Ever feel like your salary disappears the moment it hits your account? You hustle hard, meet deadlines, and still wonder why there’s barely anything left for savings or even small pleasures. The problem is simple: without a smart plan, money slips away quietly, and the new Union Budget 2026‑27 has only changed the rules. Tax tweaks, TCS reductions, and spending shifts mean yesterday’s budgeting habits may no longer work.

This leaves many young professionals stuck: overspending on lifestyle, under-saving for emergencies, or missing opportunities to invest smartly. But it doesn’t have to be that way. With a practical budget designed around these new changes, you can take control, save consistently, and still enjoy life without guilt.

In this blog, you’ll learn how to plan your money post-budget so every rupee has a purpose and works for your future.

TL;DR

- Budget rules have shifted: Taxes, TCS, and incentives from the 2026‑27 budget impact your earnings, spending, and savings.

- Track every rupee: Fixed bills, lifestyle costs, and small daily spends can silently drain your income.

- Save before you spend: Treat emergency funds, investments, and future goals as non-negotiables.

- Tailor your plan: Students, homeowners, freelancers, and small business owners are affected differently; adjust your budget accordingly.

- Use smart tools: Apps, spreadsheets, or digital trackers help manage spending gaps without disrupting long-term goals.

Union Budget 2026‑27: What Young Professionals Need to Know

The Union Budget 2026‑27 introduces several key changes that impact salaried professionals, students, homeowners, and small businesses. From tax rules to infrastructure spending, TCS reductions, and SME incentives, these changes influence your income, expenses, and financial planning.

The table below summarises the most important updates and their practical impact, so you can quickly understand what’s new and how it affects you.

| Category | Change in Budget 2026‑27 | Who Benefits | Practical Impact |

| Income Tax | Slabs unchanged; New IT Act from April 2026 | Salaried professionals, taxpayers | Stable take-home pay, simpler filing, reduced compliance stress |

| Capital Spending & Infrastructure | ₹12.2 lakh crore; 7 high-speed rail corridors; urban & transport upgrades; freight corridors & waterways | Professionals, commuters, small businesses | Faster travel, better logistics, improved property value near growth corridors |

| TCS Reductions | Foreign education & medical payments, overseas travel packages cut to 2% | Students, travellers, and families sending money abroad | Lower costs, more disposable income, and easier international payments |

| SME & Startup Support | ₹10,000 crore SME Growth Fund; simplified compliance (TReDS, exports); focus on tech, manufacturing, green energy | Entrepreneurs, small businesses, startups | Easier access to funding, less paperwork, and growth opportunities |

| Customs Duty & Imports | Personal imports reduced to 10%; exemptions on cancer/rare disease medicines; industrial imports exemptions for lithium-ion batteries & solar components. | Individuals, healthcare patients, manufacturers | Cheaper electronics & lifestyle goods, affordable medicines, support for industries |

| Education & Skills | STEM hostels, AVGC labs, sports programs | Students, young professionals | Better learning opportunities, skill development |

| Healthcare | Allied health workforce expansion, medical tourism hubs | Healthcare professionals, patients | More jobs, better access to services |

| Technology & Manufacturing | Biopharma SHAKTI, semiconductor expansion | Professionals, entrepreneurs, and industry | Innovation, employment, business growth |

| Transport & Connectivity | High-speed rail, freight corridors, waterways | Commuters, businesses | Easier travel, improved logistics |

| Comparison with the Previous Year | Added: new IT Act, TCS cuts, 7 high-speed rail corridors, ₹10,000 crore SME fund, tech & biopharma initiatives; Unchanged: tax slabs, core infrastructure & healthcare focus. | Everyone | Budget builds on last year, reduces select costs, and strengthens support for students, SMEs, and professionals |

Why the New Budget Matters to You?

The Union Budget 2026‑27 isn’t just government numbers; it directly influences your daily finances, lifestyle, and future plans. Whether you’re a young professional, student, homeowner, or freelancer, understanding these changes helps you make smarter financial choices and plan ahead.

1. Your Salary and Take-Home Pay

- Income tax slabs remain the same, so there’s no sudden jump in your taxes.

- The new simplified filing system, starting in April 2026, reduces paperwork and avoids last-minute surprises.

- TCS reductions on foreign education and travel mean students and young professionals save extra on tuition fees, international trips, or work-related travel.

- These savings can be reinvested in skill development, personal goals, or emergency funds, giving you more financial flexibility.

2. Living Costs and Everyday Expenses

- With ₹12.2 lakh crore in capital expenditure, new roads, metro projects, and high-speed rail corridors are coming up.

- Better infrastructure can cut commuting costs and time, and areas near new projects may see property values rise.

- Knowing these trends helps you budget for rent, EMIs, or future home investments wisely, avoiding last-minute financial stress.

3. Students and Early Career Professionals

- The government’s focus on education, skill-building, and emerging tech labs opens opportunities for scholarships, workshops, and certification programs.

- If you’re pursuing higher education or professional courses, the budgeted support and TCS reductions can reduce costs and improve ROI on your learning.

- Planning your monthly expenses around these opportunities ensures you invest in your career without compromising savings.

4. Homeowners and Renters

- Infrastructure upgrades often increase real estate values near growth corridors.

- Homeowners can anticipate property appreciation, while renters may need to plan for possible rent increases.

- Budgeting for EMIs, utilities, and maintenance ensures that housing costs don’t eat into your lifestyle or savings.

5. Small Business Owners and Freelancers

- SMEs and startups benefit from lower import duties, tax incentives, and easier compliance.

- Reduced operational costs improve cash flow, letting you reinvest in growth, marketing, or emergency reserves.

- A well-planned budget ensures you stay financially secure even during slow revenue months, helping your business remain sustainable.

6. Why You Should Update Your Personal Budget Now

- The 2026‑27 budget creates both opportunities and potential cost pressures, from lifestyle changes to commuting and education expenses.

- Updating your personal budget ensures you can take advantage of benefits like TCS reductions or startup incentives, while staying prepared for unexpected costs.

- In short, budgeting turns government policy changes into practical actions for your daily life, so you remain in control of your money instead of reacting to it.

Bottom line: The new budget affects your income, expenses, and financial choices. Understanding its implications allows you to plan smarter, save more, and align your daily spending with long-term goals, turning policy changes into real-life benefits.

How to Create a Budget That Actually Works

Creating a budget does not have to be complicated. Follow these practical steps to build a system you can stick to in real life.

Step 1: Calculate Your Total Monthly Income

Start with the exact amount of money you receive each month after taxes. Include salary, freelance income, business earnings, or any regular side income. This is the number your entire budget will be built around.

Example: If your monthly in-hand salary is 45,000 and you earn around 5,000 from freelance work, your working budget income becomes 50,000.

Step 2: List Your Fixed Expenses

Write down expenses that stay mostly the same every month, such as rent, EMIs, subscriptions, school fees, or insurance premiums. These are non-negotiable and should be covered first.

Example: Rent 15,000, WiFi 800, phone bill 600, and an EMI of 3,500 means your fixed monthly commitments are 19,900.

Step 3: Track Your Variable Expenses

Next, look at spending that changes month to month, like groceries, transport, eating out, shopping, and entertainment. Checking past bank statements or UPI history helps you get realistic numbers.

Example: After reviewing your past two months, you notice you spend around 6,000 on groceries, 2,500 on transport, and nearly 4,000 on eating out.

Step 4: Set Clear Financial Goals

Decide what you are working toward. This could be establishing an emergency fund, saving for travel, investing, or paying off debt. Assign a monthly amount to each goal so your budget supports your future, not just your present.

Example: You may decide to save 5,000 per month for an emergency fund and 3,000 toward a vacation planned later in the year.

Step 5: Allocate Money to Each Category

Now divide your income across essentials, lifestyle expenses, and savings. Make sure your total spending does not exceed your earnings. If it does, adjust non-essential categories first.

Example: From a 50,000 income, you might allocate 20,000 for fixed costs, 15,000 for variable expenses, 8,000 for savings goals, and keep 7,000 for flexible lifestyle spending.

Step 6: Track Your Spending Regularly

A budget only works if you review it. Check your spending weekly or at least once a month to see if you are staying within limits and make changes where needed.

Example: If you notice mid-month that dining out has already crossed your set limit, you can cut back for the remaining weeks instead of overspending blindly.

Step 7: Adjust Without Guilt

Life changes, and your budget should too. Unexpected expenses or income changes are normal. The goal is not perfection but consistency and awareness.

Example: If a medical expense of 4,000 comes up, you might temporarily reduce shopping or entertainment spending that month to stay balanced.

A good budget is not strict. It is flexible, realistic, and built around your actual lifestyle.

Also read: How to Manage Monthly Expenses Smartly in 2025

Common Budgeting Mistakes and How to Avoid Them

Even a well-planned budget can fail if certain blind spots are ignored. Below are common budgeting risks and the practical ways to prevent them.

Even a well-planned budget can fail if certain blind spots are ignored. Below are common budgeting risks and the practical ways to prevent them.

1. Ignoring Small Daily Expenses

Risk: Small, frequent purchases often go unnoticed but slowly create a gap between your planned and actual spending. Over time, these untracked expenses can derail your monthly budget without you realising where the money went.

Mitigation: Track every expense, no matter how minor, using a notes app, budgeting app, or spreadsheet. Categorising even small spends helps you see patterns and make better adjustments.

2. Setting Unrealistic Spending Limits

Risk: Extremely strict budgets that remove all lifestyle spending can feel suffocating. This often leads to frustration, followed by overspending or completely abandoning the budget.

Mitigation: Build a budget that includes reasonable room for enjoyment. Balanced plans are easier to follow consistently than overly restrictive ones.

3. Forgetting Irregular or Annual Expenses

Risk: Expenses like insurance premiums, festivals, travel, or gifts do not occur every month, so they are often left out. When they appear, they disrupt your budget and may force you to dip into savings.

Mitigation: Break large occasional expenses into smaller monthly allocations so the money is ready when needed.

4. Not Prioritising Emergency Savings

Risk: Without an emergency fund, unexpected costs such as medical bills or urgent repairs can lead to debt or financial panic.

Mitigation: Treat emergency savings as a fixed monthly expense rather than something you save only if money is left over.

5. Failing to Review and Adjust the Budget

Risk: Income changes, lifestyle shifts, and new responsibilities can make an old budget inaccurate. Sticking to an outdated plan reduces its effectiveness.

Mitigation: Review your budget at least once a month and update it whenever there is a major financial change.

Budgeting Methods You Can Choose From

Not every budget works the same way for every person. The right method depends on how you think about money, how stable your income is, and how much detail you are comfortable managing.

Here are some of the most practical budgeting styles and how they differ.

1. The 50-30-20 Budget

The 50 30 20 budget divides your income into three simple portions to create a balanced financial structure. Fifty per cent of your income is reserved for essential needs such as rent, groceries, and utility bills. Thirty per cent is meant for personal wants like shopping, entertainment, and dining out. The remaining twenty per cent is directed toward savings or debt repayment.

For example, if someone earns 40,000 per month, they may spend 20,000 on needs, 12,000 on lifestyle choices, and 8,000 on savings goals.

Best for: People who want a clear and simple framework without tracking too many categories.

Why it works: It keeps financial planning easy to understand while ensuring that saving money becomes a built-in habit rather than an afterthought.

2. Zero-Based Budget

A zero-based budget gives every rupee a specific purpose before the month begins. Your income minus your planned expenses equals zero, meaning nothing is left unassigned. This includes essentials, lifestyle spending, savings, and even small personal treats.

For instance, with a monthly income of 55,000, you might plan exact amounts for rent, groceries, transport, savings, and leisure until the entire income is accounted for.

Best for: People who like detailed planning and want full visibility into where their money goes.

Why it works: It encourages thoughtful spending decisions because each expense is planned intentionally instead of happening by default.

3. Envelope Method

The envelope method divides money into separate categories, traditionally using physical envelopes or digital equivalents. Each envelope holds a fixed amount for a specific purpose, such as groceries, transport, or entertainment. Once the money in an envelope runs out, spending in that category pauses.

For example, if you assign 5,000 for dining out and finish it early in the month, you either stop eating out or adjust another category consciously.

Best for: People who tend to overspend and benefit from clear, visible limits.

Why it works: It builds spending awareness by creating a physical or visual boundary that makes financial limits easier to respect.

4. Pay Yourself First Budget

The pay yourself first method prioritises savings before any other spending. As soon as income is received, a fixed portion is transferred to savings, investments, or retirement funds. The remaining money is then used for monthly expenses and lifestyle choices.

For example, with a salary of 60,000, you might move 12,000 directly into savings and manage your monthly life with the remaining 48,000.

Best for: People who struggle to save consistently and want to focus on long-term financial growth.

Why it works: It removes the pressure of trying to save what is left at the end of the month and turns saving into an automatic habit.

5. Incremental Budgeting

Incremental budgeting builds your current plan based on previous months, making small adjustments instead of starting from scratch. You review past spending patterns and refine numbers depending on changes in income or lifestyle.

For instance, if your grocery spending has remained around 6,500 for several months, you may keep that figure steady while increasing savings after a salary raise.

Best for: People with stable income and predictable expenses who prefer a low-effort approach.

Why it works: It saves time and mental energy while still keeping your finances organised and updated.

Also read: Best Expense Tracker Apps In India For 2025

Tools and Apps That Make Budgeting Easier

Creating a budget is one thing. Sticking to it consistently is another. The right tools can simplify tracking, improve accuracy, and reduce the effort required to manage your money regularly.

| Tool Type | What It Does | Key Advantage | Limitation to Consider |

| Budgeting Spreadsheets | Manual tracking of income, expenses, and savings with full customisation | Highly flexible and detailed control over categories | Requires regular manual updates and basic spreadsheet skills |

| Budgeting Mobile Apps | Automatically tracks and categorises spending, often linked to bank accounts | Saves time with automation and real-time tracking | May have privacy concerns or limited free features |

| Expense Tracker Apps | Records daily expenses without full budgeting features | Simple way to build spending awareness | Does not provide complete financial planning |

| Banking Apps With Insights | Provides built-in spending summaries and category breakdowns | Convenient since it works within your existing bank app | Categories may be broad and less customizable |

| Pen and Paper Method | Manual written tracking of income and expenses | Encourages mindful and intentional spending | Time-consuming and harder to analyse trends over time |

Short on Cash Between Paydays? Smart Credit Can Support Your Budget

Even the most thoughtfully planned budget can be disrupted by sudden expenses like medical bills, urgent travel, or essential repairs. When savings are not enough in the moment, Pocketly offers a quick, short-term solution to help you stay financially stable without long-term disruption.

Even the most thoughtfully planned budget can be disrupted by sudden expenses like medical bills, urgent travel, or essential repairs. When savings are not enough in the moment, Pocketly offers a quick, short-term solution to help you stay financially stable without long-term disruption.

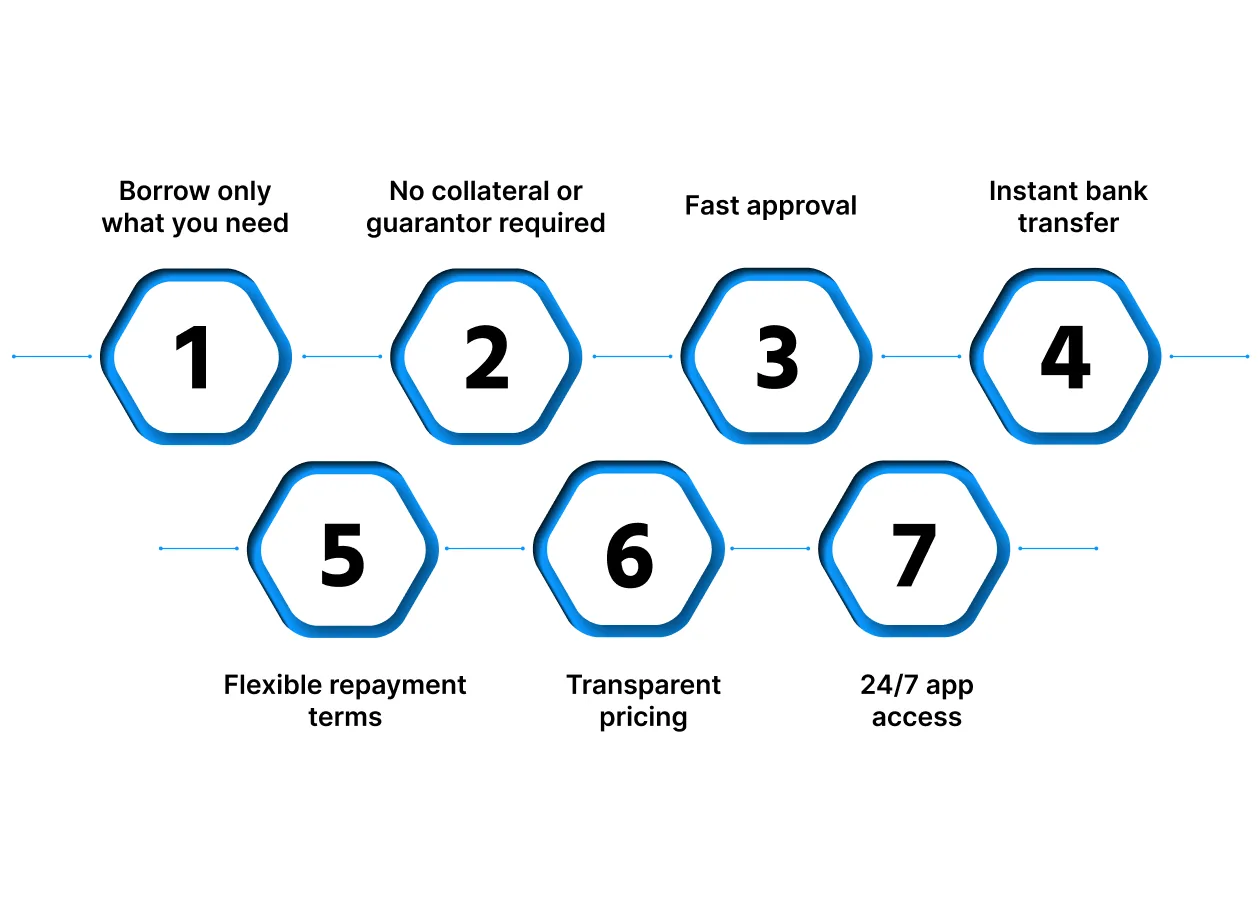

Here is why Pocketly can be a practical option:

- Borrow only what you need: Loan amounts range from ₹1,000 to ₹25,000, helping you avoid taking on more debt than necessary and keeping repayments manageable.

- No collateral or guarantor required: Pocketly offers completely collateral-free loans, making it accessible even if you don’t have assets or a co-signer.

- Fast approval with minimal documentation: A quick KYC-based verification process enables rapid decision-making without lengthy paperwork or branch visits.

- Instant bank transfer: Once approved, funds are credited directly to your bank account, making it useful for urgent expenses.

- Flexible repayment terms: Choose a repayment tenure that fits your budget, so EMIs don’t strain your monthly finances.

- Transparent pricing: Interest rates start from 2% per month, with processing fees typically between 1% and 8%, depending on your profile and loan amount, with no hidden charges.

- 24/7 app access: You can apply, track, and manage your loan anytime through the Pocketly mobile app.

Used responsibly, Pocketly can act as a financial bridge during temporary shortfalls, helping you handle urgent expenses while keeping your broader budgeting goals on track.

Conclusion

The Union Budget 2026‑27 sets the tone for India’s economic priorities, from infrastructure and skill development to incentives for SMEs and startups. While the government’s measures create opportunities, the true benefit reaches you only when you take control of your personal finances.

A practical budget is your roadmap. It turns income into purposeful spending, ensures consistent savings, and protects you from unexpected costs. By reviewing your expenses regularly, adapting to new tax rules, and allocating funds for essentials, lifestyle, and growth, you can make the most of the changes introduced in this year’s budget.

When unexpected expenses arise and stretch your budget, timely action can help you avoid long-term disruption. Short-term financial support can provide relief during urgent situations without completely derailing your plans.

Download the Pocketly app on iOS or Android to access quick funds when you need them. With flexible loan options and transparent pricing, Pocketly helps you handle sudden expenses while staying aligned with your budget.

FAQs

1. What is a budget in simple words?

A budget is a plan for how you will use your money each month. It helps you decide in advance how much to spend, save, and set aside for bills so you stay in control of your finances instead of wondering where your money went.

2. Why is budgeting important even if my income is small?

Budgeting is even more important when income is limited because it helps you prioritise essential expenses, avoid unnecessary spending, and build savings slowly. It ensures every rupee is used wisely and reduces financial stress.

3. How do I start budgeting for the first time?

Start by calculating your monthly income, listing fixed expenses like rent and bills, and estimating variable costs like groceries and travel. Then set a savings goal and adjust your spending so everything fits within your income.

4. How much of my income should I save every month?

A common guideline is to save at least 20 per cent of your income, but the right amount depends on your financial situation. Even saving a small fixed amount consistently is more effective than waiting to save what is left over.

5. What are common mistakes people make while budgeting?

Many people forget to track small daily expenses, set unrealistic spending limits, ignore irregular costs like annual fees, or stop reviewing their budget regularly. These mistakes can make a budget feel ineffective or hard to follow.