Most people don’t have a spending problem; they have a wealth-building problem. Money comes in, bills get paid, maybe a little is saved, and then the month resets. Years pass, but financially, nothing really changes. No real growth. No safety net. No feeling of being ahead.

That’s frustrating and quietly stressful. Because deep down, you know working harder is not the same as getting wealthier. Yet most financial advice is either too generic, like “just save more”, or too complex to actually follow. Without a clear strategy, it’s easy to stay stuck in survival mode instead of building assets that grow over time.

The truth is, wealth is not built through luck, big salaries, or risky bets. It’s built through consistent, smart decisions that compound. In this blog, we will break down what building wealth really means, the core principles behind it, and practical steps you can start using to grow your money with clarity and confidence.

TL;DR

- Building wealth is not about earning more but consistently turning income into assets that grow over time.

- A strong foundation includes budgeting, an emergency fund, insurance, and eliminating high-interest debt first.

- Long-term investing through diversified options like SIPs, PPF, equity, and gold helps your money compound steadily.

- Wealth grows faster when you increase investments with income hikes and avoid lifestyle inflation.

- Staying consistent, avoiding panic during market dips, and thinking long term are what truly separate wealthy investors from everyone else. e

What Does Building Wealth Really Mean?

Many people think building wealth simply means earning a high income, but the two are not the same. You can make good money and still struggle financially if you spend everything you earn.

Income is the money you receive from a job, business, or other sources. Wealth, however, is the value of what you own after subtracting what you owe. It reflects your long-term financial strength, not just your monthly earnings.

Building wealth focuses on growing assets that increase in value or generate income over time. These may include investments, savings, property, or businesses. Unlike income, which depends on active work, wealth continues to support you even when you are not working.

Three key elements shape wealth building:

- Saving: Setting aside a portion of your income instead of spending it all

- Investing: Using your money to buy assets that grow over time

- Protecting: Managing risks through emergency funds and insurance

The goal is to create financial stability and future freedom, where your money works for you instead of you always working for money.

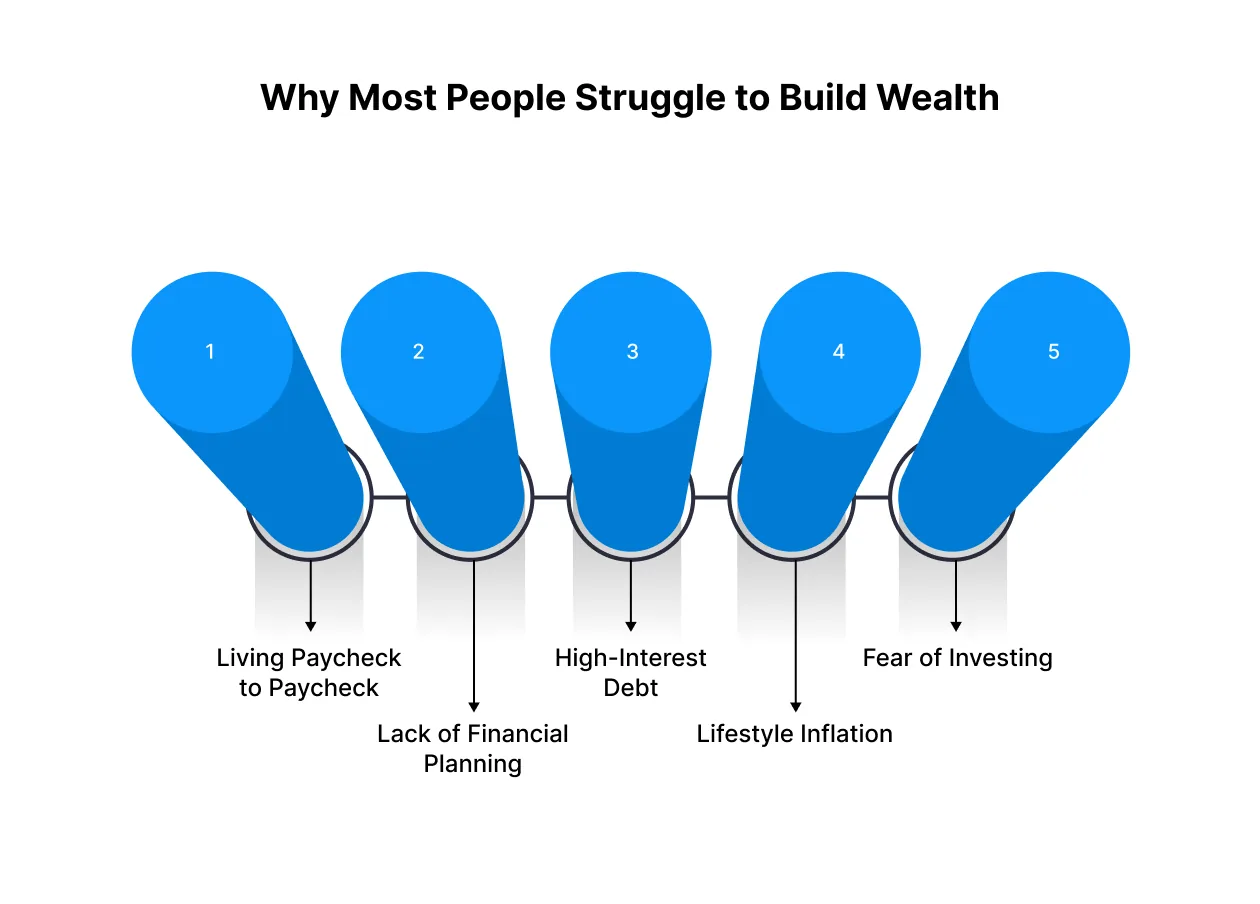

Why Most People Struggle to Build Wealth

Building wealth sounds simple in theory: earn more, spend less, and invest the difference. In reality, many people remain stuck in a cycle where their income rises but their net worth barely moves. The challenge is rarely a lack of earning potential.

Building wealth sounds simple in theory: earn more, spend less, and invest the difference. In reality, many people remain stuck in a cycle where their income rises but their net worth barely moves. The challenge is rarely a lack of earning potential.

More often, it’s a mix of financial habits, mindset gaps, and structural money mistakes that quietly block long-term growth.

Here are the deeper reasons wealth-building feels out of reach for so many.

1. Living Paycheck to Paycheck

One of the biggest reasons people struggle to build wealth is that most of their income goes toward covering monthly expenses. When rent, groceries, EMIs, and bills consume nearly everything you earn, there’s little left to save or invest.

For example, a young professional earning a decent salary may still feel financially stuck because lifestyle costs in urban areas keep rising. Even a small unexpected expense, like a medical bill or car repair, can wipe out their savings and push wealth-building further out of reach.

2. Lack of Financial Planning

Without a clear financial plan, it’s easy to drift from one expense to another without making real progress. Many people focus only on short-term needs and overlook long-term goals like investing, retirement planning, or building assets.

For instance, someone might consistently save a little money each month but leave it in a basic savings account. While it feels responsible, the money isn’t growing enough to outpace inflation, which slows down their ability to build real wealth over time.

3. High-Interest Debt

Debt, especially high-interest debt like credit cards or personal loans, can quietly block wealth creation. A large portion of income ends up going toward interest payments instead of savings or investments.

Imagine carrying a credit card balance month after month. Even if you’re earning well, the interest keeps adding up, making it harder to free up money for wealth-building activities like investing in mutual funds, stocks, or property.

4. Lifestyle Inflation

As income increases, spending often rises just as quickly. This is known as lifestyle inflation, and it prevents people from using salary growth as a tool for building wealth.

For example, after getting a raise, someone might upgrade their phone, move to a more expensive apartment, or dine out more often. While these upgrades improve comfort, they can delay long-term financial progress if additional income isn’t partly directed toward savings and investments.

5. Fear of Investing

Many people hesitate to invest because they fear losing money or don’t fully understand how investments work. As a result, they keep their money in low-risk, low-return options, which limits wealth growth.

For instance, someone might avoid equity investments due to market volatility, choosing to keep all their savings in a bank account. While this feels safe, it reduces the opportunity for higher returns that are often necessary to build significant wealth over the long term.

Also read: How to Manage Monthly Expenses Smartly in 2025

A Step-by-Step Framework for Building Wealth Consistently

Building wealth is not about earning a huge salary overnight. It is about following a clear system with disciplined financial habits over time. The steps below break wealth creation into practical actions you can start implementing immediately, regardless of your current income level.

Step 1: Define clear financial goals

Wealth building starts with clarity. Vague intentions like “I want to save more” don’t create action. Instead, set specific goals with numbers and timelines, such as building a ₹5 lakh emergency fund in two years or creating a ₹1 crore retirement corpus by age 55.

Clear goals help you calculate how much you need to save or invest each month. They also keep you motivated because you can measure progress instead of guessing.

Example: Riya, a 27-year-old marketing professional, decides she wants to buy a ₹10 lakh car in four years. She now knows she must set aside a fixed monthly amount instead of spending randomly and hoping savings “just happen.”

Step 2: Track your income and expenses

Understanding where your money goes is the foundation of financial growth. Track your spending for at least two to three months to identify patterns.

Break expenses into three categories: essentials like rent and groceries, lifestyle spending like eating out and shopping, and irregular costs like travel or repairs. This is not about cutting all fun. It is about spotting areas where small adjustments can free up money for investments.

Example: After tracking expenses, Arjun realises he spends nearly ₹4,000 a month on food delivery. By cooking more often, he redirects half that amount into a mutual fund SIP.

Step 3: Build an emergency fund first

Before investing heavily, create a financial safety net. An emergency fund covering three to six months of essential expenses protects you from relying on loans or selling investments during unexpected events like job loss or medical emergencies.

Keep this money in a safe and easily accessible place like a savings account or liquid mutual fund, not in stocks or long-term investments.

Example: When Sneha’s company delays salaries for two months, she manages her rent and bills comfortably using her emergency fund instead of taking a high-interest personal loan.

Step 4: Eliminate high-interest debt

High-interest debt can quietly destroy wealth because the interest grows faster than most investments. Credit cards, payday loans, and some personal loans often carry very high rates.

Focus on paying off the most expensive debt first while continuing minimum payments on others. Once cleared, redirect the amount you were paying as EMIs into savings and investments.

Example: Kunal was paying ₹3,000 every month in credit card interest. After clearing the balance, he started investing that same ₹3,000 monthly, turning a financial drain into wealth creation.

Step 5: Start investing consistently

You do not need a large amount to begin investing. Consistency matters more than size. Regular monthly investments benefit from compounding, where your returns start generating their own returns over time.

Automating investments through SIPs helps you stay disciplined and removes the temptation to skip months. Starting early gives your money more time to grow, even if the amounts are small.

Example: Megha starts a ₹2,000 monthly SIP at age 24. Her friend waits until 32 to invest ₹5,000 monthly. Even though Megha invests less each month, she can still end up with a similar or larger corpus because she started earlier.

Step 6: Increase your income over time

While saving is important, there is a limit to how much you can cut. Increasing your income creates more room to invest and grow wealth faster. This could mean upskilling, negotiating a raise, switching jobs, freelancing, or starting a side income stream.

When your income increases, avoid upgrading your lifestyle immediately. Instead, direct a large portion of the extra money toward investments.

Example: After getting a ₹10,000 salary hike, Devika increases her SIPs by ₹7,000 instead of upgrading her phone or moving to a more expensive apartment.

Step 7: Diversify your investments

Putting all your money into one asset can be risky. Diversification spreads your money across different asset types such as equity, debt, gold, and fixed income products. This reduces the impact if one investment performs poorly.

A balanced portfolio helps you manage risk while still aiming for steady growth.

Example: Instead of investing everything in stocks, Rohit splits his money between equity mutual funds, a PPF account, and some gold. When the stock market dips, his other investments help balance the loss.

Best Investment Options for Long-Term Wealth Creation in India

Building wealth requires choosing the right mix of investments based on your risk tolerance, time horizon, and financial goals. Some options offer higher growth potential with more volatility, while others focus on stability and capital protection. The key is balancing growth and safety rather than relying on a single investment type.

| Investment Option | Risk Level | Return Potential | Time Horizon | Liquidity | Suitable For |

| Equity Mutual Funds (SIP) | Medium | High | 5+ years | Moderate | Salaried individuals building long-term wealth |

| Direct Stocks | High | Very High | 7+ years | High | Investors with market knowledge and risk tolerance |

| Public Provident Fund (PPF) | Very Low | Moderate | 15 years | Low | Conservative investors seeking safe, tax-efficient growth |

| National Pension System (NPS) | Low–Medium | Moderate–High | Until retirement | Low | Long-term retirement-focused investors |

| Fixed Deposits (FDs) | Low | Low | 1–5 years | Medium | Capital protection and short-term goals |

| Gold (Sovereign Gold Bonds / ETFs) | Medium | Moderate | 5+ years | Medium | Portfolio diversification and inflation hedge |

| Real Estate | Medium–High | High | 8+ years | Very Low | Investors with large capital and long holding capacity |

| Index Funds | Medium | High | 5+ years | Moderate | Passive investors seeking market-linked growth |

| Debt Mutual Funds | Low–Medium | Moderate | 3–5 years | Moderate | Investors balancing risk and stable returns |

Also read: Best Expense Tracker Apps In India For 2025

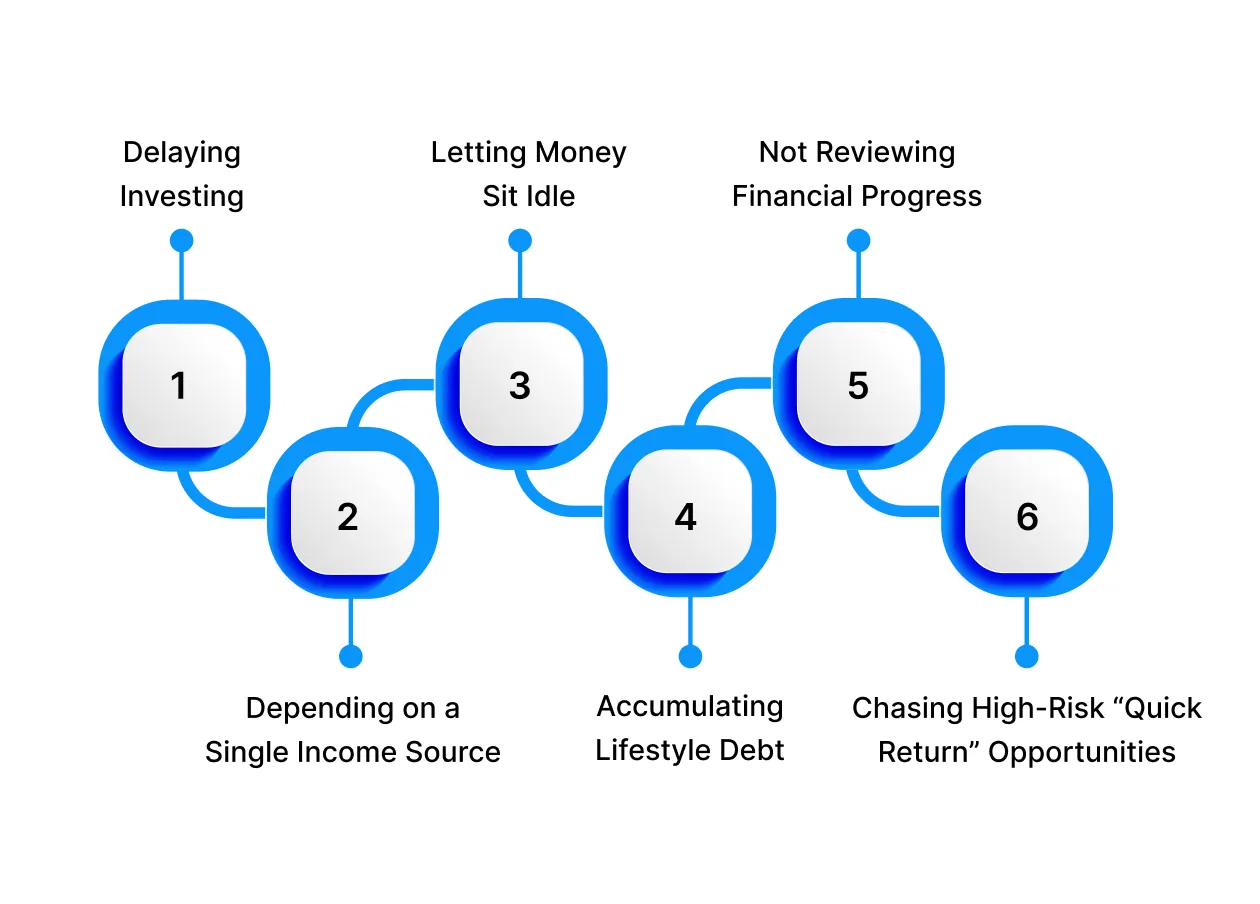

Commonwealth-Building Mistakes That Slow You Down

Building wealth is not only about what you do right, but also about the mistakes you avoid along the way. Certain financial habits quietly delay progress, reduce compounding potential, or increase risk, making it harder to reach long-term goals. Recognising these pitfalls early helps you protect your money and stay on track.

Building wealth is not only about what you do right, but also about the mistakes you avoid along the way. Certain financial habits quietly delay progress, reduce compounding potential, or increase risk, making it harder to reach long-term goals. Recognising these pitfalls early helps you protect your money and stay on track.

1. Delaying Investing

Risk: Waiting for a higher salary, a promotion, or the “right time” reduces the years your money has to compound. The longer you wait, the harder it becomes to reach long-term goals.

Mitigation: Start with small, consistent investments regardless of income level. Even modest SIPs or retirement contributions build momentum over time.

2. Depending on a Single Income Source

Risk: Relying only on salary slows wealth creation and increases financial vulnerability if income is disrupted.

Mitigation: Develop additional income streams such as freelance work, dividends, rental income, or side businesses to accelerate wealth growth and reduce risk.

3. Letting Money Sit Idle

Risk: Keeping large amounts of money in low-interest savings accounts causes your wealth to lose value due to inflation.

Mitigation: Allocate surplus funds into growth-oriented assets like equity funds, retirement accounts, or other investments that have the potential to outpace inflation.

4. Accumulating Lifestyle Debt

Risk: Using credit for non-essential spending leads to high-interest repayments that reduce your ability to invest and build assets.

Mitigation: Limit debt to value-creating purposes and avoid EMIs for depreciating or lifestyle purchases. Prioritise clearing high-interest liabilities quickly.

5. Not Reviewing Financial Progress

Risk: Ignoring your investments and financial plan can lead to misaligned portfolios, excessive risk, or underperformance over time.

Mitigation: Review your financial plan and asset allocation at least once a year. Rebalance investments to stay aligned with your goals and risk tolerance.

6. Chasing High-Risk “Quick Return” Opportunities

Risk: Get-rich-quick schemes often promise unrealistic returns and expose you to fraud, extreme volatility, or permanent capital loss.

Mitigation: Focus on long-term, diversified investing strategies. Evaluate opportunities based on fundamentals, not hype or social media trends.

Facing a Cash Crunch While Growing Your Wealth? Pocketly Helps You Stay on Course

When you’re focused on building wealth, your money is usually tied to savings, investments, and future goals. But unexpected expenses like medical emergencies, urgent travel, or necessary repairs can suddenly disturb your financial flow and force you to pull money out of long-term plans.

In situations like these, Pocketly can serve as a short-term financial cushion, helping you manage immediate expenses without completely throwing off your wealth-building progress.

Here’s how Pocketly can support you:

- Borrow only the amount you need: Get access to small loan amounts ranging from ₹1,000 to ₹25,000, so you don’t end up with more debt than required.

- No collateral or guarantor needed: These loans are unsecured, which means you don’t have to pledge assets or depend on someone else to qualify.

- Quick approval process: With a simple KYC-based verification, loan decisions are made fast without complicated paperwork.

- Direct bank transfer: Once approved, the funds are transferred straight to your bank account, making it useful for time-sensitive expenses.

- Repayment that fits your budget: Flexible tenure options allow you to choose a plan that works comfortably alongside your monthly financial commitments.

- Clear and transparent charges: Interest rates start from 2% per month, and processing fees are disclosed upfront, so there are no surprise costs later.

- Access anytime through the app: You can apply, monitor, and manage your loan 24/7 using the Pocketly mobile app.

When used carefully, Pocketly can help you handle temporary money gaps while allowing you to stay focused on your bigger, long-term wealth goals.

Conclusion

Building wealth is not about quick wins or perfect timing. It is about consistent habits, smart decisions, and staying committed to long-term goals. When you track your money, invest regularly, and make intentional spending choices, you create a strong financial foundation that grows over time.

There will be moments when unexpected expenses or cash gaps make things feel unstable. The key is to handle these situations calmly without derailing your bigger financial plans. Having the right tools and support can help you stay on track while you continue building toward financial freedom.

Download the Pocketly app now on iOS or Android to access quick funds and stay in control when your expenses exceed your budget. With flexible loan options and transparent pricing, Pocketly ensures you are always prepared for life’s financial surprises.

FAQs

1. What does building wealth actually mean?

Building wealth means growing your money and assets over time so they generate income, increase in value, and provide long-term financial security. It goes beyond just earning a salary and focuses on saving, investing, and making smart money decisions.

2. How is building wealth different from saving money?

Saving money is about setting aside cash for short-term needs or emergencies. Building wealth involves using that saved money to invest in assets like stocks, businesses, or property so your money can grow and work for you over time.

3. How much should I invest if I am just starting to build wealth?

You can start with any amount you are comfortable with, even small monthly investments. The key is consistency, patience, and increasing your investments as your income grows rather than waiting until you have a large lump sum.

4. Is it possible to build wealth with an average income?

Yes, wealth building is more about habits than high income. Regular investing, controlled spending, avoiding high-interest debt, and giving investments time to grow can help even people with average incomes build strong financial foundations.

5. How long does it usually take to build noticeable wealth?

Wealth building is a long-term process and often takes years, not months. With consistent investing and compounding returns, many people start seeing meaningful growth after five to ten years, with larger results over decades.