Have you ever found yourself stuck in a long, drawn-out loan approval process, waiting for days or even weeks to get the funds you need? Traditional lending systems often feel slow and outdated, leaving you frustrated and anxious when time is of the essence.

The reality is, getting access to funds quickly shouldn’t be this difficult. The old way of evaluating loans based solely on credit scores, lengthy paperwork, and manual approvals can lead to delays and missed opportunities, especially when you need cash in hand fast.

So, what if there was a faster, smarter way to get a loan?

Enter AI-powered loans. Artificial intelligence is transforming the lending industry, allowing for quick approvals, more personalised loan offers, and a simple, paperless experience. In this blog, we’ll dive into how AI is making borrowing easier, faster, and more accessible than ever before.

TL;DR

- AI lending evaluates borrowers using real financial behaviour (cash flow, transactions, gig income), not just bureau histories.

- This expands credit access for new-to-credit groups like students, gig workers, and early-career professionals.

- Lenders benefit through faster decisions, consistent scoring, and real-time portfolio visibility at scale.

- Core concerns remain around data privacy, model bias, transparency, and evolving regulatory expectations.

- For short-term cash gaps, Pocketly offers quick small-ticket loans (₹1,000–₹25,000) with fast digital onboarding and transparent pricing.

What Are AI Loans?

AI loans are credit products where artificial intelligence (AI) and machine learning (ML) are used to assess applicants and automate loan approval. Unlike traditional methods, AI-driven systems use data analysis to make faster, smarter lending decisions.

Why AI Loans Matter?

AI loans are transforming the lending landscape, offering several benefits:

AI loans are transforming the lending landscape, offering several benefits:

- Faster Loan Approval: AI speeds up the decision-making process, allowing for real-time approvals.

- Increased Accessibility: AI uses alternative data, helping those without traditional credit history qualify for loans.

- Personalised Loan Terms: AI tailors loan offers based on individual financial behaviour and risk profiles.

- Improved Risk Management: AI systems monitor loans in real-time, reducing the risk of defaults and fraud.

AI loans are reshaping the financial industry by making lending more efficient, inclusive, and data-driven.

How AI Loans Work?

AI-supported lending uses data and analytics to make quicker and more accurate credit decisions. Here’s a simple breakdown of how it functions:

1. Data Intake: Building a Financial Profile

AI lending begins with collecting financial and behavioural data to understand who the borrower is. This includes bank transactions, credit bureau history, income patterns, and digital activity. For users with thin credit files, alternate signals such as utility payments or UPI activity help fill the gaps.

How it works: The system pulls information from linked bank accounts, authorised data sources, and credit APIs. This creates a holistic financial profile that is richer than a traditional credit score alone.

2. Risk Assessment: Evaluating Repayment Capacity

Once the data is collected, machine learning models evaluate the borrower’s repayment capability. Instead of relying solely on credit scores, these models analyse spending behaviour, income stability, and past repayment patterns to estimate risk.

How it works: The AI looks for patterns that correlate with responsible repayment, such as steady income, credits and low credit utilisation. It flags signals that indicate higher risk, such as frequent overdrafts or irregular EMIs.

3. Automated Decisioning: Approvals Without the Wait

AI speeds up the loan approval process by automating underwriting steps that would normally require manual review. Applications can move from submission to decision in minutes instead of days.

How it works: The model compares the borrower’s profile with set risk thresholds and returns a result such as approve, decline, or manual review. High-confidence cases receive instant decisions, improving user experience.

4. Fraud Checks: Preventing Identity and Document Misuse

Digital lending is vulnerable to fraud attempts, so AI systems run parallel checks to validate the authenticity of users and documents. This helps lenders reduce defaults caused by fraudulent applications.

How it works: AI verifies identity data, flags mismatched information, and detects unusual patterns such as multiple applications from the same device or fake salary slips.

5. Pricing and Personalisation: Fair Terms for Every Borrower

Instead of offering the same loan terms to everyone, AI adjusts pricing based on individual risk levels. This helps responsible borrowers access better rates and higher limits, while maintaining lender safety.

How it works: The system combines risk scores with behavioural data to personalise interest rates, credit limits, and repayment periods, creating fairer outcomes than one-size-fits-all lending.

6. Post-Disbursement Monitoring: Tracking Repayment Health

After the loan is disbursed, AI continues to monitor repayment signals to predict stress early. This enables proactive engagement before borrowers fall behind.

How it works: Models track EMI behaviour, spending patterns, and income fluctuations. If early signs of strain appear, the system can trigger reminders or suggest restructuring options.

Also Read: Understanding Personal Finance and Budgeting for Financial Needs

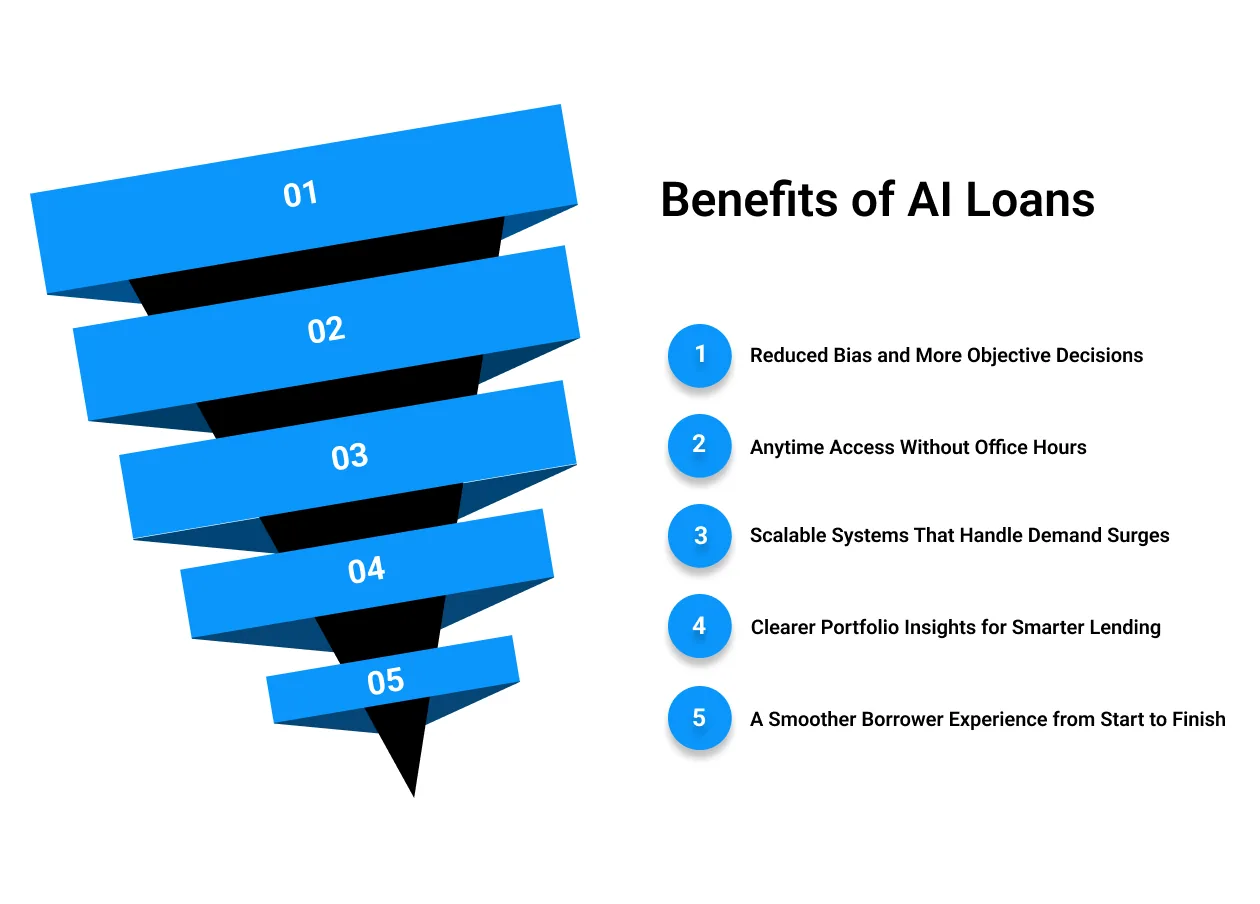

Benefits of AI Loans

AI isn’t just about automation; it reshapes lending systems in meaningful ways. Here are the benefits that go beyond speed and credit decisions:

AI isn’t just about automation; it reshapes lending systems in meaningful ways. Here are the benefits that go beyond speed and credit decisions:

1. Reduced Bias and More Objective Decisions

AI brings an analytical approach to lending that reduces the influence of human judgment. Traditional assessments often rely heavily on credit scores or visible job titles, which can exclude capable borrowers. AI models study behaviour and historical patterns instead, allowing decisions to come from data rather than assumptions.

Consider a young freelancer with irregular income but consistent repayment habits. A conventional lender may view them as risky, while an AI model can recognise strong financial discipline through transaction data and repayment history. When evaluation becomes more objective, eligible borrowers get opportunities they might have missed.

The real gain is fairness. By standardising decisions, AI gives similar profiles similar outcomes, making credit access more balanced for everyone.

2. Anytime Access Without Office Hours

AI-enabled lending platforms don’t pause for weekends, holidays or closing hours. Borrowers can apply at midnight, submit documents on the go, and receive decisions without waiting for a human review queue to reopen. This creates a level of accessibility that traditional branch-led processes can’t match.

Imagine a student dealing with an urgent academic expense late at night. Instead of waiting until the next banking day, an AI-driven system can assess their profile instantly and provide clarity on eligibility. The convenience makes financial support more responsive to real-life timing.

The advantage is control. Borrowers move at their own pace instead of adjusting to institutional schedules.

3. Scalable Systems That Handle Demand Surges

Manual underwriting teams struggle when application volumes spike, leading to delays and backlogs. AI systems don’t face that bottleneck. They can review thousands of profiles in parallel, maintaining consistent turnaround times even during seasonal peaks.

Think of a festive shopping season where demand for short-term credit skyrockets. Human teams would need overtime and temporary staffing, while AI infrastructure can scale effortlessly with traffic. Faster processing at scale benefits both the lender and the borrower.

This scalability keeps lending predictable and efficient, even when demand is volatile.

4. Clearer Portfolio Insights for Smarter Lending

AI doesn’t stop working after the loan is approved. It analyses repayment patterns, sector trends and borrower clusters to help lenders identify what’s working and what isn’t. These insights inform future lending decisions, credit policies and product design.

For example, if a model detects that a certain borrower segment consistently repays early, lenders can create tailored products for that group. On the other hand, early signs of stress in a particular industry help lenders adjust exposure before defaults escalate.

It’s not just lending; it’s learning. AI turns raw performance data into strategy.

5. A Smoother Borrower Experience from Start to Finish

Borrowers care about clarity, speed and transparency. AI supports each of these by simplifying application flows, reducing paperwork and offering predictable decisions. Instead of wondering why they were approved or declined, users get a structured journey that feels modern and supportive.

Picture a first-time borrower who struggles with traditional financial jargon. An AI-driven system can guide them with personalised prompts, offer clear next steps, and automate reminders during repayment. The experience feels less intimidating and more user-friendly.

Good experiences translate into trust. When borrowing feels seamless, people are more likely to return to the same platform or recommend it to others.

Also Read: 6 Simple Budgeting Tips for Better Money Management

AI Loans vs Traditional Loans: A Clear Side-by-Side View

The lending world is changing fast, and the biggest shift is how loans are evaluated and approved. Here’s how AI-driven lending stacks up against traditional models, written in the same easy, practical style.

| Aspect | AI Loans | Traditional Loans |

| Decision Process | Decisions use data patterns and algorithms for faster outcomes | Decisions rely on human review, paperwork, and manual checks |

| Data Considered | Looks at income patterns, digital transactions, cash flow, and behaviour | Relies mainly on credit bureau history and formal income proof |

| Speed & Convenience | Online journey with quick verification and fast outcomes | Slower processing with branch visits, paperwork, and longer wait times |

| Fairness & Consistency | Applies uniform logic to similar profiles for predictable outcomes | Outcomes vary based on human judgment and documentation differences |

| Scalability | Can handle large application volumes without extra staffing | Capacity is limited by underwriting teams and physical workflows |

The Risks You Need to Know About AI Loans

Below are the key risks associated with AI-driven lending, paired with practical mitigation logic for each.

1. Data Bias in Credit Models

AI learns from historical datasets. If that data favours certain borrower profiles, the model may unintentionally repeat those patterns. For example, if a dataset leans heavily on salaried urban applicants, gig workers, or first-time borrowers may be scored unfairly.

Mitigation logic: Improve dataset diversity, run periodic fairness tests, and introduce human review for edge cases to avoid skewed outcomes.

2. Limited Transparency Behind Decisions

Deep learning and ensemble models often produce outcomes without a simple explanation. When a user is declined, support teams may struggle to articulate why, and regulators expect clarity for consumer lending decisions.

Mitigation logic: Use explainable AI techniques, log decision variables, and design borrower feedback messages that state clear reasons rather than generic rejections.

3. Dependence on Sensitive Data

AI-driven lending typically requires access to banking transactions, income signals, spending behaviour, and identity details. This raises concerns around storage, consent, and cybersecurity.

Mitigation logic: Apply strong encryption, granular access controls, shorter data retention timelines, and transparent consent flows to protect users and meet compliance standards.

4. Evolving Regulatory Expectations

Financial regulations are catching up to AI. Requirements differ across markets and may expand around fairness, consent, model transparency, and dispute resolution. Lenders that ignore this face legal and operational exposure.

Mitigation logic: Maintain active compliance monitoring, align with policy updates, and embed regulatory checkpoints into model development and deployment.

5. Model Drift During Economic Shifts

AI models perform best when borrower behaviour matches training data. During major economic or policy shifts, user behaviour may diverge, leading to inaccurate scoring or unexpected defaults.

Mitigation logic: Conduct scenario stress tests, retrain models on recent data, and enable human override pathways when outlier conditions appear.

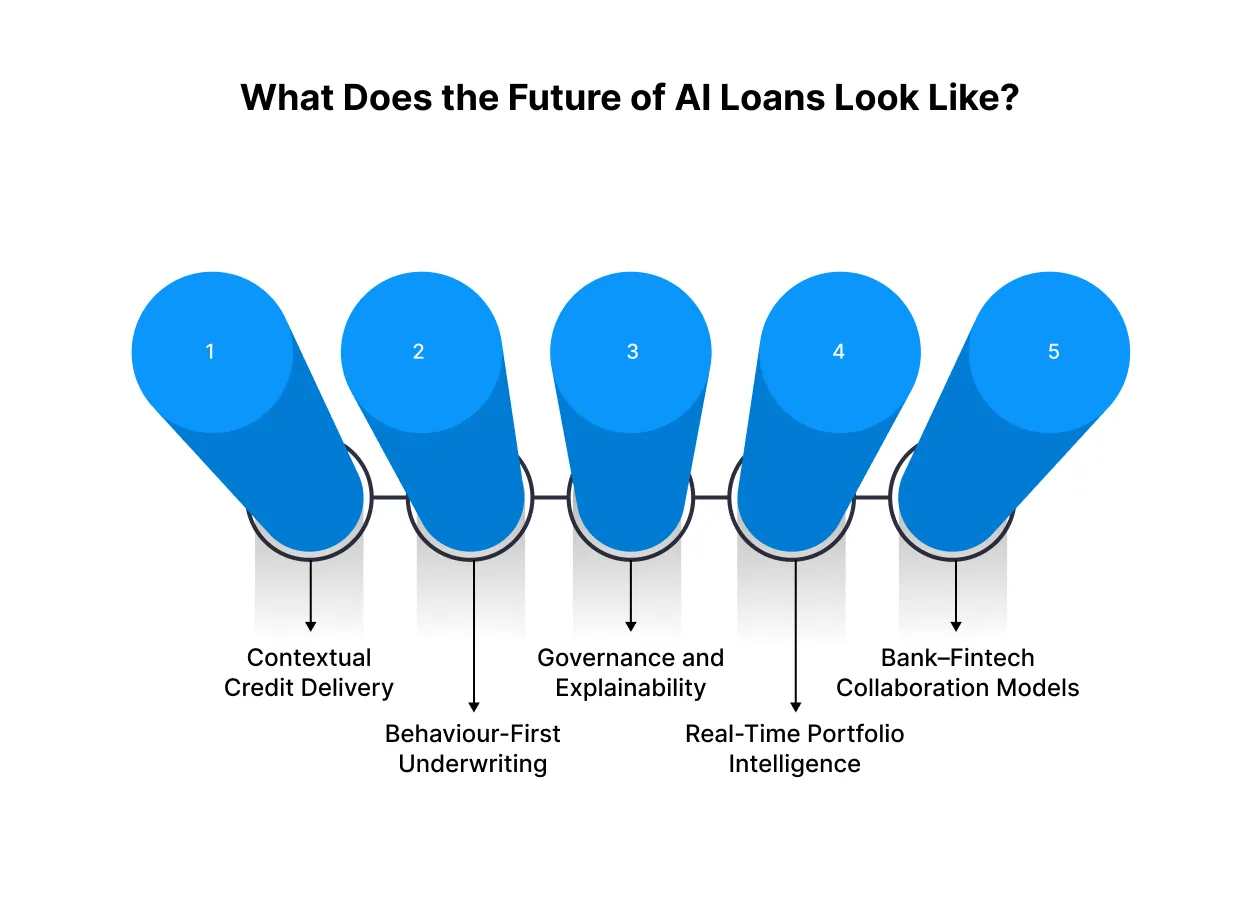

What Does the Future of AI Loans Look Like?

AI-backed lending is still early, and the next phase isn’t just about speed or automation. It’s about how lending adapts to new behaviours, new regulations, and new financial infrastructure. Here’s what that future looks like in a clear, useful format.

AI-backed lending is still early, and the next phase isn’t just about speed or automation. It’s about how lending adapts to new behaviours, new regulations, and new financial infrastructure. Here’s what that future looks like in a clear, useful format.

1. Contextual Credit Delivery

AI lending is moving closer to the point of need rather than sitting behind formal applications. Credit offers can appear inside travel bookings, gig platforms, education portals, or checkout flows based on intent and timing. By reading context, AI selects the right moment, amount, and repayment format, reducing friction for borrowers and customer acquisition costs for lenders.

2. Behaviour-First Underwriting

Future scoring models will focus less on static bureau files and more on how people manage money in real time. Cash flow stability, repayment discipline, earning cycles, and digital transaction patterns become core inputs. This approach is especially relevant for freelancers, gig workers, and young earners who rarely fit the old salaried profiles but demonstrate strong repayment behaviour through alternative signals.

3. Governance and Explainability

As AI lending scales, regulators will expect clearer answers to consumer questions like why a loan was denied or why a particular rate was offered. Explainable model architectures, audit logs, and transparent dispute workflows will become mandatory. This raises accountability for lenders while giving borrowers confidence that automated decisions are traceable and fair.

4. Real-Time Portfolio Intelligence

AI will enable lenders to shift from periodic reviews to continuous monitoring of repayment health and economic indicators. Models will scan for early stress signals such as late EMI patterns, fluctuating earnings, or sector downticks. This live visibility allows lenders to adjust line sizes, pricing, or engagement strategies long before defaults materialise, improving resilience during economic volatility.

5. Bank–Fintech Collaboration Models

The future is less about banks versus fintechs and more about what each side brings to the table. Banks hold regulatory experience, balance sheet strength, and trust. Fintechs bring speed, user-centric onboarding, and modern underwriting. Combined partnerships create safer, more innovative lending ecosystems where borrowers get faster access to credit without compromising compliance or risk standards.

Short on Cash When You Didn’t Expect It? Pocketly Can Bridge the Gap

AI lending is shaping the future, but day-to-day money stress feels very real right now. A surprise medical bill, busted phone screen, sudden travel plan, or month-end rent can throw off your balance before you even notice it.

Pocketly gives young Indians a way to handle these timing gaps with quick, small loans that fit real life instead of perfect budgets.

Why Pocketly works for everyday situations:

- Borrow what you actually need (₹1,000 to ₹25,000)

- No collateral or guarantors

- Fast digital KYC and quick approval

- Money is sent to your bank account after approval

- Repayment options that fit how you earn and spend

- Straightforward pricing: interest from 2% per month, processing fee 1% to 8%

- Available through the app anytime

Pocketly partners with regulated NBFCs to offer credit with clear terms and no hidden surprises. When an expense arrives at the wrong moment, Pocketly helps you cover it calmly and move on.

Conclusion

AI is making lending faster, clearer, and more accessible. Instead of waiting days for approvals or being judged only by credit history, borrowers are evaluated on how they actually manage money. Students, gig workers, and young professionals benefit the most because they’re finally considered beyond traditional scorecards.

The shift won’t happen overnight, but the direction is steady: lending that adapts to real life rather than rigid rules.

When an expense lands at the wrong time and disrupts your plans, address it early. Ignoring bills or pushing them to the next month only adds pressure. Short-term credit support can help you handle these timing issues without awkward borrowing or delaying essentials.

Download the Pocketly app on iOS or Android to access quick, small loans when cash flow is suddenly tight. It gives you room to breathe while you stay focused on the bigger financial picture.

FAQs

1. What are AI loans?

AI loans are credit products where artificial intelligence assists in evaluating applications, assessing risk, and making approval decisions. This often leads to faster outcomes and more consistent evaluations.

2. Are AI loans more accurate than traditional loans?

They can be, because AI considers more variables than traditional scorecard models. By analysing real financial behaviour, AI offers a more detailed picture of a borrower’s ability to repay.

3. Is AI lending safe?

AI lending is safe when lenders use strong data protection, clear consent, and regulatory-aligned practices, like any system that handles sensitive information, responsible design matters.

4. Will AI replace human underwriters?

AI is designed to support and simplify lending, not eliminate humans entirely. Complex cases, edge scenarios, and dispute handling still benefit from human judgment.

5. Can AI help people with thin credit files?

Yes. AI can analyse alternative data sources like cash flow, bank transactions, and digital payments, giving borrowers without long credit histories a fairer chance.