and statements |

Also Read: Understanding Personal Finance and Budgeting for Financial Needs

What to Do When Cash Flow Breaks Before Month-End

Even with better habits, money doesn’t always move in a straight line. Rent, deposits, medical bills, repairs, or travel can land at the wrong time. When that happens, the goal isn’t to panic, borrow from friends, or delay bills; it’s to bridge the gap cleanly and avoid downstream penalties.

Short-term gaps usually show up when:

- Salary is delayed

- Freelance income is irregular

- Unexpected expenses land mid-month

- Bills cluster in the same week

- Emergencies drain the buffer

These situations create two kinds of damage:

- Financial: late fees, reconnection charges, credit penalties, forced borrowing

- Emotional: stress, avoidance, asking friends for small favours, feeling stuck

This is where controlled, small-ticket, short-tenure financing becomes useful, not as a lifestyle tool but as a timing fix.

Feeling Stressed About Money? Pocketly Can Step In

Good habits make money easier to manage, but real life doesn’t always follow a plan. A delayed salary, clinic visit, gadget repair, or a big bill in the wrong week can throw your budget off and create pressure fast.

Pocketly helps young Indians handle these timing gaps with quick, small loans you can control.

Why people choose Pocketly:

- Borrow only what you need (₹1,000 to ₹25,000)

- No collateral or guarantors

- Fast digital KYC and quick approval

- Instant transfer to your bank account after approval

- Repayment options that follow your cash flow

- Transparent pricing: interest from 2% per month, processing fee 1% to 8%

- 24/7 access through the app

Pocketly partners with regulated NBFCs, offering secure, clear terms without hidden charges. When unexpected costs show up, Pocketly helps you handle them calmly and get back to your routine.

Conclusion

Changing how you handle money doesn’t happen overnight. It improves slowly as you track expenses, make intentional choices, and reduce small leaks. With time, the month-end feels lighter and less uncertain. You don’t need a higher income to begin; you need clarity and repeatable habits.

Keep an eye on your spending patterns, adjust when something feels off, and cover essentials first. If a tight week or an unexpected cost shows up, address it early instead of pushing it to the next month. Short-term financial support can help you manage these timing issues without asking friends or letting bills pile up.

Download the Pocketly app on iOS or Android to access quick, small-ticket loans when cash flow breaks unexpectedly. It gives you breathing room during tough weeks while you continue improving your money habits at your own pace.

FAQs

1. What does it mean to spend money wastefully?

Spending money wastefully means using money on items or experiences that don’t provide lasting value, aren’t planned, or don’t align with your financial goals. It often shows up as impulse purchases, unused subscriptions, or convenience spending that adds up.

2. How do I know if I have a wasteful spending habit?

If you regularly run out of money before the month ends, don’t remember where your money went, pay for things you don’t use, or struggle to cover essentials like bills or rent, you may have wasteful spending patterns.

3. Why do people spend money wastefully even when they know better?

Emotions, convenience, social pressure, easy digital payments, and lifestyle inflation can all override rational decision-making. When spending feels instant and painless, it’s easier to overshoot without noticing.

4. What are common examples of wasteful spending?

Frequent food delivery, multiple OTT subscriptions you rarely use, impulse shopping during sales, taking cabs for short trips, and buying gadgets or accessories without real need are common examples.

5. How can I stop spending money wastefully?

The first step is gaining visibility over spending. Track expenses for a few weeks, categorise wants vs needs, set weekly spending limits, reduce subscriptions, delay non-essential purchases, and plan food and transport ahead to avoid last-minute expenses.