Meta Description: Learn how to develop strong spending discipline with practical strategies to control expenses, avoid impulsive buying, and build long-term financial stability.

It’s never been easier to spend money. Between one-tap UPI scans and "Buy Now, Pay Later" prompts at every checkout, our bank balance can disappear before we even realise we’re overspending. For students and young professionals in India, the problem is usually about maintaining a lifestyle. As soon as we earn a little more, we start spending a lot more, often on things we didn’t even want an hour ago.

But building spending discipline doesn't mean you have to stop enjoying your life or cut out every small luxury. It’s really just about taking back control. It’s the difference between mindlessly swiping your phone and making a conscious choice about where your money goes.

If you're tired of wondering where your salary went by the 15th of the month, this guide is for you. We’re going to break down how to build habits that stick, so you can stop stressing about your bank app and start building some real financial breathing room.

Key Takeaways

- Always link your savings to a specific, measurable long-term goal to maintain motivation.

- Use technology to "pay yourself first" and automate bill payments to remove the struggle of willpower.

- Implement a 24-48 hour rule for non-essential purchases to significantly reduce impulsive spending.

- Aim for a 3-6 month buffer to prevent debt when life throws a curveball.

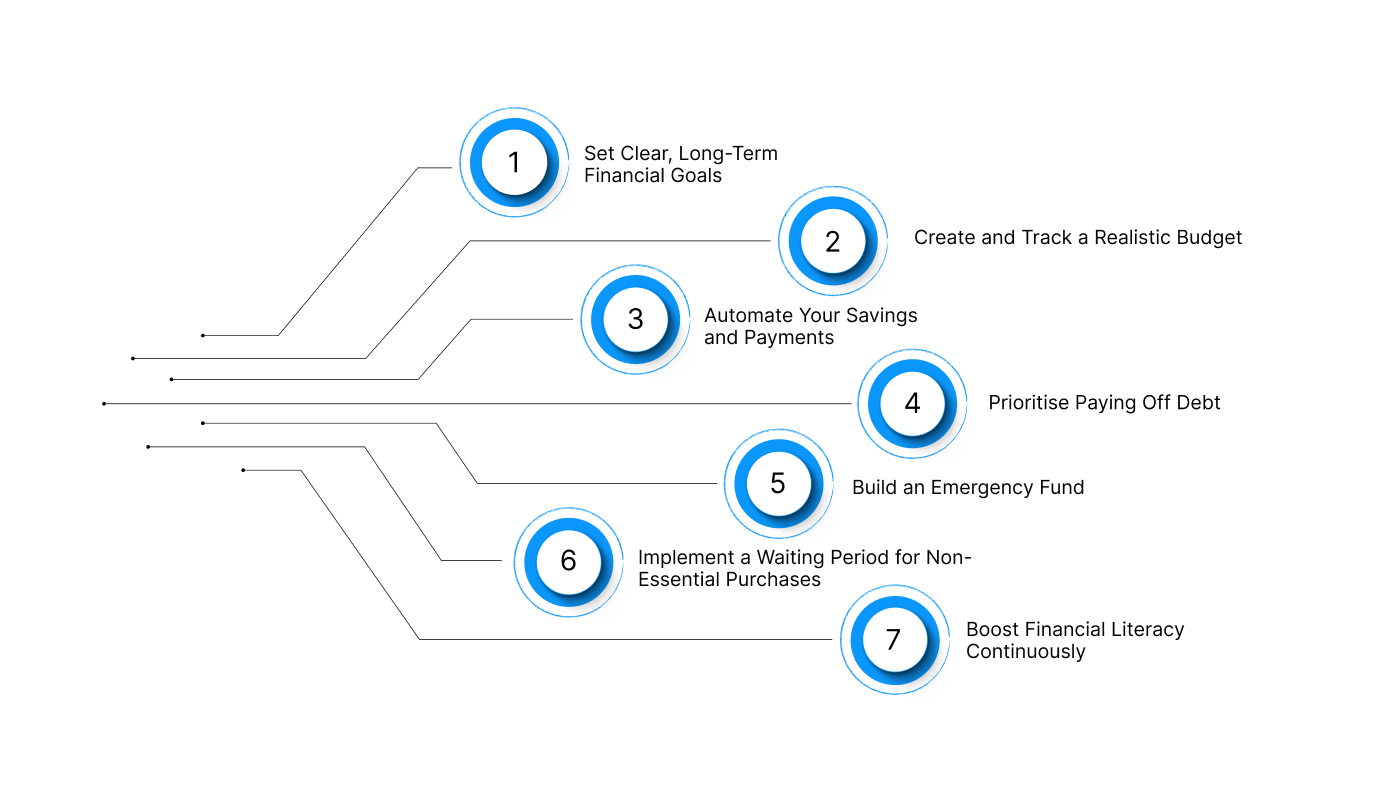

7 Practical Steps to Master Your Spending Discipline

Building lasting financial habits requires a mix of psychological shifts and practical tools. By following a structured approach, you can master your cash flow and ensure every rupee is spent with a clear purpose and intent.

Developing spending discipline is a journey that transforms your relationship with money from one of stress to one of security. Here are the essential steps to help you stay on track and achieve your financial goals:

Set Clear, Long-Term Financial Goals

The foundation of any disciplined behaviour is a "why." Without a clear purpose, spending discipline feels like a chore. When you have a specific goal in mind, whether it is saving for a post-graduate degree in the UK, buying your first vehicle, or building a down payment for a home, every rupee you save feels like a victory rather than a sacrifice.

- Define Specific and Measurable Objectives: Instead of saying "I want to save money," say "I want to save ₹2 Lakhs for a professional certification by December 2026." Specificity creates a roadmap for your brain to follow.

- Create a Visual Motivation: Many successful savers use "vision boards" or digital wallpapers of their goals. Seeing your dream holiday or a debt-free certificate every time you open your phone acts as a psychological barrier against impulsive splurges.

- Break Goals into Milestones: Large goals can be overwhelming. If you need ₹50,000 for a new laptop, break it down into ₹4,200 per month. Achieving these smaller milestones provides the dopamine hit usually sought through shopping, reinforcing your positive habits.

Once you have your "why" firmly in place, you need a system to manage the "how" and that starts with a realistic budget.

Create and Track a Realistic Budget

A budget is often misunderstood as a "financial diet," but in reality, it is a tool for freedom. It tells your money where to go instead of you wondering where it went. For young Indians, tracking expenses is crucial because small, daily costs like ₹50 for tea or ₹200 for a quick delivery can quietly drain thousands of rupees over a month.

- The 50/30/20 Rule: A popular and effective framework is to allocate 50% of your income to "Needs" (rent, groceries, bills), 30% to "Wants" (entertainment, dining out), and 20% to "Financial Goals" (savings, debt repayment). This ensures you are living within your means while still enjoying life.

- Monitor Every Rupee: Use digital spreadsheets or budgeting apps to log your expenses in real-time. Seeing that you have already spent 80% of your "dining out" budget by the 10th of the month is a powerful deterrent to ordering that extra pizza.

- Categorise Your Costs: Separate your fixed costs (subscriptions, insurance premiums) from your variable costs (shopping, transport). This allows you to see exactly where you can "trim the fat" when your spending discipline starts to slip.

While a budget provides the plan, automation provides the willpower to stick to it without effort.

Automate Your Savings and Payments

One of the biggest enemies of spending discipline is "decision fatigue." If you have to choose to save money every single month, eventually, you will have a bad day and choose to spend it instead. Automation removes the human element of temptation, making saving the default state of your bank account.

- Set Up standing Instructions: Arrange for a portion of your salary or allowance to be automatically transferred to a separate savings or investment account on the day you receive it. This is known as "paying yourself first."

- Automate Bill Payments: Use the Bharat Bill Payment System (BBPS) or bank standing instructions for your electricity, mobile, and internet bills. This avoids late fees and ensures your essential obligations are met before you can spend on non-essentials.

- Systematic Investment Plans (SIPs): For those looking to grow wealth, SIPs in mutual funds are an excellent tool. By automating a fixed monthly investment, you benefit from rupee-cost averaging and the power of compounding without needing to "time the market."

Also Read: Top 8 Financial Planning Strategies for Salaried Employees

Prioritise Paying Off Debt

Debt is the opposite of spending discipline; it is spending tomorrow’s money today at a very high cost. For many young professionals in India, high-interest credit card debt or informal loans can become a significant emotional and financial burden. Clearing these should be your top priority.

- The Debt Avalanche Method: List all your debts and focus on paying off the one with the highest interest rate first, while making minimum payments on the others. This mathematically saves you the most money over time.

- Avoid the "Minimum Due" Trap: Credit card companies in India often highlight the "Minimum Amount Due." Paying only this ensures you stay in debt for years as interest piles up. Always aim to pay the total amount due to maintain your credit score.

- Consolidate Where Possible: If you have multiple high-interest small loans, consider consolidating them into a single, lower-interest personal loan to simplify your repayments and reduce the total interest paid.

Clearing debt creates a clean slate, but to keep it that way, you need a safety net for life’s unexpected moments.

Also Read: Top 10 Tips to Spend and Save Money Wisely

Build an Emergency Fund

Financial discipline often breaks down when an emergency occurs. If your laptop breaks or you face a medical issue without a safety net, you are forced to borrow, which derails your entire budget. An emergency fund is your "financial insurance policy."

- The 3-6 Month Rule: Aim to save enough to cover at least three to six months of your essential living expenses. This fund should be kept in a liquid, easily accessible account—not locked in long-term investments.

- Start Small but Consistent: If saving three months' worth of expenses feels impossible, start with a goal of ₹5,000. Once you hit that, aim for ₹10,000. The security of even a small fund prevents the panic that leads to poor financial choices.

- Use it only for True Emergencies: A "sale" on your favourite brand is not an emergency. Define what constitutes an emergency (e.g., job loss, health crisis) and stick to those rules strictly to protect your fund.

Implement a Waiting Period for Non-Essential Purchases

In our current digital environment, retailers use "flash sales" and "limited-time offers" to create a false sense of urgency. This urgency bypasses the rational part of your brain and leads to spending discipline failures. A simple cooling-off period is the most effective antidote.

- The 24-48 Hour Rule: For any non-essential purchase over a certain amount (e.g., ₹2,000), commit to waiting at least 24 to 48 hours. Often, the emotional "need" for the item disappears once the initial excitement cools down.

- The "Can I Buy It Twice?" Rule: If you cannot afford to buy an item twice over without stressing your budget, you cannot afford it once. This simple mental check helps you distinguish between what you have the money for and what you can actually afford.

- Clear Your Carts: Many people use online shopping carts as a "wish list." Instead of keeping items in the cart where a single click can buy them, move them to a "Save for Later" list or a separate note on your phone.

Boost Financial Literacy Continuously

Knowledge is the ultimate tool for spending discipline. When you understand concepts like inflation, compound interest, and real rates of return, you begin to view every rupee as a potential employee that can work for you.

- Read Reliable Sources: Follow reputable Indian finance blogs, listen to podcasts, and read books on personal finance. Understanding the Indian tax system (like Section 80C) can also help you save money legally and efficiently.

- Understand the "Cost of Credit": Many people don't realise that a "No Cost EMI" often involves hidden processing fees or the loss of a cash discount. Being literate about these details helps you make truly cost-effective decisions.

- Attend Workshops: Many organisations and the RBI offer free financial literacy resources. Spending 30 minutes a week on your financial education is one of the best investments you can make.

Even with the best discipline, life can sometimes throw a curveball that requires immediate support.

How Pocketly Supports Your Financial Journey

Building perfect spending discipline takes time, and during that learning curve, you might encounter an unexpected cash flow gap. Perhaps an emergency repair is needed, or a vital bill is due before your next salary arrives.

In these moments, instead of turning to high-interest credit cards or unverified lenders, Pocketly offers a transparent and regulated solution.

Pocketly is a digital lending platform designed to help young Indians manage short-term financial needs without compromising their long-term goals.

- Accessible Credit: We offer personal loans from ₹1,000 to ₹25,000, perfect for bridging small gaps in your monthly budget.

- Transparent Terms: Our interest rates range from 2% to 3% per month, with processing fees between 1% and 8%. We believe in total transparency—no hidden charges, ever.

- Fast and Digital: Our KYC process is 100% digital and paperless. Once approved, the funds are disbursed instantly to your bank account.

- Responsible Borrowing: We encourage our users to only borrow what they need and to have a clear repayment plan. Using Pocketly responsibly can also help you build a positive credit history, which is essential for larger loans (like a home or car loan) in the future.

How to Get Started with Pocketly:

- Download: Get the Pocketly app from the Google Play Store or iOS App Store.

- Verify: Complete the quick, paperless KYC process with your basic documents.

- Apply: Choose the amount you need and see the repayment schedule upfront.

- Receive: The money is transferred to your account, helping you stay on track with your financial obligations.

Conclusion

Developing spending discipline is one of the most transformative skills a young adult can master. It provides a sense of security and confidence that transcends mere numbers on a screen.

By setting clear goals, automating your systems, and being mindful of your triggers, you can build a lifestyle that is both enjoyable today and secure for tomorrow. Remember, financial wellness is a journey of many small steps.

For the times when you face a temporary hurdle, Pocketly is here to provide the support you need to keep moving forward.

Ready to take control of your finances? Download the Pocketly app today on iOS or Android and join thousands of young Indians building a smarter financial future.

FAQs

1. How much should I ideally save every month?

While the 50/30/20 rule suggests 20%, the ideal amount depends on your individual goals and stage of life. If you are a student, even saving 5-10% of your allowance is a great way to build the habit of spending discipline.

2. Can I use a budget and still have fun?

Yes! A good budget includes a category for "Wants" or "Fun." The goal is to spend that money guilt-free because you know your bills and savings are already taken care of.

3. What is the biggest mistake people make with spending discipline?

The most common mistake is being too restrictive too quickly. If your budget is "all work and no play," you are likely to quit. Aim for progress, not perfection, and allow yourself small, planned rewards.

4. How does my credit score affect my financial future?

Your credit score (CIBIL) is a reflection of your financial discipline. A high score allows you to get lower interest rates on major loans like home or education loans, saving you lakhs of rupees in the long run.