Keeping up with bills feels easy until due dates start overlapping, and your salary timing doesn’t match your expenses. A few delayed payments, an unexpected cost, or missed tracking can quickly lead to late fees, stress, and disrupted plans. Even with a steady income, it can feel like your money isn’t working in your control.

The problem is not just income but the lack of a clear system to manage when and how your bills are paid. Without structure, small gaps can turn into repeated financial pressure.

Bill management helps you stay ahead by organising payments, prioritising essentials, and aligning everything with your income. In this blog, you will learn simple, practical ways to manage your bills without stress.

Key Takeaways

-

Bills feel stressful, not because of income, but because of poor planning and timing between salary and expenses.

-

Effective bill management means knowing what to pay, when to pay and setting money aside as soon as your salary arrives.

-

Track all types of bills, fixed, variable, and irregular, to avoid surprises and last-minute financial pressure.

-

Simple habits like reminders, weekly checks, and prioritising essentials can prevent late fees and keep your finances stable.

-

If you face a temporary cash gap, short-term options like advance loans can help you stay on track, but they should be used carefully.

What is Bill management?

Bill management means planning and paying your expenses in a way that fits your income, so you don’t miss payments or feel financially stretched. It’s not just about remembering due dates. It’s about knowing what to pay, when to pay it, and how to prepare for it in advance.

Instead of reacting when a bill shows up, you stay prepared for it. This helps you avoid late fees, reduce stress, and keep your monthly finances stable.

What it looks like in real life:

-

Setting aside rent and other fixed expenses as soon as your salary arrives

-

Tracking variable bills like electricity or mobile so they don’t surprise you

-

Using reminders or auto-pay to avoid missing due dates

In simple terms, bill management is about staying ahead of your expenses so your payments happen smoothly without last-minute pressure.

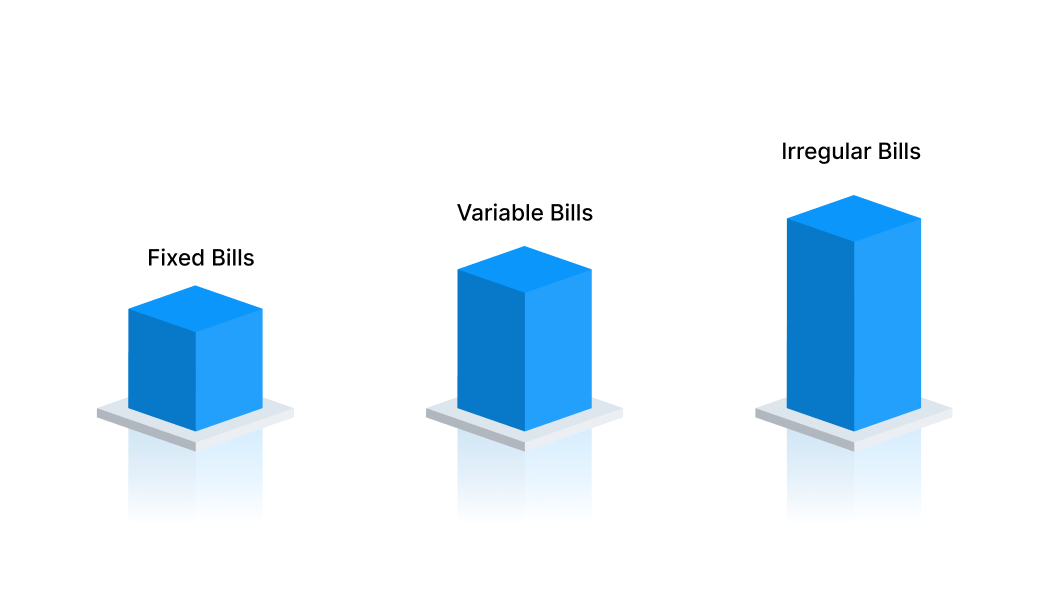

Types of Bills You Should Track Every Month

Not all bills behave the same way. Some are predictable, some fluctuate, and some appear occasionally. If you don’t understand these differences, it becomes difficult to plan your money properly, and that’s when missed payments or sudden stress start.

1. Fixed Bills

Fixed bills are expenses that stay almost the same every month and are usually mandatory. These are commitments you’ve already signed up for, so they don’t change unless you actively modify or cancel them.

Examples:

-

Rent

-

EMIs

-

Subscriptions (Netflix, gym, etc.)

Why it matters: These bills form the foundation of your monthly expenses. Since they are predictable, they should be accounted for first as soon as your salary arrives, so the rest of your spending doesn’t interfere with them.

2. Variable Bills

Variable bills are expenses that change based on how much you use or spend. They are flexible by nature, which means they can go up or down depending on your habits and lifestyle choices.

Examples:

-

Electricity bill

-

Groceries

-

Fuel or transport

Why it matters: These bills are harder to control because the amount isn’t fixed. Without tracking, they can slowly increase and reduce the money you have left for savings or other priorities.

3. Irregular Bills

Irregular bills are expenses that don’t occur every month but are still unavoidable. They often come as one-time or occasional payments and can feel sudden if you’re not prepared for them.

Examples:

-

Insurance premiums

-

Medical expenses

-

Repairs, travel, or annual fees

Why it matters: These are the most commonly ignored expenses. Since they don’t show up monthly, people don’t plan for them, which leads to dipping into savings or borrowing when they arise.

Read more: Understanding Utility Bills: Types and Examples

Step-by-Step System to Manage Your Bills Efficiently

Bills start feeling stressful when you don’t know what’s due, when it’s due, or whether you’ll have enough balance when the time comes. A simple system removes this confusion and helps you stay in control of your money throughout the month.

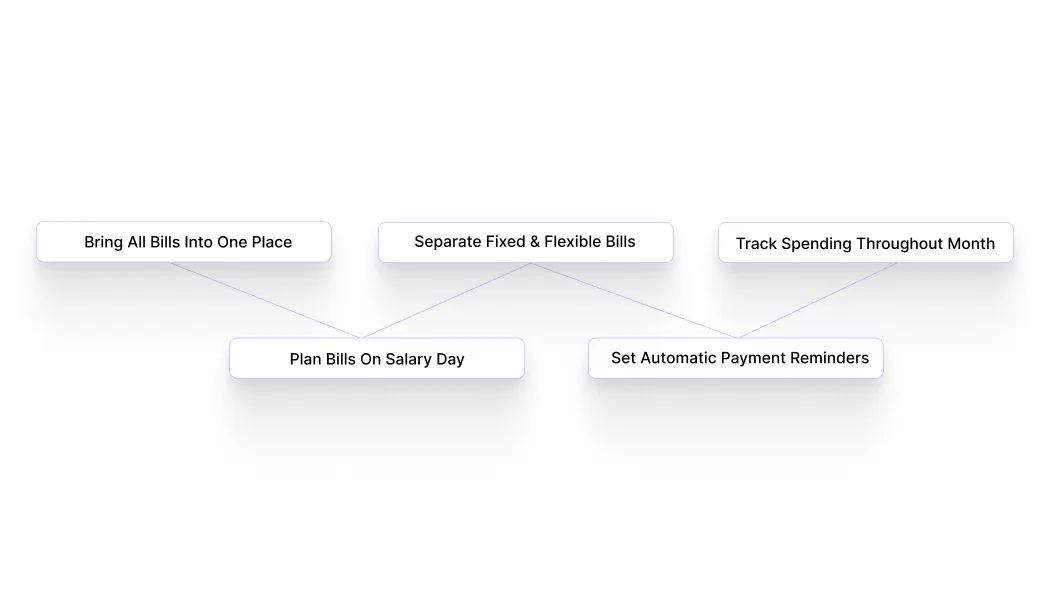

Step 1: Bring All Your Bills Into One Place

Most people have their expenses scattered across apps, messages, and emails. This makes it easy to forget payments or underestimate how much they owe.

Create one simple list where you write:

-

The bill name (rent, electricity, mobile, etc.)

-

Due date

-

Usual amount

This list becomes your monthly reference. Once everything is visible in one place, you stop relying on memory and start making clearer decisions.

Step 2: Plan Your Money the Day Your Salary Comes In

The biggest mistake beginners make is spending first and managing bills later. Instead, reverse this habit.

As soon as your salary is credited, decide how much will go toward bills. You don’t need to physically separate the money, but you should mentally lock it.

For example, if your total bills are around ₹20,000, treat that amount as unavailable for spending. This prevents situations where you enjoy early-month spending but struggle when bills are due.

Step 3: Understand Which Bills Can Change and Which Cannot

Not every expense has the same level of importance. Some payments must be made on time, while others give you flexibility.

-

Fixed and essential: rent, EMIs, electricity

-

Flexible: subscriptions, ordering food, shopping

This clarity helps you make better decisions when money feels tight. You don’t need to panic; you simply adjust flexible spending while keeping essentials secure.

Step 4: Reduce Dependence on Memory

Trying to remember every due date increases the chances of missing payments. Instead, create a system that reminds you automatically.

You can:

-

Set phone reminders a few days before due dates

-

Use auto-pay for fixed bills like subscriptions

-

Keep a simple calendar view of your payments

This way, even during busy weeks, your bills stay on track without extra effort.

Step 5: Stay Aware of Your Money During the Month

Bill management is not a one-time activity. Your spending keeps changing during the month, so your awareness should too.

Take a few minutes once a week to check:

-

What is already paid?

-

What is coming next?

-

How much balance is left?

This helps you catch problems early. For example, if you notice your balance dropping faster than expected, you can reduce spending before it affects important bills.

Step 6: Prepare for Expenses That Don’t Come Every Month

A major reason people struggle with bills is not monthly expenses, but unexpected ones. Medical costs, repairs, or annual payments often feel like sudden shocks.

Instead of treating them as surprises, plan for them in advance. Even setting aside a small amount like ₹500–₹1,000 every month can make a big difference. Over time, this creates a safety cushion that protects your savings and reduces stress.

Handle urgent bills effortlessly. Pocketly gives you ₹1,000–₹25,000 instantly, so your budget stays stress-free. Apply in minutes and get instant access to your funds.

Common Bill management Mistakes That Cost You Money

Bills usually don’t become a problem overnight. It’s small, repeated habits that slowly create pressure, missed payments, and confusion around money.

Here are the mistakes that most beginners make, often without realising their impact:

1. Missing Due Dates

Risk: A missed payment doesn’t just mean a late fee. Over time, repeated delays can affect your credit score, especially for EMIs or credit cards. It also creates a pattern where you are always catching up instead of staying ahead.

How to Avoid: Set reminders at least 2–3 days before the due date, not on the same day. This gives you time to arrange money if needed. For fixed bills, auto-pay can remove the risk completely.

2. Ignoring Small Recurring Expenses

Risk: Subscriptions and small auto-debits often go unnoticed because the amount feels insignificant. But when multiple such expenses run together, they reduce your available balance and make important bills harder to manage.

How to Avoid: Go through your bank statement once a month and identify all recurring charges. Ask yourself if you actually use each service. Removing even 2–3 unused subscriptions can free up meaningful money.

3. Not Planning for Irregular Bills

Risk: Expenses like medical bills, repairs, or annual payments feel "unexpected", but they are actually a normal part of life. When you don’t plan for them, they disrupt your monthly budget and often force you to use savings or borrow.

How to Avoid: Treat irregular expenses as part of your monthly planning. Even saving a small amount regularly builds a buffer that makes these situations easier to handle.

4. Spending First, Paying Bills Later

Risk: When you spend freely at the start of the month, you may enjoy short-term comfort but face pressure later when bills are due. This often leads to cutting essentials, delaying payments, or relying on credit.

How to Avoid: As soon as your salary is credited, mentally reserve money for bills. This simple habit ensures your essential payments are always covered, regardless of other spending.

5. Depending Only on Memory

Risk: With multiple bills, different due dates, and daily distractions, it’s easy to forget a payment. Missing even one bill due to forgetfulness can lead to penalties and unnecessary stress.

How to Avoid: Use a system instead of memory. It can be as simple as phone reminders, a notes app, or a calendar. The goal is to make sure nothing depends on you remembering it manually.

6. Not Checking Your Financial Position During the Month

Risk: If you only look at your bank balance occasionally, you may not realise how quickly your money is being used. This can lead to situations where important bills are due, but your balance is already low.

How to Avoid: Take a few minutes each week to check your balance, upcoming bills, and recent spending. This helps you stay aware and make small corrections before problems build up.

What to Do When You Can’t Pay a Bill on Time

There will be months when your expenses don’t go as planned. The key is not to panic, but to take small, practical steps that help you stay in control and avoid making the situation worse.

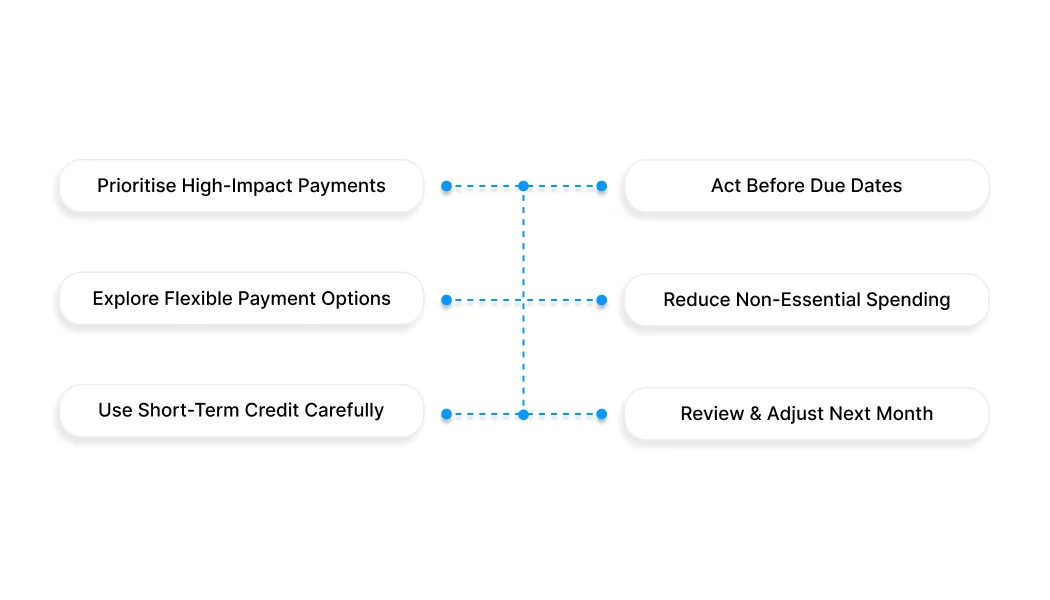

1. Prioritise Payments That Have Immediate Impact

When money is limited, trying to pay for everything at once can create more confusion. Instead, focus on the bills that have the highest consequences if missed, like rent, EMIs, or credit card payments.

For example, delaying rent or an EMI can lead to penalties or long-term issues, while some subscriptions or services can be paused without major impact. This clarity helps you use your available money more effectively.

2. Don’t Wait Until the Last Minute

Ignoring a bill doesn’t make it go away. In fact, delays often lead to late fees, penalties, or service disruptions that increase your overall burden.

A better approach is to check your due dates early and assess your situation honestly. Even a few days of early action give you more options compared to reacting after the deadline has passed.

3. Explore Flexible Payment Options

In some cases, service providers or lenders may offer small adjustments if you reach out in advance. This could include a short extension, a revised due date, or even part-payment options.

For instance, if you inform your provider before the due date, they may allow you to split the payment instead of charging a full penalty. These options are not always guaranteed, but they are often overlooked.

4. Temporarily Cut Back on Non-Essential Spending

When you’re short on funds, even small expenses can make a difference. Reducing non-essential spending for a few days can help you free up enough money to cover important bills.

This could mean avoiding food delivery, postponing shopping, or pausing subscriptions temporarily. These are short-term adjustments that help you manage a bigger priority.

5. Use Short-Term Credit as a Backup, Not a Habit

If the gap is temporary and you are confident about your next income, short-term options like advance loans can help you stay on track.

For example, if your salary is a few days away but a bill is due now, borrowing a small amount and repaying it soon can prevent penalties or disruptions. The key is to borrow only what you need and avoid relying on it regularly.

6. Reflect and Adjust for the Next Month

Once the situation is handled, take a moment to understand what caused the gap. It could be an unplanned expense, missed tracking, or overspending earlier in the month.

For example, if a medical expense disrupted your budget, you can start setting aside a small buffer going forward. These small adjustments help you avoid repeating the same situation.

Also Read: How to Manage Monthly Expenses Smartly in 2025

Struggling to Keep Up With Bills? Pocketly Can Help You Bridge the Gap

Even with a clear plan, there are times when your bills and salary don’t align. A payment might be due today, while your income is still a few days away. In such moments, the challenge is not your budgeting, but the timing of your cash flow.

Pocketly is designed to handle exactly this kind of situation. It gives you quick access to small amounts of money so you can pay important bills on time without disrupting your overall financial plan.

Here’s how it helps:

-

Access only what you need: Borrow between ₹1,000 and ₹25,000 to cover specific bills like rent, utilities, or urgent payments, instead of taking a larger loan.

-

No credit history required: You can get started without a credit score, collateral, or guarantor, making it easier for students and first-time earners.

-

Quick approval and fast transfer: A simple KYC process allows you to apply and receive funds directly into your bank account within a short time.

-

Repayment that fits your income: Choose a plan that aligns with your salary cycle so repayment doesn’t create additional pressure.

-

Clear, upfront costs: Interest starts from 2% per month, with processing fees between 1% and 8%, so you know the total cost before you borrow.

-

Helps you avoid penalties and disruptions: Paying bills on time means no late fees, no service interruptions, and better financial consistency.

-

Simple app-based experience: Everything from applying to tracking repayments happens in one place, making it easy to manage even for beginners.

Pocketly works best as a short-term support system, not a long-term dependency. When used carefully, it helps you stay on track with your bills while keeping your finances stable and predictable.

There may still be situations where your bills and income don’t align perfectly. In such cases, Pocketly can act as a practical backup. With loan amounts ranging from ₹1,000 to ₹25,000, quick approvals, and flexible repayment options, it helps you cover urgent payments without disrupting your routine.

Download Pocketly on iOS or Android to manage short-term gaps and stay in control of your finances.

FAQs

1. What is Bill management, and why is it important?

Bill management is the process of planning and paying your expenses on time so you don’t face late fees, penalties, or financial stress. It helps you stay organised, avoid last-minute pressure, and keep your monthly finances stable.

2. How do I start managing my bills as a beginner?

Start by listing all your bills with their due dates and amounts. Once you have a clear view, plan your payments as soon as your salary comes in, set reminders, and review your expenses weekly to stay on track.

3. Which bills should I prioritise first?

Always pay essential bills first, such as rent, EMIs, and credit card dues. These have stricter consequences if missed. Other expenses, like subscriptions or non-essential services, can be delayed if needed.

4. What should I do if I miss a bill payment?

Pay the bill as soon as possible to reduce late fees or penalties. Check if there are additional charges, and try to avoid repeating the delay by setting reminders or using auto-pay going forward.

5. What if I don’t have enough money to pay a bill on time?

Focus on the most important payments, cut down non-essential spending, and try to free up cash within your budget. If the gap is temporary, short-term options like advance loans can help, but only if you’re sure about repayment.