Ever been surprised when a loan or credit card gets rejected even though you thought your finances were fine? The problem isn’t your income; it’s your credit history. In India, banks and lenders rely on credit management bureaus to see how responsibly you’ve handled loans, payments, and credit cards. Without knowing how these bureaus work, even small mistakes can hurt your credit score and future financial plans.

The solution is simpler than you think. Understanding credit management bureaus lets you track your financial behaviour, spot errors, and make smarter decisions.

In this blog, we’ll explain what a credit management bureau is, why it matters, and how beginners can build a strong credit profile in India. By the end, you’ll know exactly how to take control of your credit and avoid surprises when you need funds the most.

Key Takeaways

-

A credit management bureau doesn’t lend money. It builds your financial profile based on how you use and repay credit over time.

-

Your credit behaviour matters more than your income, as lenders rely on your past actions to judge future reliability.

-

Even small actions shape your credit profile early, and mistakes can stay on your record for years if not corrected.

-

You can check your credit report for free and should review it regularly to catch errors, track progress, and stay informed.

-

Strong credit comes from consistency, paying on time, using credit wisely, and managing short-term cash gaps smartly.

What is a Credit Management Bureau?

A credit management bureau is an organisation that tracks your borrowing and repayment behaviour. In simple terms, it records how you use credit, like loans or credit cards, and whether you repay them on time. This data is used to create your credit report and credit score, which lenders use to judge your reliability.

Credit Bureau vs Bank or Lender

Many beginners confuse these, but they play very different roles:

-

Banks/Lenders: Give you loans or credit cards

-

Credit Bureaus: Collect and maintain your credit data

-

Key point: Bureaus don’t approve or reject loans; they only provide your financial history

Popular Credit Bureaus in India

In India, there are four main credit bureaus:

-

CIBIL (TransUnion CIBIL)

-

Experian

-

Equifax

-

CRIF High Mark

Each bureau maintains your credit information and generates your credit score based on your financial habits.

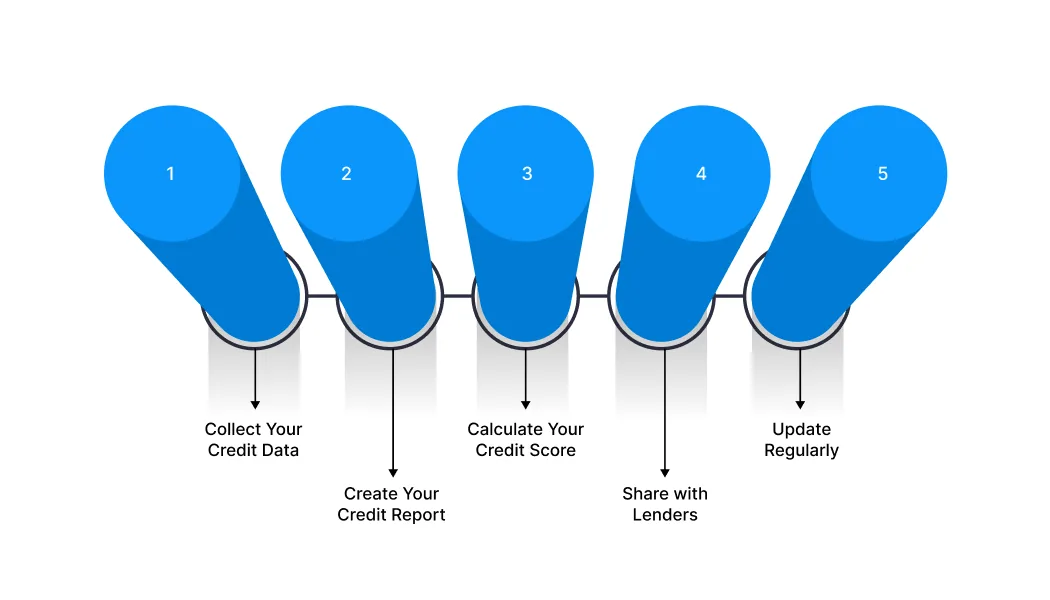

How Does a Credit Management Bureau Work?

A credit management bureau collects your credit information, organises it into a report, and shares it with lenders when needed. Instead of tracking your financial behaviour yourself, the bureau maintains a detailed record that reflects how responsibly you handle credit.

The process usually involves these steps:

-

Collect Your Credit Data: Whenever you take a loan or use a credit card, banks and lenders share your details with credit bureaus. This includes your loan amount, repayment history, and any missed or delayed payments.

-

Create Your Credit Report: All this information is compiled into a credit report, which shows your complete borrowing and repayment history over time.

-

Calculate Your Credit Score: Based on your report, the bureau assigns you a credit score. This number reflects your creditworthiness and helps lenders quickly assess your risk level.

-

Share with Lenders: When you apply for a loan or credit card, lenders access your credit report and score from the bureau to make approval decisions.

-

Update Regularly: Your credit data is updated frequently as you make payments or take new credit, so your report stays current.

Example: If you regularly pay your credit card bills on time, your credit score improves. But if you miss payments, your score drops, making it harder to get approved for loans in the future.

A credit management bureau does not lend money, but it plays a key role in helping lenders make informed decisions and encouraging responsible financial behaviour.

Also Read: What Is a Credit Score: Calculation & Tips to Improve

CIBIL vs Experian vs Equifax vs CRIF: What’s the Difference?

At first glance, all credit bureaus in India may seem the same. They all collect your credit data and generate a score, but there are small differences in how they operate and what lenders prefer.

Here’s how they differ:

|

Factor |

CIBIL |

Experian |

Equifax |

CRIF High Mark |

|

Full Name |

TransUnion CIBIL |

Experian India |

Equifax India |

CRIF High Mark |

|

Most Used By Lenders |

Very high (widely preferred) |

High |

Moderate |

High (NBFCs & microfinance) |

|

Score Range |

300–900 |

300–900 |

300–900 |

300–900 |

|

Data Coverage |

Strong across banks & credit cards |

Good mix of lenders |

Balanced but slightly limited |

Strong in NBFC & rural lending |

|

Report Updates |

Regular |

Regular |

Regular |

Regular |

|

Key Strength |

Most trusted by banks |

Detailed reports |

Global presence |

Strong in alternative lending |

How Credit Bureaus Impact Your Loans, Rates, and Opportunities

Most people think credit bureaus only matter when applying for a loan. But their real impact goes beyond approvals; they quietly shape how lenders treat you financially.

Here’s what that means in practice:

-

It Controls the “Cost” of Your Credit: Two people can get the same loan, but pay very different interest rates. Your credit data decides whether you get cheaper credit or end up overpaying for the same money.

-

It Builds Your Financial Identity Before You Realise It: Even small actions like missing a single payment or using too much credit can start shaping your profile early. By the time you need a loan, your financial reputation is already formed.

-

It Influences More Than Just Loans: Your credit profile can impact approvals for rentals, credit cards, and even some job background checks, something most beginners don’t expect.

-

It has a Long Memory: Good habits take time to build, but mistakes can stay visible for years. This makes early awareness extremely important, especially for students and first-time earners.

-

It Rewards Consistency, Not Income: You don’t need a high salary to build a strong credit profile. Regular, on-time payments matter more than how much you earn.

Example: Someone earning ₹25,000 but paying bills on time can have a better credit profile than someone earning ₹1 lakh but missing payments.

Take control of your finances and credit score. Pocketly lets you access ₹1,000 to ₹25,000 instantly, keeping payments on time and your record clean. Apply in minutes and build a stronger credit profile.

How to Check Your Credit Report in India Before It Affects You

Checking your credit report is simpler than most people think, and it’s one of the easiest ways to stay in control of your financial health. Many beginners avoid this step, assuming it’s complicated or only needed when applying for a loan.

The process usually involves these steps:

1. Choose a Credit Bureau

Start by selecting a trusted credit bureau like CIBIL, Experian, Equifax, or CRIF High Mark. Each of these platforms allows you to access your credit report and score. While the core information remains similar, scores may vary slightly between bureaus due to different calculation methods.

Example: You check your score on CIBIL and see 750, while Experian shows 740. Both are considered good, but the variation comes from how each bureau evaluates your data.

2. Sign Up with Basic Details

To access your report, you’ll need to register using basic details like your name, PAN card, mobile number, and date of birth. This helps the bureau match your identity with your credit records.

Example: If your PAN is linked to your loans and credit cards, entering it correctly ensures your full credit history is fetched without missing details.

3. Complete Identity Verification

After entering your details, you’ll go through a verification step, usually via an OTP sent to your registered mobile number. This ensures that only you can access your financial information.

Example: You receive an OTP on your phone and enter it on the website to securely log in and view your report.

4. Access and Download Your Credit Report

Once verified, you can view your credit report online or download it for future reference. This report gives a complete picture of your credit activity.

Example: You download your report as a PDF and review all your active loans, credit cards, and past payment records in one place.

5. Review Important Details Carefully

Go through key sections like repayment history, credit utilisation, active accounts, and any overdue payments. This helps you understand what’s affecting your credit score.

Example: You notice a few delayed payments from the past year, which explains why your score is lower than expected.

6. Check for Errors or Unknown Entries

Mistakes in credit reports are more common than people think. Look for loans you didn’t take, incorrect balances, or wrong payment statuses.

Example: You find a credit card listed that you never applied for. This could be an error or fraud, and you can raise a dispute to fix it.

7. Use Your Free Credit Report Benefit

In India, you’re entitled to at least one free credit report per year from each bureau. Using this regularly helps you stay updated without any cost.

Example: You check your report every few months using different bureaus, ensuring your data is accurate, and your score is improving over time.

Also Read: Minimum Credit Score Required for Personal Loan

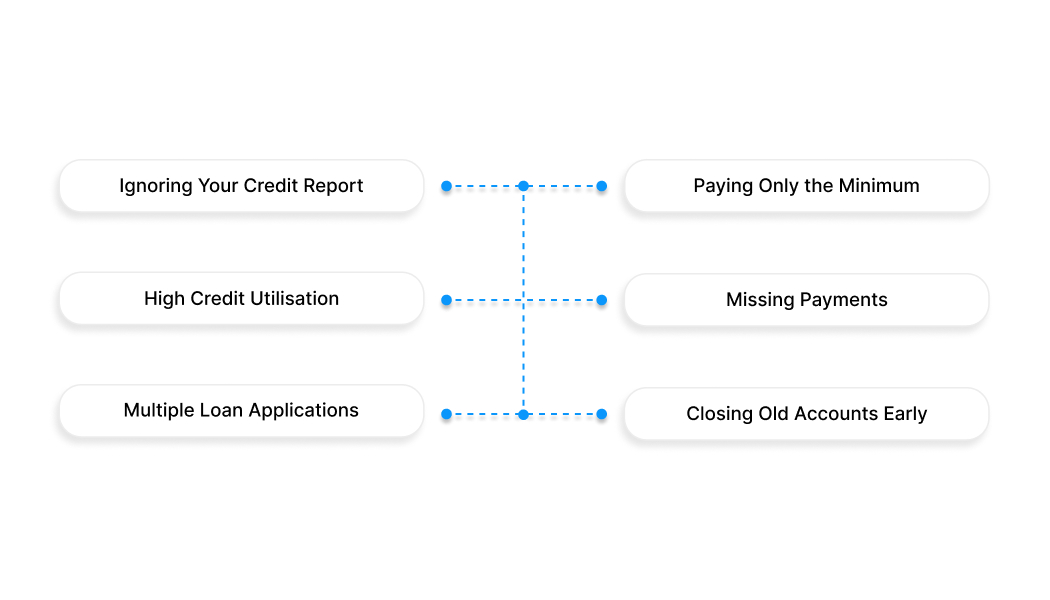

What Most People Get Wrong About Credit Early On and How Bureaus See It

When it comes to credit, small mistakes can have a long-term impact, and credit management bureaus track all of them. Most people don’t realise they’re harming their credit profile until it’s too late, especially in the early stages of building it.

Here are some common mistakes to watch out for and how bureaus reflect them:

1. Ignoring Your Credit Report

Many beginners don’t realise that credit management bureaus track every detail of your borrowing and repayment behaviour. Ignoring your credit report means errors, outdated info, or even fraudulent accounts can go unnoticed. These issues can lower your credit score and affect loan or credit card approvals.

Actionable Tip: Review your credit report from CIBIL, Experian, Equifax, or CRIF High Mark at least every few months. Spot errors? Raise a dispute immediately to ensure your credit history is accurate. Early intervention prevents long-term damage.

2. Paying Only the Minimum Due

Paying only the minimum amount keeps your account active, but it signals potential repayment risk to lenders and is recorded by credit bureaus. Over time, this can increase interest costs and make your credit profile appear weak.

Actionable Tip: Whenever possible, pay the full outstanding amount. If that’s not feasible, pay more than the minimum. This shows consistent repayment behaviour, which bureaus reward with better credit scores.

3. Using Too Much of Your Credit Limit

High credit utilisation is a red flag for lenders and is captured by credit bureaus. Even if you pay on time, consistently maxing out your credit can reduce your score and limit your loan opportunities.

Actionable Tip: Keep your credit usage below 30–40% of your total limit. Spread expenses across cards or request a higher limit to maintain a healthy ratio and reflect responsible credit behaviour in your bureau report.

4. Missing Payments

Missing even a single payment is recorded by bureaus and can negatively affect your credit score for years. It sends a warning signal to lenders that you may be unreliable, even if all other payments are timely.

Actionable Tip: Set up auto-debit or reminders. At the very least, ensure minimum payments are on time. This simple habit can protect your score and maintain a clean credit record.

5. Applying for Multiple Loans or Cards Together

Every loan or card application triggers a check recorded by bureaus. Applying for many products in a short span can make you appear financially stressed and lower your chances of approval.

Actionable Tip: Apply only when necessary. Space out applications and check your eligibility criteria beforehand. This demonstrates measured and responsible credit behaviour.

6. Closing Old Credit Accounts Too Early

Older accounts contribute to your credit history length, which bureaus consider when calculating your score. Closing them too soon can reduce your overall credit age, weakening your credit profile.

Actionable Tip: Keep older accounts active with occasional usage. Even small, timely transactions help maintain a strong credit history, signalling reliability to lenders.

Bridge Payment Gaps Instantly and Protect Your Credit Score with Pocketly

Even when you handle money responsibly, timing mismatches can affect your credit record. A bill or EMI might be due before your salary arrives, or unexpected expenses can temporarily create a shortfall. These small gaps can lead to late payments, which are recorded by credit management bureaus and can hurt your score.

Pocketly is built to support you during these short gaps. It gives you quick access to small amounts of money so you can manage urgent expenses without delaying important payments.

Here’s how it helps:

-

Manage urgent payments on time: Whether it’s a bill or a small EMI, you can avoid delays during tight situations.

-

Borrow only what’s necessary: With access to ₹1,000 to ₹25,000, you can cover immediate needs without taking on extra burden.

-

Fast access when you need it most: A simple digital process ensures quick approval and direct transfer to your bank account.

-

No complicated eligibility barriers: You don’t need a strong credit history, collateral, or a guarantor to get started.

-

Repay in a way that fits your income cycle: Flexible repayment options help you manage your cash flow better.

-

Clear, upfront costs: Interest starts from 2% per month, with processing fees between 1% and 8%, so you know the total cost before you borrow.

-

Avoid unnecessary financial stress: Handle short-term gaps without disrupting your monthly budget.

-

Simple, app-based experience: From applying to tracking repayments, everything is managed in one place.

Pocketly works best as a short-term financial cushion, not something to rely on regularly. When used carefully, it helps you handle timing mismatches without disturbing your overall financial flow.

With easy access to small loan amounts, quick approvals, and convenient repayment options, you can manage urgent expenses without disrupting your overall financial flow.

Download Pocketly on iOS or Android to handle short-term money needs with ease and stay in control of your finances.

FAQs

1. What is a credit management bureau?

A credit management bureau is an organisation that keeps track of your borrowing and repayment behaviour. It collects data from banks and creates your credit report and credit score. Lenders use this to understand how reliable you are before giving you a loan or credit card.

2. Which are the main credit bureaus in India?

The major credit bureaus in India are CIBIL, Experian, Equifax, and CRIF High Mark. All of them track your credit activity and generate a score based on your behaviour. Your score may differ slightly across bureaus, but the overall trend usually stays similar.

3. How do credit bureaus get my information?

Banks, NBFCs, and credit card companies regularly share your financial data with credit bureaus. This includes your loan amounts, credit usage, and payment history. The bureaus use this data to update your credit profile.

4. How often is my credit report updated?

Your credit report is typically updated every 30–45 days, depending on when lenders submit new data. So, if you repay a loan or miss a payment, it may take some time to reflect. That’s why it’s important to track your report regularly.

5. How can I check my credit report?

You can check your credit report online through any of the official bureau websites. Most bureaus offer one free report per year to users. Checking it helps you understand your financial standing and spot errors early.

6. Why is a credit score important?

Your credit score shows how well you manage borrowed money. A higher score increases your chances of loan approval and may get you better interest rates. A low score can lead to rejections or higher borrowing costs.

7. Can I improve my credit score?

Yes, by paying your EMIs and bills on time, keeping your credit usage low, and avoiding too many loan applications. These habits slowly build trust in your profile. Improvement takes time, but consistency makes a big difference.