Introduction

Handling money can already feel overwhelming, and it becomes even trickier when financial terms sound similar but have different meanings. Many people are familiar with banks, but when words like building society vs credit union come up, the picture isn’t always clear.

For students, young professionals, or anyone starting their financial journey, this confusion can lead to uncertainty about where to save, how to borrow affordably, or which institution truly puts their needs first. Choosing the wrong option could result in higher costs, fewer benefits, or missed opportunities to build financial security.

That’s why understanding the difference between building societies and credit unions is so important. Both are designed to serve their members rather than maximise profits, but they operate in unique ways. In this blog, we’ll break down what each one is, highlight their key differences, and explain why knowing about them can make you a more competent money manager.

At a Glance

- Building societies and credit unions are both member-owned financial institutions that prioritise people over profits.

- Building societies (common in the UK) mainly focus on long-term savings and home loans, reinvesting profits to improve member services.

- Credit unions are smaller, community-driven cooperatives that provide affordable short-term personal loans, emergency loans, and basic savings options.

- While India doesn’t have these exact institutions, co-operative banks and credit societies work similarly. They highlight fair, transparent, and community-first finance models.

What is a Building Society?

A building society is a financial institution, primarily found in the United Kingdom, that is owned by its members, who are the individuals who save with it or borrow from it. Unlike traditional banks that exist to maximise profits for shareholders, building societies reinvest earnings to give members better savings rates, affordable loans, and improved services.

Their primary role is to help people save money and access loans, especially for buying homes.

Common services include:

- Savings accounts with competitive interest rates.

- Home loans (mortgages) are available at lower costs compared to those offered by commercial banks.

- Basic financial services such as debit cards or small personal loans.

While India doesn’t have “building societies” in the UK sense, it does have co-operative banks and housing finance societies that work similarly. For example, many state cooperative banks and urban cooperative banks are community-owned, serving their members by offering savings accounts and affordable loans for housing or agriculture. These are India’s closest equivalents to a building society.

So, when you think of a building society, imagine a co-operative style bank in India, not designed to chase profits, but to support its members’ financial needs.

Now that you have an idea of how building societies work and their closest Indian equivalents, let’s explore another member-first financial model: the credit union.

Must Read: How to Start Building Credit at The Age of 18

What is a Credit Union?

A credit union is a member-owned financial cooperative where individuals pool their money to help one another save and borrow. Unlike banks that operate mainly for profit, credit unions exist to serve their members. This means any surplus they make is returned in the form of lower loan rates, higher savings interest, or better services.

The idea is simple. Members contribute funds, which are then used to provide affordable loans to other members who need them. Because of this community-driven approach, credit unions are often trusted for their low-cost personal loans, savings schemes, and financial guidance.

In countries like the US, credit unions are widely used for small loans, car financing, or even daily banking, often at lower costs than commercial banks.

While the term “credit union” isn’t commonly used in India, we have similar institutions, such as credit cooperative societies, self-help groups (SHGs), and cooperative banks. These organisations are community-based, member-driven, and often help people in rural areas, small businesses, or specific groups (like farmers or workers) access savings and affordable loans.

For example, in India, a farmer’s cooperative society may allow members to save regularly and borrow at low interest rates to purchase seeds or equipment. That’s essentially the same principle a credit union follows globally.

With both concepts introduced, the next step is to compare how building societies and credit unions side by side, allowing you to see their differences clearly.

Must Read: How Credit Risk Models Help Borrowers Get Loans Quickly

Building Society vs Credit Union

Both building societies and credit unions are member-owned financial institutions that exist to support their members rather than to maximise profits. While they share a common “people-first” approach, their goals, size, and services differ in essential ways. Understanding building society vs credit union can help you see how each one fits into the wider financial system.

1. Ownership and Purpose

Building Societies are generally larger institutions, especially in the UK, and are designed to help people save and become homeowners. Their primary focus is on offering affordable mortgages and promoting long-term savings. Since they don’t have external shareholders, any profits they generate are reinvested to enhance member benefits, such as providing better interest rates.

Credit Unions are smaller and more community-driven. Their core purpose is to give members access to affordable credit and encourage savings within the group. They are built on cooperation. Members help each other by pooling funds, which are then lent back to those in need, usually at lower rates than commercial banks.

2. Scale of Operations

Building Societies can operate at a national level and often resemble small or mid-sized banks in terms of size. Some building societies have millions of members and offer services across entire countries, making them more formal and structured in their operations.

Credit Unions are usually localised and serve specific groups or communities. Membership could be restricted to individuals living in a specific area, working in a particular profession, or belonging to a specific organisation. Because of this, their operations are smaller in scale, but they are often more personal and tailored to members' needs.

3. Products Offered

Building Societies focus heavily on long-term financial products, primarily housing loans (mortgages) and savings accounts. They may also offer additional services such as insurance, personal loans, and debit cards, but home ownership and savings remain their central mission.

Credit Unions specialise in short-term financial products such as small personal loans, emergency loans, and basic savings accounts. These are designed to help members cover immediate needs, like medical expenses, education, or day-to-day costs, while also promoting financial discipline through savings.

4. Accessibility

Building Societies often operate like banks and therefore may have stricter eligibility requirements for loans or mortgages. The process can feel more formal, involving paperwork, credit checks, and compliance with regulatory frameworks.

Credit Unions are more approachable because they are based on community membership and mutual trust. While they also follow rules, the focus is on helping members rather than applying rigid banking criteria. This makes credit unions more inclusive, particularly for people who may struggle to access mainstream financial services.

5. Profit Distribution

Building Societies reinvest their profits into the organisation. Instead of paying dividends to shareholders, they use earnings to improve savings rates, reduce mortgage costs, and enhance member services. The benefit is derived indirectly through improved financial products.

Credit Unions usually share their surplus directly with members, either as dividends or through lower interest rates on loans. This makes members feel the benefits more directly, since the savings and earnings are returned to the very people who contributed.

While their differences are apparent, these two institutions also share common values that set them apart from traditional banks. Let’s look at the similarities.

Similarities Between Building Societies and Credit Unions

Although building societies and credit unions differ in terms of size, focus, and operations, they share several significant similarities that distinguish them from traditional banks. These similarities explain why both institutions are often described as “member-first” financial organisations.

1. Member-Owned and Democratic

Both are owned by their members rather than outside shareholders. This means every member typically has a say in how the institution is run, often on a one-member-one-vote basis, regardless of how much money they’ve deposited or borrowed.

2. People Over Profits

Instead of focusing on generating profits for investors, building societies and credit unions prioritise serving their members’ financial needs. Surpluses are either reinvested to improve services or shared back with members in the form of lower interest rates or higher returns on savings.

3. Community-Centred Approach

Both institutions are closely tied to the communities they serve. Building societies were traditionally formed to help groups of people buy homes, while credit unions were designed to support communities with affordable loans. In both cases, the idea of cooperation and mutual benefit lies at the heart of their existence.

4. Accessible Financial Products

Unlike some commercial banks that may target only high-value clients, both building societies and credit unions offer services tailored for everyday people. Their products, whether savings accounts, loans, or mortgages, are structured to be affordable and accessible to ordinary members.

5. Financial Education and Support

Many building societies and credit unions also focus on improving financial literacy. By encouraging members to save, borrow responsibly, and plan for the future, they promote long-term financial well-being rather than focusing solely on short-term transactions.

Recognising these similarities is essential, but the bigger question is, why does this matter to students and young professionals in India today?

Must Read: Understanding Promissory Notes for Personal Loans

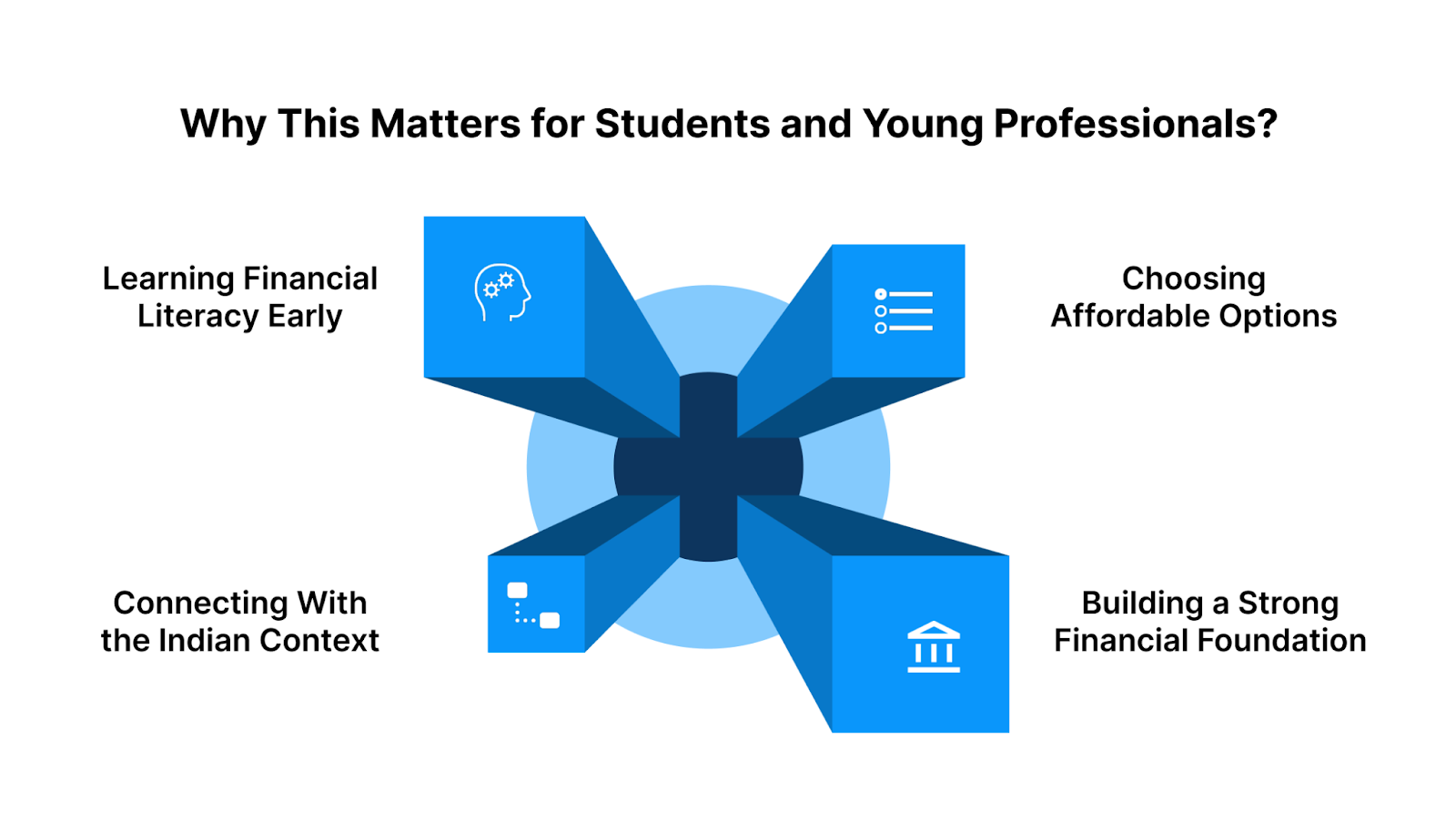

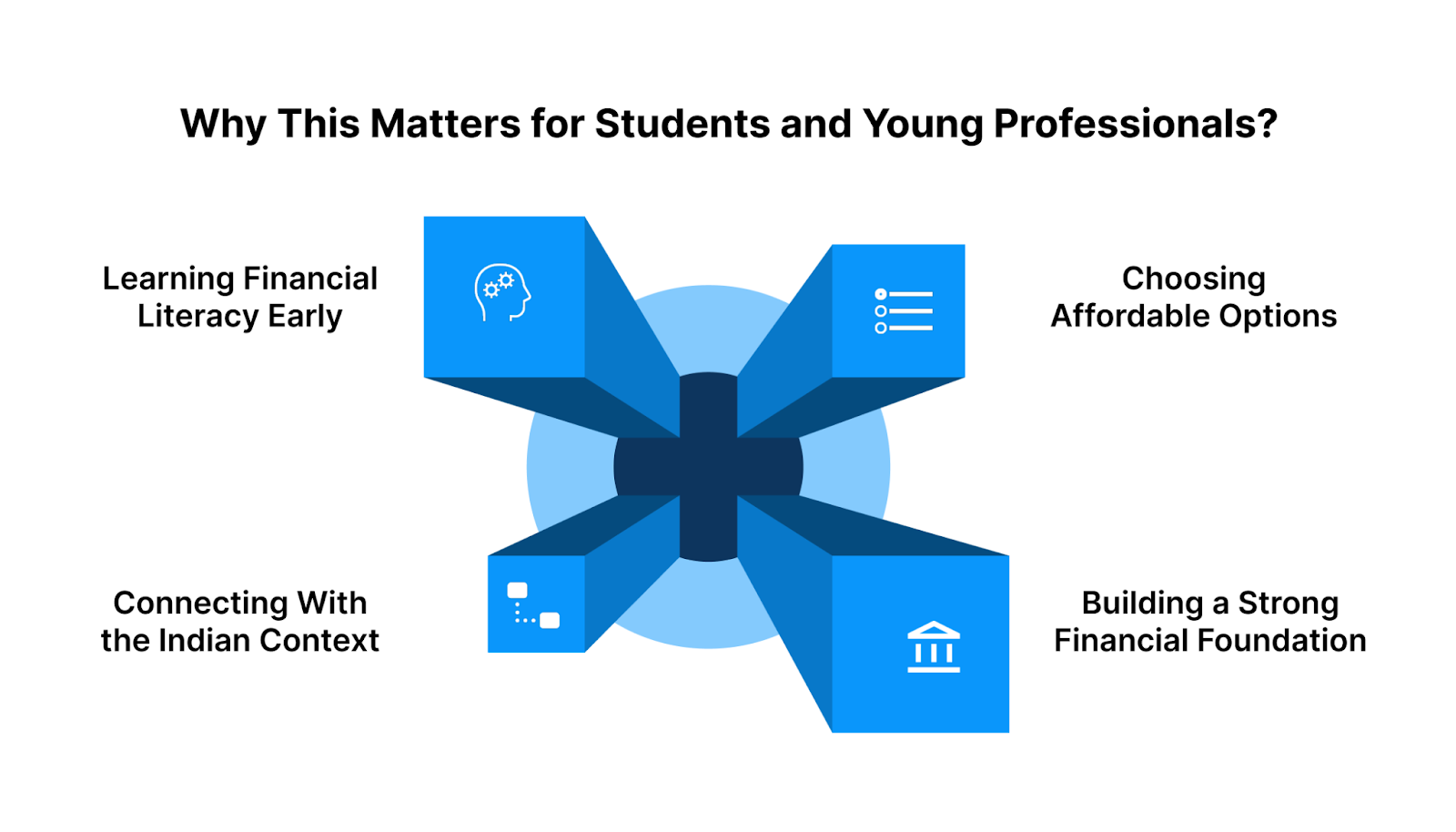

Why This Matters for Students and Young Professionals?

Building societies and credit unions might feel like financial concepts that only matter in the UK or the US. However, for students and young professionals in India, understanding how these institutions operate remains valuable. It highlights how different models of finance, such as cooperative, member-owned, or profit-driven, affect the way people access money and manage their financial needs.

1. Learning Financial Literacy Early

The college and early career years are when most people begin managing their own finances. By studying examples like building societies and credit unions, students can see how financial institutions are structured, who they serve, and why some are more people-friendly than others. This awareness enables you to make more informed decisions when comparing banks, NBFCs, or digital lenders in India.

2. Choosing Affordable and Accessible Options

The biggest lesson from these models is that financial services don’t have to be profit-first. Credit unions demonstrate how affordable loans can be made available to community members. Building societies demonstrate how collective ownership can make long-term goals, such as homeownership, more achievable. For young Indians, this highlights the importance of selecting lenders and financial products that are transparent, fair, and easily accessible.

3. Connecting With the Indian Context

In India, although we don’t have building societies or credit unions in the same form, we do have equivalents, such as co-operative banks, credit co-operative societies, and NBFCs. These institutions are community-driven and often offer services that are more accessible than those of traditional banks. For students and first-time earners, knowing these options exist can prevent them from relying only on expensive credit cards or informal borrowing.

4. Building a Strong Financial Foundation

The real takeaway is that the financial choices made today, whether borrowing for education, managing rent, or covering emergencies, significantly impact your credit history and future independence. Understanding global models, such as building societies and credit unions, helps students appreciate the importance of responsible borrowing and saving, even if the specific institutions differ in India.

While learning from global models is valuable, young Indians also need financial solutions tailored to their own needs. This is where Pocketly comes in.

Must Read: Best Way to Use a Credit Card to Build Credit Score

Pocketly: A Smart Way to Handle Finances

While building societies and credit unions show how communities can make finance more accessible, students and young professionals in India often need a quicker, more digital-first solution. That’s where Pocketly comes in. This is a lending platform explicitly designed to support young Indians who face short-term financial gaps.

1. Small, Flexible Loan Amounts

Pocketly offers instant personal loans starting from as little as ₹1,000 and going up to ₹25,000. This makes it perfect for covering everyday student or professional needs, such as exam fees, travel, rent, or emergency expenses, without taking on unnecessary debt.

2. No Collateral, 100% Digital Process

You don’t need to pledge property or valuables. With quick KYC and a fully online application, approvals are simple, and you avoid the hassle of paperwork.

3. Fast Disbursal to Your Bank Account

Once approved, the money is transferred directly to your bank account. You can use it immediately via UPI, debit card, or net banking, providing you with financial freedom when you need it most.

4. Transparent and Fair Costs

Pocketly believes in clarity. Interest starts at 2% per month, with processing fees ranging from 1% to 8%, and no hidden charges. You always know exactly what you’re paying.

5. Flexible Repayments

Repaying through UPI, cards, or net banking is quick and convenient. The flexibility ensures you can stay on track without extra stress.

6. Building Credit History

Every repayment you make is reported to credit bureaus, helping you establish a positive financial record early. This builds trust with lenders and improves your chances of accessing larger loans later in life.

7. Peace of Mind During Cash Crunches

Instead of worrying about how to find money at the last moment, Pocketly gives you a reliable safety net. That means more time and energy for your studies, work, and personal growth.

By combining the principles of fairness and accessibility with a fully digital approach, Pocketly shows how modern lending can truly work for students and young professionals. But before we wrap up, let’s recap the big picture.

Conclusion

Understanding the differences between building societies and credit unions reveals how financial institutions can prioritise people's needs, whether by offering fairer loans, reinvesting profits for members, or providing community-driven support. Both models highlight the importance of accessible, transparent, and trust-based finance.

For students and young professionals in India, however, the challenge is different; their financial needs are often small, urgent, and fully digital. That’s where Pocketly makes a real difference.

With instant loans starting from just ₹1,000, zero collateral, transparent costs, and flexible repayments, Pocketly gives you the confidence to handle unexpected expenses while also helping you build credit for the future. Don’t let sudden expenses hold you back.

Download the Pocketly app today on iOS or Android and take control of your finances with smart, hassle-free loans designed for students and young earners.

FAQs

Q1. Are building societies and credit unions the same as banks?

No. While they offer similar services, such as savings and loans, building societies and credit unions are member-owned and non-profit oriented, unlike banks, which are shareholder-driven and profit-focused.

Q2. Can I join a building society or credit union in India?

Not directly in the same way as in the UK or the US. In India, cooperative banks and credit cooperatives operate similarly to credit unions, providing community-based financial services.

Q3. Which is better: a building society or a credit union?

It depends on your needs. If you want long-term savings or home loans, building societies are a more suitable option. If you need short-term, affordable personal loans or community-based support, credit unions are often a better fit.

Q4. How do building societies and credit unions use profits?

Both reinvest profits for members. Building societies typically offer improved interest rates and services, while credit unions often provide dividends or lower loan rates directly to their members.

Q5. Why should students and young professionals care about this?

Both institutions emphasise fairer, community-focused finance, serving as a reminder that alternatives to high-interest loans and profit-driven banks exist. For young Indians, Pocketly brings this principle into the digital age by offering instant, small-ticket loans designed for modern needs.