Borrowing money is easier than ever. A few taps on your phone and funds are credited within minutes. But with convenience comes a growing concern: how secure is your cash loan?

Many borrowers focus only on speed and approval, ignoring hidden charges, unclear terms, or unsafe lending apps. This can lead to high interest burdens, data misuse, or aggressive recovery practices that create more stress than relief. What starts as a quick financial fix can quickly turn into long-term anxiety.

Cash loan security is not just about whether your application gets approved. It is about transparency, data protection, fair pricing, and responsible borrowing. When you understand how secure lending works and what to look for in a platform, you protect both your money and your peace of mind.

In this blog, you will learn what cash loan security really means and how to borrow safely without putting your finances at risk.

TL;DR

- Cash loan security goes beyond quick approval. It includes transparent pricing, strong data protection, fair lending terms, and ethical recovery practices.

- Unregulated loan apps can expose borrowers to hidden charges, privacy misuse, and harassment. Verifying a lender’s RBI or NBFC backing is essential in India’s evolving digital lending ecosystem.

- Before applying, always check the total repayment amount, interest rate structure, app permissions, and loan agreement clarity to avoid unpleasant surprises later.

- Secured and unsecured loans carry different levels of risk. The right choice depends on whether you can provide collateral, how urgent the need is, and your repayment capacity.

- Safe borrowing ultimately comes down to discipline. Take only what you need, ensure the EMI fits your budget, and choose regulated platforms that offer transparent, short-term financial support.

What Is Cash Loan Security?

Cash loan security refers to the safeguards that protect you when you borrow money. It is not only about whether a loan requires collateral. It also includes how safely your data is handled, how transparent the pricing is, and how fair the repayment terms are.

A secure cash loan typically includes:

- Clear disclosure of interest rates and processing fees

- Transparent repayment schedule with no hidden penalties

- Regulated lender or RBI-registered NBFC backing

- Proper KYC verification process

- Encrypted handling of personal and banking data

- No unnecessary access to contacts, photos, or private information

While fast approvals and instant transfers are attractive, security should never be overlooked. For many Indian borrowers using digital lending apps, the real risk lies not in borrowing itself, but in choosing the wrong platform.

Note: Cash loan security is about protecting your money, your data, and your peace of mind before, during, and after borrowing.

Secured vs Unsecured Cash Loans

When discussing cash loan security, one of the most important distinctions is whether the loan is secured or unsecured. The level of risk and protection differs significantly between the two.

| Criteria | Secured Cash Loan | Unsecured Cash Loan |

| Collateral | Requires assets like gold, property, or FD | No collateral required |

| Risk Level | An asset can be seized if you default | No asset loss, but credit score impact |

| Interest Rates | Usually lower due to reduced lender risk | Slightly higher due to higher risk |

| Approval Speed | Slower due to asset verification | Faster with minimal documentation |

| Loan Amount | Typically higher | Usually smaller, short-term amounts |

| Best Use Case | Large planned expenses | Urgent short-term needs |

Secured loans reduce risk for lenders but increase risk for borrowers because your asset is involved. Unsecured loans are more accessible and convenient, but choosing a regulated and transparent platform becomes critical for security.

Why Cash Loan Security Matters More Than Ever?

As digital lending grows, the risks associated with unsecured borrowing have also increased. Below are the key risks linked to unsafe cash loans and the practical steps to reduce them.

1. Fraudulent or Unregulated Lending Platforms

Risk: Some apps operate without regulatory backing, offering instant approvals but engaging in hidden charges, harassment, or unethical recovery practices.

Mitigation: Borrow only from platforms partnered with RBI-registered NBFCs. Verify lender details, read app reviews, and check for a clear company presence before applying.

2. Hidden Fees and Misleading Interest Rates

Risk: Advertised interest rates may appear low, but processing fees, penalties, and additional charges can significantly increase the total repayment amount.

Mitigation: Review the full cost structure, including APR, processing fees, and late payment penalties. Ensure the total repayment amount is clearly mentioned before accepting the loan.

3. Data Privacy and Security Breaches

Risk: Some digital lending apps request unnecessary access to contacts, messages, or photos, which may be misused during recovery or in case of data leaks.

Mitigation: Check app permissions carefully before installation. Use only verified platforms that follow secure KYC processes and encrypted data handling standards.

4. Overborrowing and Debt Dependency

Risk: Quick approvals can encourage borrowers to take larger amounts than needed, increasing repayment pressure and creating repeated borrowing cycles.

Mitigation: Borrow only what fits within your monthly repayment capacity. Ensure the EMI does not compromise essential expenses or savings commitments.

5. Aggressive Recovery and Harassment Practices

Risk: Some unregulated lenders use intimidation tactics, public shaming, or constant harassment if repayments are delayed, causing emotional and financial stress.

Mitigation: Choose lenders that follow RBI guidelines for ethical recovery practices. Read user reviews about customer support and recovery behaviour before applying.

Cash loan security depends on both lender transparency and borrower awareness. Recognising these risks early helps you make safer financial decisions.

Also Read: Can Paying Bills Help Build a Credit Score?

How to Check If a Cash Loan Is Secure?

Before applying for any loan, use this practical checklist to evaluate its security. A few minutes of verification can prevent long-term financial trouble.

Before applying for any loan, use this practical checklist to evaluate its security. A few minutes of verification can prevent long-term financial trouble.

1. Verify Regulatory Backing

A secure cash loan should always be linked to an RBI-registered NBFC or bank. Regulatory backing ensures the lender follows compliance standards related to interest disclosure, recovery practices, grievance redressal, and data protection.

Check the app or website for the NBFC partner’s full legal name and registration number. Cross-verify this information on the RBI website if necessary. Legitimate lenders are transparent about their partnerships and regulatory status.

If regulatory details are missing, unclear, or difficult to verify, it increases the risk of unethical practices or a lack of accountability in case of disputes.

2. Evaluate the True Cost of Borrowing

Security is closely tied to pricing transparency. Many borrowers look only at the monthly interest rate, but the total repayment amount is what truly matters. A secure platform clearly breaks down interest rate, processing fees, GST, late penalties, and any foreclosure charges.

Calculate the total amount payable before accepting the offer. Compare this figure across multiple lenders if possible. Transparency reduces the risk of repayment shock and helps you plan your cash flow accurately.

If cost components are vaguely described or only partially disclosed, that signals weak pricing transparency.

3. Assess Data Privacy and Digital Protection

Digital loan security extends beyond money to your personal information. A credible lending platform will use encrypted systems for KYC verification and transaction processing. It will not demand unnecessary access to contacts, gallery, call logs, or messages.

Before installation, review app permissions carefully. Secure platforms collect only what is legally required for identity verification and credit assessment.

Excessive data access requests increase the risk of privacy breaches and misuse during recovery.

4. Examine Loan Agreement Clarity

A secure cash loan includes a clearly written agreement that defines repayment tenure, EMI amount, due dates, penalty structure, and grievance procedures. The language should be understandable, not ambiguous or overly technical.

Take time to read the document before digitally signing. Confirm that repayment dates align with your salary cycle and that penalty clauses are clearly specified.

Ambiguity in agreements often leads to disputes or unexpected charges later.

5. Analyse Repayment Affordability

Even the most secure platform cannot compensate for poor financial planning. Loan safety also depends on whether the EMI fits comfortably within your monthly income.

A practical rule is that total EMIs should not consume a large portion of your take-home income. Ensure essentials such as rent, groceries, utilities, and savings remain unaffected after repayment.

Borrowing within your repayment capacity reduces dependency on future loans and protects your long-term financial stability.

Cash loan security is a combination of regulatory compliance, pricing transparency, data protection, and responsible borrowing behaviour. Evaluating all four dimensions helps you make safer financial decisions.

Key Features That Make a Cash Loan Secure (Security Checklist)

Before applying for any cash loan, take a few minutes to evaluate the lender carefully. A secure loan is not just about fast approval. It is about transparency, regulation, and protection of your financial and personal data.

1. RBI Registration and Regulatory Backing

A secure cash loan provider in India should be backed by an RBI-registered NBFC or a regulated financial institution. This ensures the lender follows proper guidelines around interest disclosure, recovery practices, and borrower protection.

When a platform operates under regulatory supervision, you are less likely to face harassment, arbitrary penalties, or illegal recovery tactics. Regulatory backing creates accountability and gives you formal channels for grievance redressal if required.

If a lending app does not clearly mention its NBFC partner or regulatory status, treat it as a warning sign and verify before proceeding.

2. Clear and Upfront Interest Disclosure

Secure lenders display interest rates, processing fees, penalty charges, and total repayment amounts before you accept the loan offer. You should know exactly how much you are borrowing and how much you will repay.

When pricing details are hidden behind vague terms or revealed only after disbursement, it increases the risk of financial strain. Transparent disclosure allows you to calculate affordability and compare options confidently.

A trustworthy lender makes pricing easy to understand, not complicated to decode.

3. Transparent Repayment Schedule

A reliable loan agreement clearly outlines your repayment tenure, EMI amount, due dates, and late payment charges. Everything should be documented before funds are credited.

Clarity in repayment structure prevents confusion and protects you from unexpected penalties. When you know your exact obligations in advance, you can plan your monthly budget without anxiety.

If the repayment terms feel unclear or subject to change, reconsider the lender.

4. Strong Data Protection and Limited Permissions

Digital loan apps require KYC verification, but secure platforms collect only essential information such as PAN, Aadhaar, and bank details. They should not request unnecessary permissions like access to contacts, photos, or call logs.

Data misuse is one of the biggest risks in unsecured digital lending. Apps that demand excessive permissions may expose borrowers to privacy violations or unethical recovery practices.

Before installing any loan app, review the permissions requested and ensure the platform follows secure encryption protocols.

5. No Hidden Charges or Surprise Fees

A secure cash loan clearly outlines all associated costs, including processing fees, late penalties, foreclosure charges, and applicable taxes. There should be no hidden clauses buried in fine print.

Hidden charges can significantly increase your total repayment and create avoidable stress. Reading the complete loan agreement before accepting ensures there are no unpleasant surprises later.

If any fee feels unclear, ask for clarification before proceeding.

6. Verified Reviews and Visible Digital Presence

Trustworthy lenders maintain an active website, customer support channels, and consistent app store reviews. A registered office address and clear contact details further strengthen credibility.

A strong digital footprint reflects operational transparency. On the other hand, anonymous apps with inconsistent reviews or missing contact information increase the risk of fraud.

Taking a few extra minutes to check reviews and online presence can protect you from long-term financial trouble.

Also Read: Should You Save for an Emergency Fund or Pay Off Debt?

When Is an Unsecured Cash Loan Still a Safe Option?

An unsecured cash loan does not require collateral, which makes it accessible and fast. However, safety depends less on the loan type and more on how and why you use it. Below are the situations where an unsecured cash loan can still be a financially responsible choice.

An unsecured cash loan does not require collateral, which makes it accessible and fast. However, safety depends less on the loan type and more on how and why you use it. Below are the situations where an unsecured cash loan can still be a financially responsible choice.

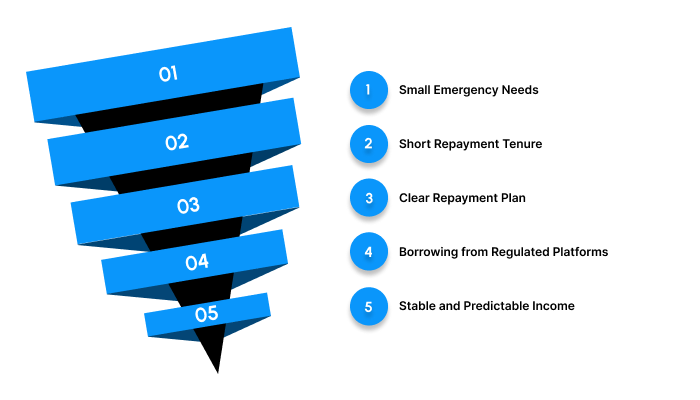

1. Small Emergency Needs

Unsecured loans are safest when used for urgent but limited expenses rather than large lifestyle upgrades or long-term commitments. The smaller the loan amount, the easier it is to manage repayments without disturbing your overall financial balance.

For example, if you need ₹8,000 for a sudden medical consultation or an urgent train ticket, repaying it over the next one or two salary cycles is far more manageable than borrowing ₹40,000 for discretionary shopping.

2. Short Repayment Tenure

Choosing a shorter repayment tenure reduces the total interest paid and prevents long-term financial dependency. A brief tenure keeps the loan temporary and focused on solving an immediate problem rather than becoming a recurring liability.

For instance, repaying a ₹10,000 loan within 30 days keeps the financial obligation contained, whereas stretching it over several months increases both cost and risk of repayment fatigue.

3. Clear Repayment Plan

A loan becomes safe only when repayment is planned before the money is borrowed. This means calculating the EMI, checking your fixed monthly expenses, and ensuring the instalment comfortably fits within your disposable income.

For example, if your monthly income is ₹45,000 and your fixed expenses total ₹32,000, you should confirm that the EMI does not strain the remaining ₹13,000 allocated for variable expenses and savings.

4. Borrowing from Regulated Platforms

Security improves significantly when borrowing from RBI-registered NBFCs or regulated digital lending partners. These platforms follow compliance norms, disclose fees clearly, and avoid unethical recovery practices.

For instance, a regulated app will clearly state the interest rate, processing fee, and penalty charges upfront, instead of adding hidden costs after disbursement or requesting unnecessary access to your phone data.

5. Stable and Predictable Income

An unsecured cash loan is safer when you have a steady income that supports timely repayments. Stability reduces the likelihood of missed EMIs and protects your credit profile.

For example, a salaried professional with a fixed monthly paycheck is generally better positioned to handle a short-term loan compared to someone relying entirely on irregular freelance payments.

Need a Secure Cash Loan Without the Risk? Pocketly Keeps It Simple

When an unexpected expense hits, the last thing you need is confusion about interest rates, hidden charges, or unsafe lending apps. You need speed, clarity, and security in one place. That is exactly what Pocketly is built for.

Here is what makes Pocketly a secure borrowing option:

- Borrow only what you actually need: Loan amounts range from ₹1,000 to ₹25,000, so you stay in control of your borrowing. You are not pushed toward larger amounts that increase repayment pressure.

- No collateral, no guarantor: There is no requirement to pledge gold, property, or involve a co-signer. The process is completely unsecured, making it accessible for students and young professionals.

- Fast approval with proper KYC: Pocketly follows a quick but compliant KYC process to verify your identity. This ensures both speed and regulatory safety, without long paperwork or branch visits.

- Instant transfer to your bank account: Once approved, funds are credited directly to your bank account. This makes it practical for urgent needs where timing matters.

- Flexible repayment that fits your budget: You can choose a repayment tenure aligned with your income cycle, helping you avoid unnecessary strain on your monthly cash flow.

- Clear and transparent pricing: Interest rates start from 2 percent per month, with processing fees typically ranging between 1 percent and 8 percent depending on your profile and loan amount. All costs are disclosed upfront so you know the total repayment before accepting the loan.

- Available 24/7 through the mobile app: You can apply, track your loan, and manage repayments anytime, without waiting for business hours.

Pocketly works with regulated NBFC partners to ensure lending follows proper guidelines and ethical practices. So when your budget falls short, you can bridge the gap confidently, knowing your loan is structured, transparent, and secure.

Conclusion

Ensuring cash loan security is one of the smartest financial decisions you can make in 2026. By verifying the lender, understanding the terms clearly, and borrowing within your repayment capacity, you reduce risk and protect both your finances and your peace of mind.

Loan security is not just about collateral. It is about transparency, regulation, data protection, and responsible usage. When you treat borrowing as a structured financial tool rather than an impulse decision, short-term credit can support you without creating long-term stress.

If unexpected expenses disrupt your cash flow, platforms like Pocketly can offer quick and regulated access to funds while maintaining transparent pricing and clear repayment terms.

Ready to borrow safely and confidently? Download the Pocketly app today on [Android] or [iOS] and access secure cash loans designed to support your financial stability.

FAQs

1. What does cash loan security mean?

Cash loan security refers to the measures that ensure a loan is safe for both the borrower and the lender. It includes whether collateral is required, how transparent the terms are, whether the lender is regulated, and how well your personal and financial data is protected.

2. Is a secured cash loan safer than an unsecured loan?

A secured loan is backed by collateral such as gold or property, which reduces risk for the lender and may result in lower interest rates. However, the borrower risks losing the pledged asset if they default. An unsecured loan does not require collateral but may have slightly higher interest rates and stricter eligibility checks.

3. How can I check if a cash loan app is safe in India?

You can check whether the lender is partnered with an RBI-registered NBFC, review the app’s ratings and feedback, read the terms and conditions carefully, and verify that interest rates and fees are clearly disclosed. Avoid apps that ask for unnecessary permissions like access to contacts or photos.

4. What are the common risks associated with cash loans?

Common risks include high interest rates, hidden charges, data privacy concerns, and borrowing more than you can comfortably repay. These risks can be reduced by choosing regulated lenders and reading the loan agreement carefully before accepting.

5. Can my personal data be misused during a loan application?

Yes, if you apply through an unregulated or fraudulent platform. Safe lending platforms use encrypted systems and follow proper KYC guidelines. Always review privacy policies and never share OTPs or sensitive details with unknown sources.