Many people search for how debit card interest rates are calculated, assuming debit and credit cards work in the same way. The confusion usually starts when charges appear on statements, making it seem like interest is being applied.

In reality, debit cards do not usually have interest rates because they use your own money. However, certain situations such as overdraft facilities, penalties, or linked credit features can introduce costs that feel similar to interest.

Understanding when these charges apply and how they are calculated is important. It helps you avoid unnecessary costs and clearly distinguish between debit card usage and credit-based borrowing.

This blog explains how debit card-related charges work, when interest may apply, how it is calculated in specific cases, and why credit card costs often feel higher.

At a Glance

-

Debit cards do not have interest rates like credit cards. They use your own money, so no borrowing means no interest calculation.

-

Credit card interest is calculated daily, not monthly. The annual rate is broken into a daily rate and applied to your outstanding balance.

-

The number of days your balance stays unpaid drives the cost. Even small delays increase total interest significantly over time.

-

Carrying a balance removes the interest-free benefit. New transactions may also start attracting charges once dues are not fully cleared.

-

Interest feels high because it compounds through usage patterns. Partial payments, continued spending, and delays increase the total payable faster than expected.

Do Debit Cards Have Interest Rates Like Credit Cards

Debit cards are linked directly to your bank account. When you use them, the money is deducted from funds you already have.

Since there is no borrowing involved, there is no standard interest calculation like credit cards.

However, users may still notice charges on their statements. These are usually:

-

ATM withdrawal charges

-

foreign transaction fees

-

penalty fees

-

overdraft-related charges

These are not interest in the traditional sense, but they can feel similar because they increase the total amount deducted from your account.

Also Read: How Does EMI Work on Credit Cards in India? (2026 Guide)

How Are Credit Card Interest Rates Actually Calculated

Credit card interest is not applied as a flat monthly charge. The annual percentage rate (APR) shown on your card is first broken down into a smaller daily rate, and that rate is then applied to the outstanding balance over time.

The process starts with converting the annual rate into a daily periodic rate. This is done by dividing the annual rate by the number of days in a year.

For example:

If the APR is 36% per year, the daily rate becomes approximately:

-

36% ÷ 365 ≈ 0.0986% per day

This daily rate is what actually gets applied to your unpaid balance.

Instead of charging interest once at the end of the month, the card issuer applies this daily rate to the outstanding amount for each day the balance remains unpaid. This is why the total interest depends not just on the amount, but also on how long it stays unpaid.

Key points to understand here:

-

The annual rate is only a reference, not the actual calculation unit

-

Interest is applied daily, not monthly

-

The longer the balance remains, the higher the total interest

This daily calculation method is what makes credit card interest feel higher than expected, especially when balances are carried forward for multiple days.

How Does Daily Interest Calculation Work on Credit Cards

Once the daily rate is derived, the next step is understanding how it is applied across your billing cycle. Interest is calculated based on how your outstanding balance changes day by day.

Instead of treating the balance as one fixed number, the card issuer tracks it daily.

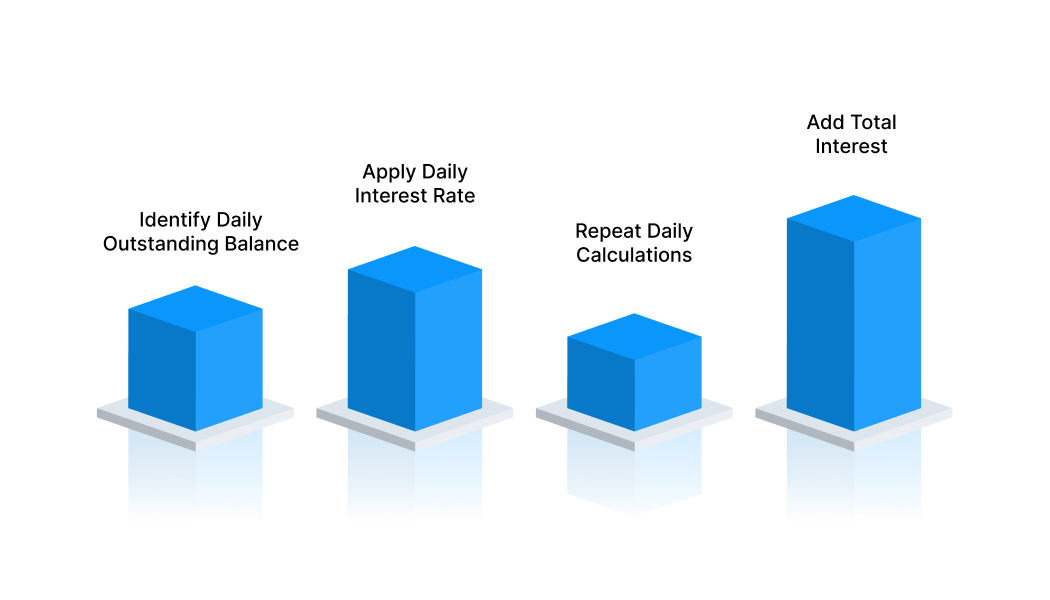

Step 1: Identify the outstanding balance for each day

Every day, your balance may change depending on:

-

new transactions

-

repayments made

-

previous unpaid amount

Interest is calculated on the balance that exists at the end of each day.

Step 2: Apply the daily rate to that balance

For each day, the daily rate is applied to that day’s outstanding amount. If the balance changes the next day, the calculation adjusts accordingly.

Step 3: Repeat this for all days in the cycle

This process continues for every day until the outstanding amount is cleared. Each day’s interest is calculated separately based on that day’s balance.

Step 4: Add up the total interest

At the end of the billing period, all the daily interest amounts are added together to arrive at the total interest charged.

What makes this important is that even small delays or additional transactions can change the daily balance, which directly affects the final interest amount.

If you are dealing with a small expense and want to avoid interest building up daily, you can explore short-term options like Pocketly instead of carrying a balance forward.

What Is the Formula to Calculate Credit Card Interest

Once the daily balances and rates are known, the total interest is calculated using a simple structure that combines three elements: the outstanding amount, the daily rate, and the number of days the balance is carried.

The basic formula is:

Interest = Outstanding Balance × Daily Rate × Number of Days

This formula is applied to each portion of the balance depending on how long it remains unpaid.

How to read this formula

-

Outstanding Balance → the amount on which interest is being applied

-

Daily Rate → the per-day percentage derived from the annual rate

-

Number of Days → how long that specific balance remains unpaid

If the balance changes during the billing cycle, the formula is applied separately for each period where the amount stays constant.

Where this matters

-

A higher balance increases the interest directly

-

More days increase the total cost even if the balance stays the same

-

Changes in balance during the cycle create multiple calculations

This formula helps break down what looks like a complex charge into a predictable structure. Once you know these three variables, it becomes easier to estimate how much interest will be added.

Also Read: How Secured Credit Cards Build Credit Score

How Is Credit Card Interest Calculated With an Example

To see how the calculation works in practice, consider a simple scenario where the balance remains unchanged for a few days.

Example

-

Outstanding amount: ₹10,000

-

Annual interest rate: 36%

-

Number of days unpaid: 10

Using the daily rate derived earlier, interest is applied for each day the balance is carried.

Step-wise outcome

-

Daily interest on ₹10,000 comes to roughly ₹9.86

-

Over 10 days, total interest becomes approximately ₹98.6

So, instead of just looking at the annual rate, the actual cost depends on how long the amount remains unpaid.

What this example shows

-

Even for a small amount, interest builds up with time

-

The number of days has a direct impact on total cost

-

Clearing the balance earlier reduces the overall interest

This kind of calculation becomes more noticeable when balances are carried for longer periods or when new transactions are added before clearing the previous dues.

When Does Credit Card Interest Start Getting Charged

Interest does not apply immediately after every transaction. It depends on how the outstanding amount is handled by the due date.

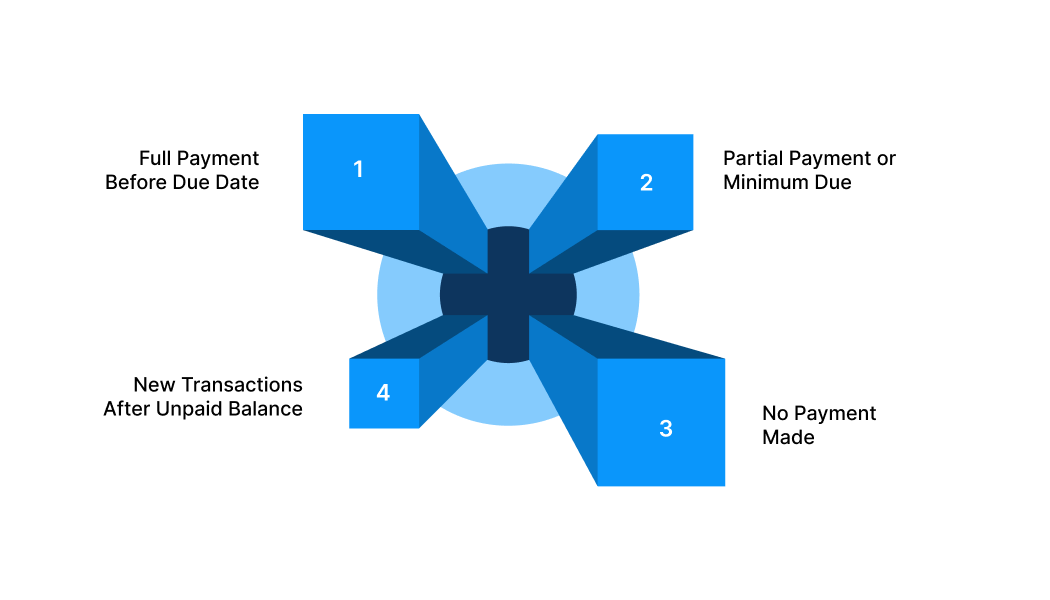

-

Full payment before due date: If the entire outstanding balance is paid within the billing cycle, no interest is charged on those transactions. This is often referred to as the interest-free period.

-

Partial payment or minimum due paid: If only part of the total amount is paid, interest starts applying to the remaining balance. From that point, the outstanding amount continues to attract charges until it is fully cleared.

-

No payment made: If no payment is made by the due date, the entire outstanding amount becomes subject to interest. This also removes the benefit of any interest-free period for that cycle.

-

New transactions after unpaid balance: Once a balance is carried forward, new purchases may also start attracting interest from the transaction date itself, depending on the card terms. This increases the overall cost even if the original amount was small.

Understanding this timing helps in planning repayments more effectively and avoiding unnecessary charges.

Why Credit Card Interest Feels So High

Many users feel that credit card interest is unusually high, even when the amount borrowed is not very large. This perception comes from how the charges build up over time rather than the rate alone.

-

Interest keeps adding to the remaining balance: When the outstanding amount is not cleared, the next cycle starts with a higher base. This means future charges are applied on a larger amount, which increases the total payable faster than expected.

-

Multiple transactions increase the impact: Using the card again before clearing previous dues adds new amounts to the existing balance. This creates a combined effect where different spends contribute to the total cost.

-

Charges are spread across billing cycles: Interest does not always appear as a single visible charge. It can continue across multiple cycles, making it harder to notice how much is being added over time.

-

Small amounts feel manageable but add up: Individual daily or cycle-based charges may seem small, but when they accumulate over several days or cycles, the total becomes significant.

-

Lack of visibility on total cost: Many users focus only on the minimum due or monthly statement without tracking the overall impact. This makes the final cost feel higher when seen over a longer period.

This is why even a small unpaid balance can feel expensive if it is carried forward without a clear repayment plan.

When charges start building across cycles, switching to a fixed short-term option can help keep costs predictable. Pocketly is one such option for smaller amounts.

What Mistakes Increase Your Credit Card Interest

Interest often increases not because of the rate itself, but because of how the card is used during the billing cycle. Certain patterns can raise the total cost without being immediately obvious.

-

Paying only the minimum amount regularly: Paying just the minimum due keeps the account active but leaves most of the balance unpaid. This causes the remaining amount to continue accumulating charges over time.

-

Withdrawing cash using a credit card: Cash withdrawals are treated differently from purchases. They usually attract charges from the day of withdrawal, which increases the overall cost quickly.

-

Continuing to spend without clearing previous dues: Adding new transactions before clearing earlier balances increases the total outstanding. This makes it harder to reduce the principal amount and keeps charges building up.

-

Missing the due date by a few days: Even short delays can increase the total payable. A missed or late payment can lead to additional charges and extend the period for which the balance remains unpaid.

-

Ignoring statement details: Not reviewing the statement properly can lead to unnoticed charges or patterns that increase the total cost. This makes it harder to take corrective action early.

These mistakes often seem small individually, but together they can significantly increase the overall amount paid.

How Can You Reduce Credit Card Interest Charges

Reducing interest is less about changing the rate and more about controlling how the balance is managed across billing cycles. A few consistent actions can significantly lower the total amount paid over time.

-

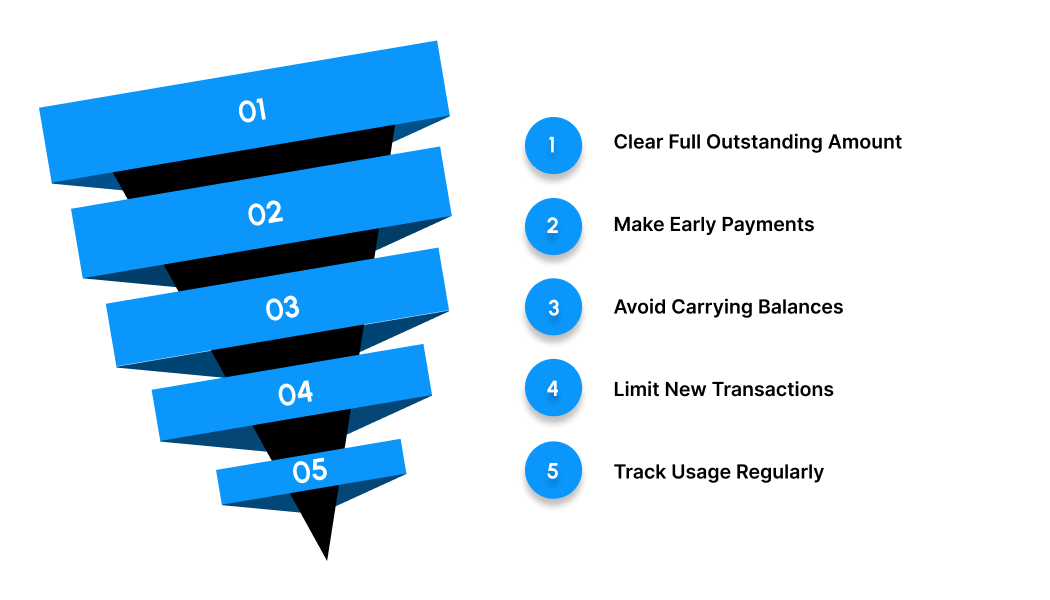

Clear the full outstanding whenever possible: Paying the entire billed amount prevents any remaining balance from carrying forward. This keeps future cycles free from additional charges.

-

Make payments earlier within the cycle: Instead of waiting until the due date, making payments earlier reduces the number of days the balance stays active. This directly lowers the total amount added over time.

-

Avoid carrying balances across cycles: Keeping the balance from moving into the next cycle helps maintain control over the total payable. Once a balance is carried forward, it becomes harder to reduce quickly.

-

Limit new transactions until dues are cleared: Reducing or pausing card usage while an outstanding amount exists helps prevent the total from increasing further. This allows repayments to bring the balance down more effectively.

-

Track usage regularly: Checking balances and transactions during the cycle helps identify how the outstanding amount is changing. This makes it easier to adjust payments before the next statement is generated.

These steps focus on controlling the duration and size of the outstanding balance, which has a direct impact on how much is added over time.

How Pocketly Can Help With Small Short-Term Credit Needs

Credit cards are designed for flexible spending, but when balances are carried forward, the cost can become difficult to manage for smaller, short-term needs. In such situations, having a structured option with clearer terms can help avoid ongoing charges.

Pocketly is built for small-ticket, short-duration requirements, where the need is limited but immediate. Instead of revolving balances, it focuses on defined amounts and repayment timelines.

Where it fits better

-

When the required amount is relatively small

-

When the expense cannot be delayed

-

When there is clarity on repayment timing

-

When avoiding rolling balances is a priority

What Pocketly offers

-

Loan amounts typically ranging from ₹1,000 to ₹25,000

-

Fully digital process with quick KYC

-

Short-term usage aligned with immediate needs

-

No requirement for collateral

This approach works differently from credit cards because the focus is on closing a defined gap, rather than keeping a balance open across cycles.

You can download Pocketly on iOS or Android and check your eligibility to see available amounts before deciding, especially for small short-term needs.

FAQs

Q: Is credit card interest calculated daily or monthly in India?

Credit card interest is calculated on a daily basis. The annual rate is converted into a daily rate and applied to the outstanding balance for each day it remains unpaid.

Q: Why do I get charged interest even after paying my credit card bill?

This usually happens when the full outstanding amount is not cleared. Even if a partial payment is made, the remaining balance continues to attract charges until it is fully repaid.

Q: Does interest apply to new purchases if I have unpaid dues?

Yes, in most cases. Once a balance is carried forward, new transactions may also start attracting charges from the transaction date instead of getting an interest-free period.

Q: Why is credit card interest higher than other types of loans?

Credit cards offer unsecured, flexible borrowing without fixed repayment schedules. This convenience is priced higher compared to structured loans with defined tenures.

Q: Is there a way to manage small expenses without relying on credit card rollover?

For smaller, short-term needs, some users prefer structured options where the amount and repayment are clearly defined. Platforms like Pocketly allow users to check eligibility for small amounts instead of carrying forward credit card balances.

Q: How can I check how much interest I will be charged on my credit card?

You can estimate it by looking at your outstanding balance, the annual rate on your card, and how many days the balance will remain unpaid. Statements also provide a breakdown of charges applied.