You expect your EMI to go through automatically, but instead, it fails and you get charged a penalty. For many borrowers, this comes as a surprise because the reason behind the failure is not always clear.

The issue is that EMI bounce charges are often not understood until they actually happen. People assume the payment will be processed smoothly, without realizing how small gaps or technical issues can lead to additional costs.

Without clarity on when these charges apply and how they work, it becomes easy to incur penalties that could have been avoided.

In this blog, we break down what EMI bounce charges are, how much they cost, why EMIs fail, and what you can do to avoid them.

Key Takeaways

- EMI bounce charges are penalties applied when your scheduled loan payment fails due to insufficient balance or payment issues

- Charges typically range between ₹300 and ₹750 per bounce, with GST applied on top, increasing the total cost

- EMI failures are often caused by timing mismatches, mandate issues, or bank-side processing delays, not just low balance

- Repeated EMI bounces can increase your repayment cost and negatively impact your credit score and future loan eligibility.

- Maintaining a payment buffer and tracking your debit timing are key to avoiding unnecessary penalties

What Are EMI Bounce Charges and When Are They Applied

EMI bounce charges are penalties charged by lenders when your scheduled EMI payment fails to go through on the due date. This usually happens when the auto-debit request is not successfully processed.

These charges are applied only when a payment attempt is made and fails. If no attempt is triggered, such as when auto-debit is not set up, bounce charges may not apply in the same way.

EMI bounce typically occurs in situations like:

- Your account does not have enough balance at the time of auto-debit

- The bank declines the transaction during processing

- The payment mandate (NACH or auto-debit setup) is not active or fails

For example, if your EMI is scheduled for the 5th of the month and your account balance is lower than the required amount on that day, the payment attempt fails, and a bounce charge is applied.

EMI bounce charges are triggered when a scheduled payment attempt fails, not just when a payment is delayed.

Also Read: Is EMI Good or Bad? A 2026 Guide to Smart Borrowing in India

How Much EMI Bounce Charges Do Banks and NBFCs Charge in India

EMI bounce charges vary across lenders, but most banks and NBFCs follow a similar range. These charges are applied per failed transaction, which means repeated bounces can quickly increase the total cost.

Here is what you can typically expect:

- ₹300 to ₹750 per bounce: This is the common range charged by most lenders for each failed EMI attempt.

- GST charged additionally: Goods and Services Tax is applied on top of the bounce charge, increasing the total amount payable.

- Charges may differ by lender and loan type: The exact fee can vary depending on the bank, NBFC, or the type of loan you have.

- Repeated bounces lead to multiple charges: If your EMI fails more than once, the penalty is applied each time, not just once per month.

For example, if your EMI bounces twice in a month and the lender charges ₹500 per bounce, you could end up paying ₹1,000 plus GST in penalties alone.

EMI bounce charges may seem small individually, but repeated failures can significantly increase your total repayment cost.

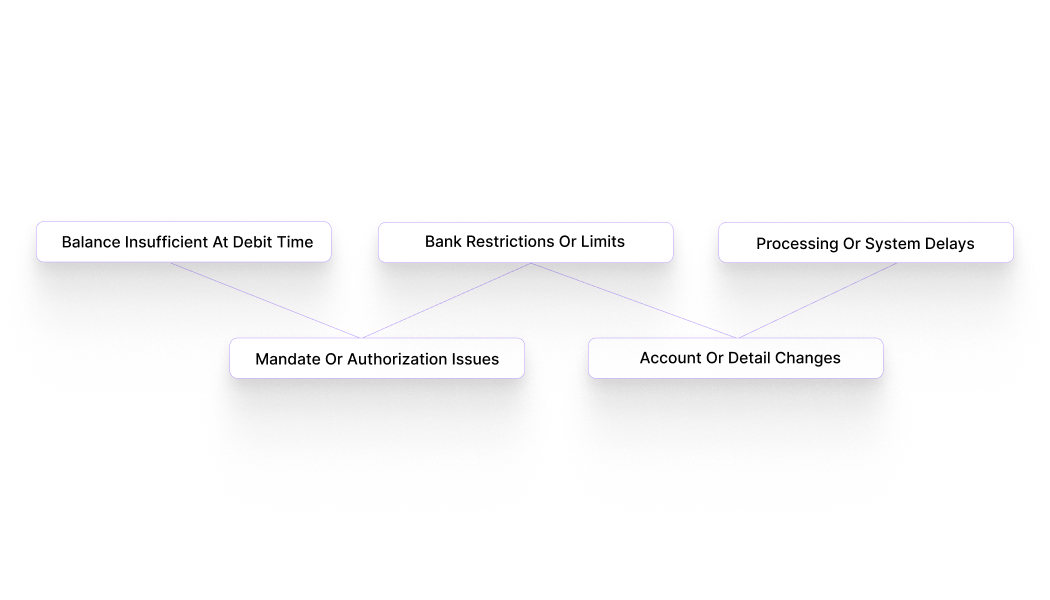

Why EMI Payments Fail (Most Common Reasons Behind EMI Bounce)

EMI payments usually fail due to specific triggers related to account balance, payment setup, or banking processes. Identifying the exact reason helps prevent repeat failures.

Here are the most common causes:

- Balance mismatch at the exact debit time: Even if funds are added later in the day, the EMI can fail if the balance was insufficient at the exact moment the debit request was processed.

- Mandate or authorization issues: Auto-debit setups like NACH require active authorization. If the mandate expires, is not verified, or fails validation, the transaction will not go through.

- Bank-side restrictions or limits: Banks may decline transactions due to daily debit limits, security checks, or temporary restrictions on the account.

- Account or payment detail changes: Switching bank accounts, closing an account, or updating details without informing the lender can interrupt the payment flow.

- Processing or system delays: In rare cases, technical issues on the bank’s or lender’s side can prevent successful debit attempts.

EMI bounce is often a timing or system issue, not just a lack of funds. When the issue is timing, not total income, a small-ticket option like Pocketly can help you manage the gap without taking on a larger long-term loan.

Also Read: How Does EMI Work on Credit Cards in India? (2026 Guide)

What Happens Immediately After an EMI Bounce (Charges, Alerts, Next Steps)

When an EMI bounce occurs, the lender’s system triggers a set of actions almost immediately. These are operational steps that happen before any long-term impact, such as credit score changes.

Here is what typically happens right after a failed EMI:

- Bounce charge is applied instantly: The penalty for the failed transaction is added to your loan account as soon as the EMI fails.

- You receive alerts and notifications: Most lenders send SMS, email, or app notifications informing you about the failed payment and next steps.

- Payment may be reattempted: In some cases, the lender may retry the auto-debit within a few days, depending on their policy.

- Outstanding amount increases: The unpaid EMI, along with the bounce charge, becomes due and needs to be cleared.

- Manual payment option is enabled: You are usually given the option to repay the EMI manually through the app, website, or payment link.

For example, if your EMI fails on the due date, you may immediately receive a notification along with the updated amount that includes the penalty, giving you the option to clear it manually.

An EMI bounce triggers immediate charges and alerts, giving you a short window to act before further consequences build up.

How EMI Bounce Charges Affect Your Credit Score and Future Loan Approval

EMI bounce does not just result in a one-time penalty. If not resolved quickly, it can impact your credit profile and future borrowing ability.

Here is how it affects you over time:

- Negative impact on your credit score: Missed or delayed EMI payments are reported to credit bureaus, which can lower your CIBIL score.

- Reduced chances of future loan approval: Lenders evaluate your repayment history. Repeated EMI bounces signal higher risk, which may lead to rejection.

- Higher interest rates on future loans: Even if approved, you may be offered loans at higher interest rates due to a weaker credit profile.

- Lower loan eligibility: Lenders may reduce the loan amount you qualify for if your repayment track record shows inconsistencies.

- Stricter verification and conditions: You may face more checks, stricter terms, or additional requirements when applying for loans later.

For example, a single delayed payment may have a limited impact, but repeated EMI bounces can significantly affect your ability to access affordable credit in the future.

EMI bounce charges are not just a cost. If they lead to missed payments, they can affect your credit score and future borrowing opportunities.

How to Avoid EMI Bounce Charges with Better Repayment Planning

Avoiding EMI bounce charges is mostly about planning your repayments correctly and ensuring your payment setup works without interruption. Small adjustments can prevent repeated penalties.

Here are practical ways to avoid EMI bounce:

- Keep a pre-EMI buffer: Maintain a small buffer above your EMI amount at least 24 hours before the due date to avoid last-minute shortfalls.

- Track your debit timing: Understand when your lender typically initiates the debit request. This helps ensure funds are available at the right moment, not just on the same day.

- Regularly verify your auto-debit setup: Check that your mandate is active, linked to the correct account, and has not expired or failed silently.

- Spread out your financial obligations: Avoid scheduling multiple auto-debits on the same date, which can strain your account balance unexpectedly.

- Align EMI dates with cash flow: If possible, choose an EMI date that matches your salary or income cycle to reduce dependency on manual balance management.

- Use alerts and reminders as backup: Even with auto-debit enabled, reminders act as a safety layer to ensure everything is in place before the due date.

When the issue is timing, not total income, a small-ticket option like Pocketly can help you manage the gap without taking on a larger long-term loan.

Also Read: What is EMI: Definition, Types, Advantages, and How it Works

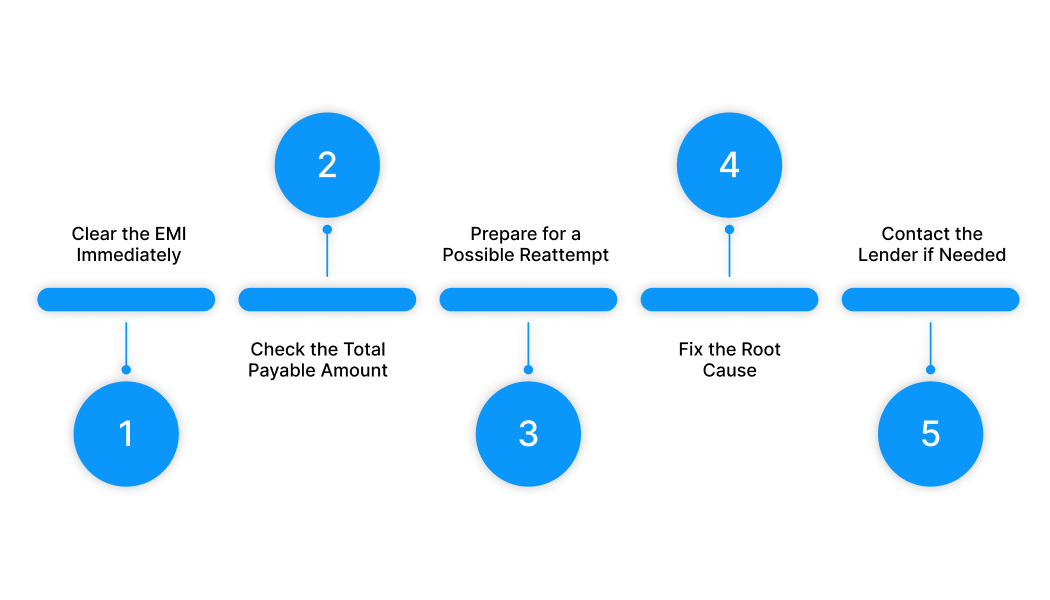

What to Do If Your EMI Has Already Bounced (Step-by-Step Recovery)

Once your EMI has bounced, quick and precise action can prevent additional penalties and protect your credit profile.

Here’s what you should do:

1. Clear the EMI immediately

Use your lender’s app, website, or payment link to manually pay the missed installment without waiting for a reattempt.

2. Check the total payable amount

Confirm the updated amount, which may include:

- Missed EMI

- Bounce charge

- Applicable GST

3. Prepare for a possible reattempt

If your lender retries the debit, ensure sufficient balance is maintained to avoid another failure.

4. Identify and fix the root issue

Check whether the failure was due to timing, mandate issues, or account changes, and correct it before the next cycle.

5. Contact the lender if something seems incorrect

If the bounce was caused by a technical issue or an unexpected charge, reaching out early can help resolve it.

Speed matters. Acting early helps limit penalties and prevents escalation into a credit score impact.

How Pocketly Helps You Manage Short-Term Gaps Before EMI Bounce

When EMI bounce happens, the issue is often not a major debt problem. It is a short-term balance gap that appears at the wrong time. In that situation, the need is usually small, immediate, and time-sensitive.

This is where Pocketly fits more practically.

Pocketly is a digital lending platform working with RBI-registered NBFCs. It is designed for short-term borrowing needs where a smaller amount can help cover an immediate gap before it turns into a missed payment or penalty.

Here is how it helps in this context:

- Smaller loan amounts keep borrowing limited: Pocketly offers loans from ₹1,000 to ₹25,000, which makes it more relevant for temporary shortfalls rather than large, long-term borrowing.

- Short-term borrowing matches short-term problems: If the issue is a timing gap before salary or an urgent payment date, a shorter borrowing cycle can be more practical than taking a large loan.

- Transparent cost structure supports better decisions: Interest starts from around 2% per month, with processing fees between 1% and 8%, depending on the borrower profile and loan amount.

- Fully digital process saves time: Since urgent EMI situations need quick action, a digital application and approval flow can help reduce delays.

- No collateral required: The loan is unsecured, so there is no need to pledge assets for a relatively small and immediate requirement.

For example, if your EMI is due in a day or two but your salary is credited shortly after, a small short-term loan may help you avoid bounce charges, penalty build-up, and credit score damage.

If you are dealing with a temporary cash gap and want to avoid EMI penalties, you can download Pocketly on iOS or Android and check your eligibility before the shortfall turns into a bigger issue.

FAQs

Q: What is the penalty for EMI bounce in India?

The penalty for EMI bounce usually ranges between ₹300 and ₹750 per failed transaction, plus GST. The exact EMI bounce charges depend on the lender and loan type.

Q: How can you remove or reduce EMI bounce charges?

EMI bounce charges generally cannot be reversed, but some lenders may waive them in genuine cases if you contact support quickly. Paying the overdue EMI immediately can help prevent additional penalties.

Q: What happens if I pay my EMI 1 day late?

If the EMI auto-debit fails, bounce charges may apply even if you pay the next day. A one-day delay may not always impact your credit score, but repeated delays can affect your repayment record.

Q: Why do EMI bounce charges happen even when I have money in my account?

EMI bounce charges can occur due to inactive auto-debit mandates, bank processing issues, or incorrect account details. It is not always caused by an insufficient balance.

Q: Do EMI bounce charges affect your CIBIL score immediately?

A single EMI bounce may not impact your credit score immediately if corrected quickly. However, repeated missed payments or delays can lower your CIBIL score over time.

Q: What is the best way to avoid EMI bounce charges in urgent situations?

Maintaining a buffer and tracking your due dates helps, but for sudden gaps, short-term solutions may be needed. Platforms like Pocketly can help cover small shortfalls and avoid EMI bounce penalties.