You work hard, earn steadily, and still wonder whether taking something on EMI is smart or a financial mistake. From smartphones to home appliances and even education, EMI options are everywhere. It feels convenient. It feels manageable.

But is it actually helping you, or quietly increasing your financial burden?

The confusion often comes later. Multiple EMIs start stacking up. A salary delay happens. An unexpected expense appears. Suddenly, what once felt affordable begins to feel stressful. Many young professionals in India fall into this cycle, not because EMI is bad, but because they never clearly understood when it makes sense and when it does not.

The truth is simple. EMI is neither good nor bad by default. It is a financial tool. Used wisely, it can support growth and cash flow. Used carelessly, it can trap you in unnecessary debt. In this blog, you will learn how to tell the difference and make smarter borrowing decisions.

Key Takeaways

- Use EMIs for productive purposes: Home loans, education, or business investments that add long-term value.

- Ensure affordability: Keep your total EMIs below 30–40% of your monthly income to maintain a healthy cash flow.

- Check interest rates: Opt for loans with reasonable rates; avoid high-interest consumer or lifestyle loans.

- Maintain emergency savings: A robust safety net prevents EMIs from becoming a financial burden.

- Borrow with discipline, not impulse: Always evaluate whether the loan will improve your financial position or just satisfy a short-term desire.

What Is an EMI and How Does It Really Work?

An EMI, or Equated Monthly Instalment, is a fixed amount you pay every month to repay a loan. Instead of paying the full loan amount at once, the borrower repays it in smaller, structured instalments over a fixed tenure.

Each EMI includes both the amount you borrowed and the interest charged by the lender. The goal is simple: spread repayment over time so it fits within your monthly income.

Components of EMI

Every EMI has two main parts:

- Principal Amount: This is the original amount you borrowed from the lender. Over time, a portion of every EMI goes toward reducing this outstanding principal.

- Interest Amount: This is the cost of borrowing money. The lender charges interest on the remaining loan amount, and this forms the second component of your EMI.

In the early months of a loan, a larger portion of your EMI goes toward interest. As the principal reduces, the interest component gradually decreases, and more of your EMI starts going toward principal repayment.

How Lenders Calculate EMI

Lenders calculate EMI using three key variables:

- Loan amount

- Interest rate

- Loan tenure

The standard EMI formula is based on reducing balance interest, where interest is charged only on the outstanding principal. While the formula looks technical, most lenders use automated systems or online EMI calculators to determine the exact amount.

The longer the tenure, the lower the EMI, but the higher the total interest paid. The shorter the tenure, the higher the EMI but the lower the total interest cost.

Example Calculation With a Simple Scenario

Suppose you take a loan of ₹1,00,000 at an annual interest rate of 12% for 2 years.

At 12% reducing balance interest for 24 months:

- Your EMI would be approximately ₹4,707 per month

- Total repayment would be around ₹1,12,968

- Total interest paid would be about ₹12,968

If you increase the tenure to 3 years:

- EMI reduces

- But total interest paid increases

This is why EMI affordability should always be evaluated along with total loan cost.

Is EMI Good or Bad? The Short Answer

EMI or Equated Monthly Instalment is neither inherently good nor bad. It is a financial tool that allows you to repay a loan in manageable monthly amounts. Its impact on your finances depends on how wisely you use it, why you borrow, and whether it fits within your budget.

When EMI Works in Your Favour?

EMIs can be a smart financial strategy when they support meaningful goals or essential needs. They help you access opportunities today without draining your savings.

For example, a home loan for ₹30 lakh at a 7% interest rate with a monthly EMI of ₹23,200 allows you to purchase a property now instead of waiting several years to save the full amount. The property appreciates over time, giving you both security and long-term value.

EMIs make sense when they are used for assets or investments that grow in value, education that increases your earning potential, or necessary expenses such as medical treatments or essential home repairs.

When EMI Becomes Risky?

EMIs can become harmful when they strain your monthly cash flow or fund non-essential purchases. If a significant portion of your income goes toward EMIs, you risk financial stress and reduced flexibility.

For instance, taking multiple EMIs for a car, a personal loan, and a high-end gadget can leave you struggling to cover unexpected expenses such as medical bills or urgent travel. EMIs that cover lifestyle upgrades rather than productive investments often lead to debt traps and unnecessary interest payments.

Affordability and Purpose Are Key

The real question is not whether EMI is good or bad but whether it is affordable and purposeful. If your EMIs fit comfortably within your budget and help you achieve a long-term goal, they are an asset. If they compromise essentials or savings, they become a liability.

A useful guideline is to ensure that your total EMIs do not exceed 30 to 40 per cent of your monthly income. This balance helps maintain financial flexibility and reduces stress.

Productive Debt Versus Lifestyle Debt

EMIs can be categorised into productive debt and lifestyle debt.

Productive debt contributes to long-term value or income. This includes home loans, education loans, or business investments. These EMIs build your future wealth or improve your earning potential.

Lifestyle debt funds short-term desires without long-term benefits. Examples include EMIs for gadgets, designer items, or vacations. These EMIs do not appreciate in value and can strain your finances if not planned carefully.

For example, a student loan of ₹5 lakh with a monthly EMI of ₹5,000 is productive if it helps secure a higher-paying job. A personal loan for a designer watch is lifestyle debt, as it adds no lasting value and can create unnecessary financial pressure.

The bottom line is that EMIs are beneficial when they build your future and harmful when they only serve temporary desires at the cost of financial stability.

When EMI Is a Good Financial Decision?

EMIs are not inherently bad. They can be a smart financial tool when used for the right reasons. Here’s when taking an EMI works in your favour:

EMIs are not inherently bad. They can be a smart financial tool when used for the right reasons. Here’s when taking an EMI works in your favour:

For Asset Building

EMIs are ideal for acquiring valuable assets that appreciate or provide long-term benefits. This includes:

- Home Loans: Buying a house with an EMI allows you to own property without paying the entire amount upfront. Over time, property value may appreciate, making the investment worthwhile.

- Education Loans: Financing higher education through an EMI helps you invest in skills and career growth, which can lead to higher earning potential.

- Business Loans: Borrowing for equipment, inventory, or expansion via EMIs can boost business productivity without straining cash flow.

Example: A ₹30 lakh home with a 7% interest rate over 20 years has manageable EMIs around ₹23,000/month, much less stressful than paying the full amount upfront.

When It Improves Cash Flow Management

EMIs can help spread large, essential expenses across multiple months instead of draining your bank balance in one go.

- They allow you to plan monthly budgets better and keep cash available for other priorities.

- EMIs turn big, unavoidable payments into predictable, manageable amounts.

Example: Buying essential household appliances worth ₹1,00,000 on a 12-month EMI of ₹8,500/month helps maintain monthly liquidity for other living expenses.

When the interest rate is low

Low-interest EMIs can be a financially smart choice, especially if the borrowing cost is lower than the potential returns from investments or inflation.

- Borrowing at a 7–9% interest rate while inflation runs at 6–7% may allow your money to grow elsewhere more efficiently.

- This can create an opportunity to invest the remaining cash instead of tying it all in one payment.

Example: Taking a ₹5 lakh personal loan at 8% interest to invest in a skill development course that increases earning potential is more effective than paying the full ₹5 lakh upfront.

When You Have a Stable Income

A predictable, stable income ensures that EMIs do not disrupt your monthly budget.

- EMIs should ideally be less than 30–40% of your net monthly income to avoid financial stress.

- Regular income allows timely repayment and reduces the risk of penalties or defaults.

Example: A professional earning ₹80,000/month can comfortably manage a ₹20,000/month home loan EMI without compromising daily expenses or savings goals.

When EMI Becomes a Risky Financial Choice

EMIs can be convenient, but they are not always the best solution. If taken without careful planning, they can create long-term financial stress, increase overall costs, and reduce your ability to save or invest.

Here’s when EMIs may do more harm than good:

For Non-Essential or Depreciating Purchases

EMIs should ideally fund assets that appreciate or provide long-term value, like homes, education, or business investments. Using EMIs for items that lose value quickly, such as smartphones, luxury gadgets, or designer products, can result in paying more than the actual worth.

Example: A ₹1,50,000 smartphone on a 12-month EMI of ₹13,500/month may cost you an extra ₹10,000–₹12,000 in interest, while the phone’s market value drops by 20–30% within a year. You end up paying more for a temporary utility.

When Interest Rates Are High

High-interest EMIs significantly increase the total repayment amount, often making the purchase much more expensive than paying upfront. Comparing the borrowing cost with potential investment or inflation returns is crucial before committing.

Example: A personal loan of ₹2,00,000 at 18% interest for 24 months costs over ₹40,000 in interest. If the same amount were invested in a low-risk mutual fund earning 8–10% annually, you could earn interest instead of paying it.

When Income Is Unstable

Committing to EMIs without a stable income exposes you to defaults, penalties, and credit score damage. Freelancers, commission-based earners, or those in project-based jobs should carefully calculate affordability before taking on a monthly liability.

Example: Taking a ₹10,000/month EMI while working on a variable monthly income can force you to miss payments in lean months, leading to late fees, higher interest, and a lower credit rating.

When EMIs Reduce Your Savings or Investments

Even if EMIs are manageable, allocating too much monthly cash to debt can restrict your ability to save, invest, or build an emergency fund. A high EMI burden reduces financial flexibility and long-term wealth creation.

Example: Paying ₹25,000/month for multiple loans while saving only ₹2,000–₹5,000/month means you miss out on compounding benefits, delaying goals like retirement planning or buying property.

When Borrowing Encourages Impulsive Spending

EMIs can make expensive purchases seem “affordable” because of smaller monthly instalments. This psychological effect can lead to lifestyle inflation, unnecessary debt, and poor financial discipline.

Example: A ₹2,50,000 luxury watch on a 24-month EMI of ₹12,500/month might feel manageable, but it adds to debt without providing real financial benefit, especially if your monthly income is just ₹50,000.

Here’s a quick snapshot to help you instantly see when taking an EMI works in your favour and when it could backfire:

| Situation | EMI Can Be Good | EMI Can Be Bad |

| Purpose | Asset building (home, education, business) | Lifestyle splurges (gadgets, vacations) |

| Income | Stable and predictable | Uncertain or irregular |

| Interest Rate | Low or reasonable | High or compounding |

| EMI % of Income | Below 30–40% | Above 50% |

| Emergency Fund | Available | Not available |

Tips to Manage EMIs Smartly

Managing EMIs effectively ensures they support your financial goals rather than strain your budget. Follow these steps to make EMIs work in your favour:

Managing EMIs effectively ensures they support your financial goals rather than strain your budget. Follow these steps to make EMIs work in your favour:

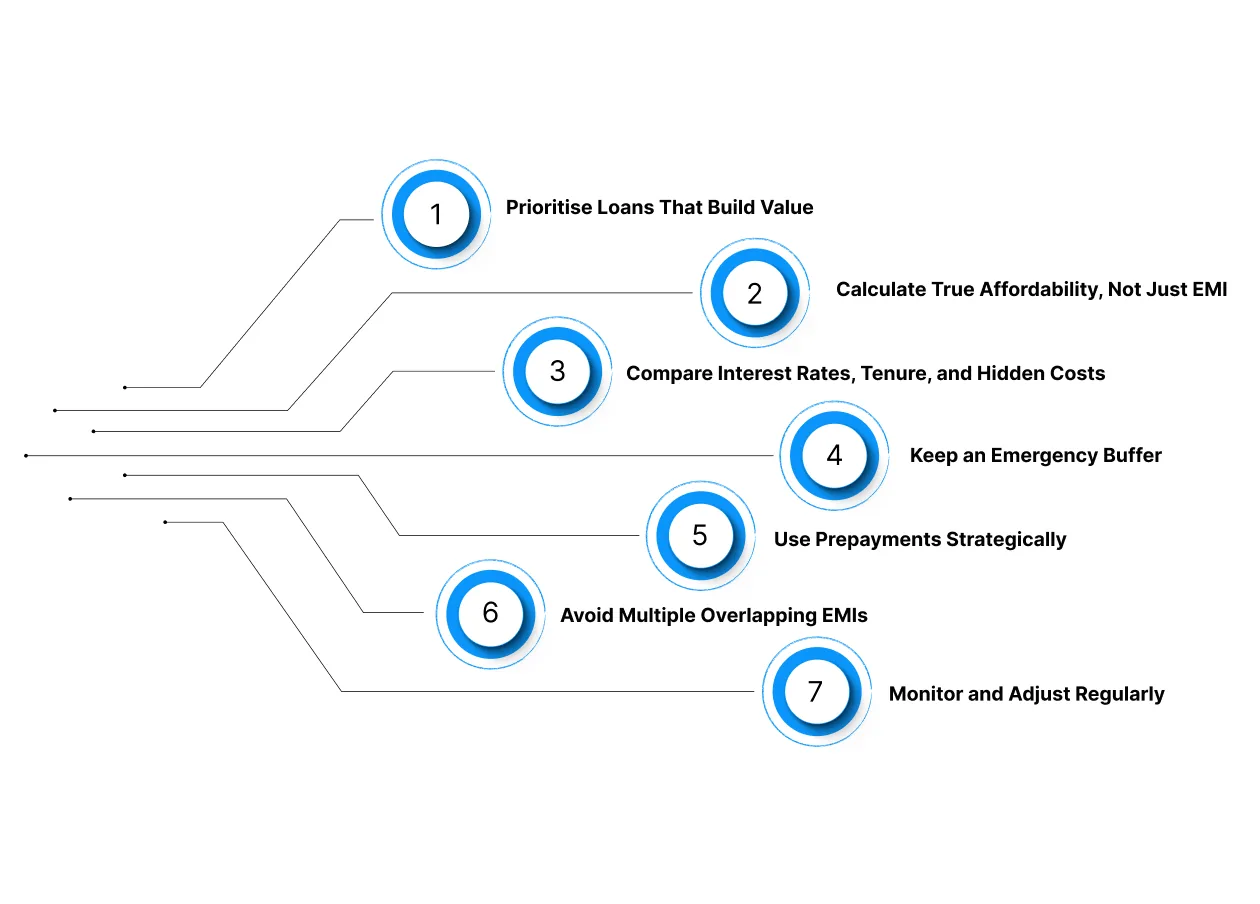

1. Prioritise Loans That Build Value

Not all EMIs are equal. Loans for assets like homes, education, or businesses contribute to long-term wealth creation.

Consumer loans for items that depreciate quickly can become a financial burden without adding real value. By focusing your EMIs on meaningful investments, each payment moves you closer to financial growth rather than just draining your cash.

Key insights:

- Let your debt work for you by increasing assets or earning potential.

- Avoid EMIs for items that lose value quickly (gadgets, luxury goods).

- Evaluate the long-term return versus immediate gratification before borrowing.

- EMIs should ideally contribute to future financial stability, not just temporary convenience.

2. Calculate True Affordability, Not Just EMI

EMI affordability isn’t just about the monthly figure; it’s about your entire financial picture. Consider all recurring expenses, lifestyle costs, and savings goals. Experts recommend total EMIs remain under 30–40% of net income. This prevents cash flow stress, missed payments, and keeps your day-to-day life financially comfortable.

Key insights:

- Treat EMIs as part of your overall budget, not a standalone number.

- Ensure enough room for essentials, discretionary spending, and savings.

- Avoid overusing, which can increase stress and risk of defaults.

- Consider the impact of interest and tenure on long-term financial health.

3. Compare Interest Rates, Tenure, and Hidden Costs

Small differences in interest rates or loan tenure can drastically affect total repayment. Look at more than the EMI: check prepayment charges, processing fees, and long-term interest obligations. A slightly higher EMI with a shorter tenure may save you more overall than a low EMI stretched over many years.

Key insights:

- Focus on the total cost of borrowing, not just the monthly EMI.

- Factor in hidden charges like processing fees, prepayment penalties, or insurance costs.

- Shorter tenures with higher EMIs often reduce overall interest paid.

- Compare multiple loan options before committing.

4. Keep an Emergency Buffer

Even a well-planned EMI can become a trap without a financial cushion. Maintain a buffer of 1–3 months of essential expenses. This protects you from unexpected events, medical emergencies, urgent travel, or sudden repairs—without defaulting or falling into stress.

Key insights:

- EMIs should fit comfortably without draining your safety net.

- An emergency fund prevents a debt snowball in case of sudden income loss.

- Helps maintain mental peace and financial resilience.

- Encourages better financial discipline by separating planned payments from unforeseen needs.

5. Use Prepayments Strategically

Partial prepayments reduce the principal, lower interest costs, and shorten the loan tenure. Allocate windfalls such as bonuses, tax refunds, or extra freelance income to prepay when possible. Even small prepayments compound over time, saving you thousands and giving you freedom from debt sooner.

Key insights:

- Prepayments directly reduce interest burden and loan duration.

- Windfalls or bonuses should prioritise high-interest loans first.

- Keeps financial goals on track while reducing long-term obligations.

- Encourages a habit of proactive debt management rather than passive repayment.

6. Avoid Multiple Overlapping EMIs

Handling multiple EMIs at once increases the risk of missed payments, stress, and budget strain. Prioritise essential loans first, and aim to clear one before taking another. Consolidating or staggering EMIs creates a clear repayment plan and reduces financial complexity.

Key insights:

- Fewer, well-managed EMIs improve financial control.

- Reduces the risk of late payments and penalty interest.

- Helps maintain clarity in monthly cash flow and budget allocation.

- Avoids overwhelming your finances and keeps debt manageable.

7. Monitor and Adjust Regularly

Life changes, and so should your EMI strategy. Regularly review your loan obligations, interest rates, and budget alignment. Refinancing or adjusting EMIs can free up cash flow and prevent debt from becoming unmanageable.

Key insights:

- Regular review ensures EMIs remain aligned with income and financial goals.

- Refinancing or prepayment can optimise interest costs and cash flow.

- Keeps your financial plan flexible for lifestyle changes or unexpected expenses.

- Encourages continuous financial awareness and reduces the risk of future debt stress.

Struggling to Manage Your EMIs? Pocketly Makes It Easier

Even well-planned EMIs can become stressful when unexpected expenses pop up. Pocketly offers quick, short-term loans to help you stay on top of your payments without disrupting your budget.

Why Pocketly works for EMI support:

- Borrow exactly what you need: Loans from ₹1,000 to ₹25,000, so you avoid extra debt.

- No collateral or guarantor: Simple application, no assets or co-signers required.

- Fast approval: Instant loan decisions after quick KYC verification.

- Immediate fund transfer: Money hits your bank account right after approval.

- Flexible repayment: Pick a plan that fits your monthly budget.

- Transparent pricing: Interest from 2%/month and processing fees of 1–8%, with no hidden charges.

- 24/7 access: Apply, track, and manage your loan anytime through Pocketly’s app.

With Pocketly’s secure NBFC partnerships, you get clarity, speed, and flexibility. So even if your EMIs feel overwhelming, you can cover them confidently and keep your finances on track.

Conclusion

Using EMIs wisely can be a powerful way to manage large expenses without straining your finances. By planning your loans carefully, choosing reasonable interest rates, and keeping your EMIs within a manageable portion of your income, you can enjoy the benefits of big purchases without falling into debt stress.

EMIs aren’t inherently bad; they become risky only when borrowing is impulsive or unplanned. Practising disciplined borrowing, prioritising essential expenses, and maintaining an emergency buffer ensures that EMIs support your financial goals rather than derail them.

For unexpected costs or short-term gaps, tools like Pocketly can provide responsible, quick financial support so you stay on track without compromising your long-term plans.

Take control of your borrowing today. Download the Pocketly app today on [Android] or [iOS] to access quick, transparent, and flexible loans whenever you need them.

FAQs

1. What does EMI mean?

EMI stands for Equated Monthly Instalment. It is the fixed amount you pay every month to repay a loan, which includes both principal and interest.

2. Is taking an EMI always bad?

No. EMI is not inherently bad. It can be helpful if used to buy assets, manage cash flow, or invest in something productive. It becomes risky when it strains your income or finances for non-essential purchases.

3. How can I know if an EMI is affordable?

A general rule is that your total EMIs should not exceed 30–40% of your monthly income. You should also have emergency savings before taking on multiple loans.

4. What types of loans make EMI good?

Home loans, education loans, business loans, or any productive loan with a reasonable interest rate and long-term benefits are generally considered good EMI use.

5. What types of loans make EMI risky or bad?

High-interest personal loans, credit card EMIs, Buy Now Pay Later (BNPL) for non-essential items, or loans when your income is unstable can make EMIs financially risky.

6. Can paying multiple EMIs affect my credit score?

Yes. Having too many active EMIs increases your debt-to-income ratio. Missing payments or defaulting can negatively impact your credit score.