Investing can be a daunting concept, especially when you're just starting out. The sheer volume of options, jargon, and conflicting advice makes it feel like you need to be a financial expert just to get your foot in the door. But here's the catch: You don’t need a massive bankroll or years of experience to begin building wealth. The real issue isn’t the complexity of investing; it’s the fear of making the wrong choice and losing money.

This hesitation leads many to miss out on opportunities for long-term financial growth. Without taking the plunge, your money is simply sitting idle, unable to work for you. The good news? Getting started with investing doesn’t have to be overwhelming.

In this blog, we'll simplify the investing basics, helping you understand where to begin, what to focus on, and how to make confident decisions that will set you on the path to financial success.

TL;DR

- Investing means putting your money to work to earn returns over time, unlike saving, which is about preserving capital.

- Risk and return are key concepts; higher returns often come with higher risks, and diversifying helps manage this.

- Common investment options: Stocks, bonds, mutual funds, and real estate — each with different risk and reward potentials.

- Start with clear goals: Understand your risk tolerance and make small, consistent investments to build wealth over time.

- Focus on long-term growth, avoid emotional decisions, and ensure you regularly monitor and adjust your portfolio.

The Building Blocks of Investing: What You Should Know to Get Started

Investing doesn’t have to be complicated. At its core, it’s about making your money work for you over time. You’re not just putting money into stocks or bonds; you’re aligning it with your long-term goals and balancing the risk and reward.

Here’s what you need to know:

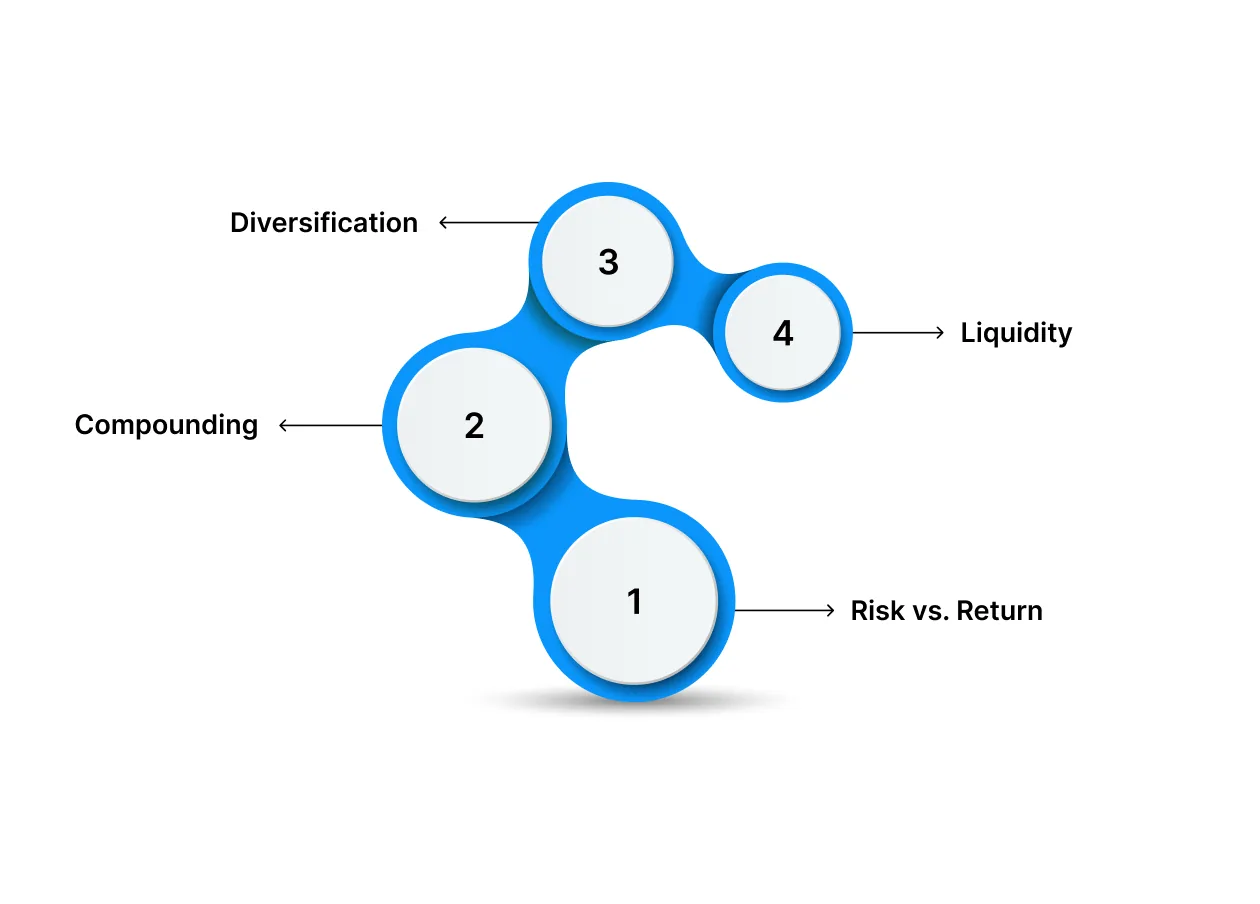

- Risk vs. Return: Higher returns often are associated with higher risk.

- Compounding: Your money earns returns on both the initial investment and the returns themselves.

- Diversification: Spread your investments to lower risk and increase stability.

- Liquidity: How quickly you can access your investment without losing value.

The more you understand these fundamentals, the easier it will be to make confident decisions that align with your financial goals. Investing is a long-term pursuit, and starting early can give you a significant advantage.

The Most Popular Investment Strategies for Those Just Starting Out

When you’re starting out, knowing where to put your money can be the biggest hurdle. The good news? You don’t need to understand every single investment type; just focus on the most accessible and well-established options.

Here’s a breakdown of the top investment types that are perfect for beginners:

1. Stocks (Equity)

Investing in stocks is a way to own a part of a company and benefit from its growth. However, this comes with some risk. The value of stocks can spike or fall, depending on company performance, market conditions, and broader economic factors. This is a long-term strategy aimed at growing your wealth over time.

Example: Buying shares in a tech startup could yield high returns if the company grows rapidly, but the stock price may also fluctuate wildly based on market trends and investor sentiment.

2. Bonds (Debt)

Bonds are a safer alternative to stocks, where you lend money to governments or corporations in exchange for interest over a specified period. They offer more stable returns but with less growth potential compared to stocks.

Example: Buying a government bond means receiving regular interest payments, but you won't see the same level of growth as you would with stocks, making it a good option for risk-averse investors.

3. Mutual Funds

A mutual fund pools money from several investors to buy a diversified portfolio of assets. It's ideal for beginners who want exposure to different investments without picking individual stocks or bonds.

Example: A mutual fund that invests in tech companies gives you a stake in several high-growth firms without the risk of putting all your money in one company.

4. Index Funds & ETFs

Index funds and ETFs track a market index, like the S&P 500. They are low-cost, low-effort ways to invest in the overall market. These options are great for long-term investors who want steady, broad market exposure.

Example: An ETF that tracks the S&P 500 gives you access to a diverse range of companies, offering automatic diversification and lower risk than investing in individual stocks.

5. Real Estate

Real estate presents the opportunity for both rental income and property appreciation. While this type of investment usually requires more upfront capital, it can provide long-term stability and passive income.

Example: Purchase of a rental property in a growing city could provide you with steady income through rent, as well as the chance for long-term value appreciation as the area develops.

6. Savings Accounts & Fixed Deposits

These are low-risk investments where you deposit your money in a bank or financial institution for a set period and earn interest. While the returns are modest, they’re secure and perfect for short-term goals or an emergency fund.

Example: A fixed deposit offers guaranteed returns, making it ideal for those who want a safe place for their money, though it won’t provide the high returns of more volatile investments like stocks.

How to Start Investing: A Simple Step-by-Step Guide

Investing is an incredible way to grow your wealth over time, but understanding where to start can be tricky. Follow these steps to make informed, confident investment decisions that align with your goals.

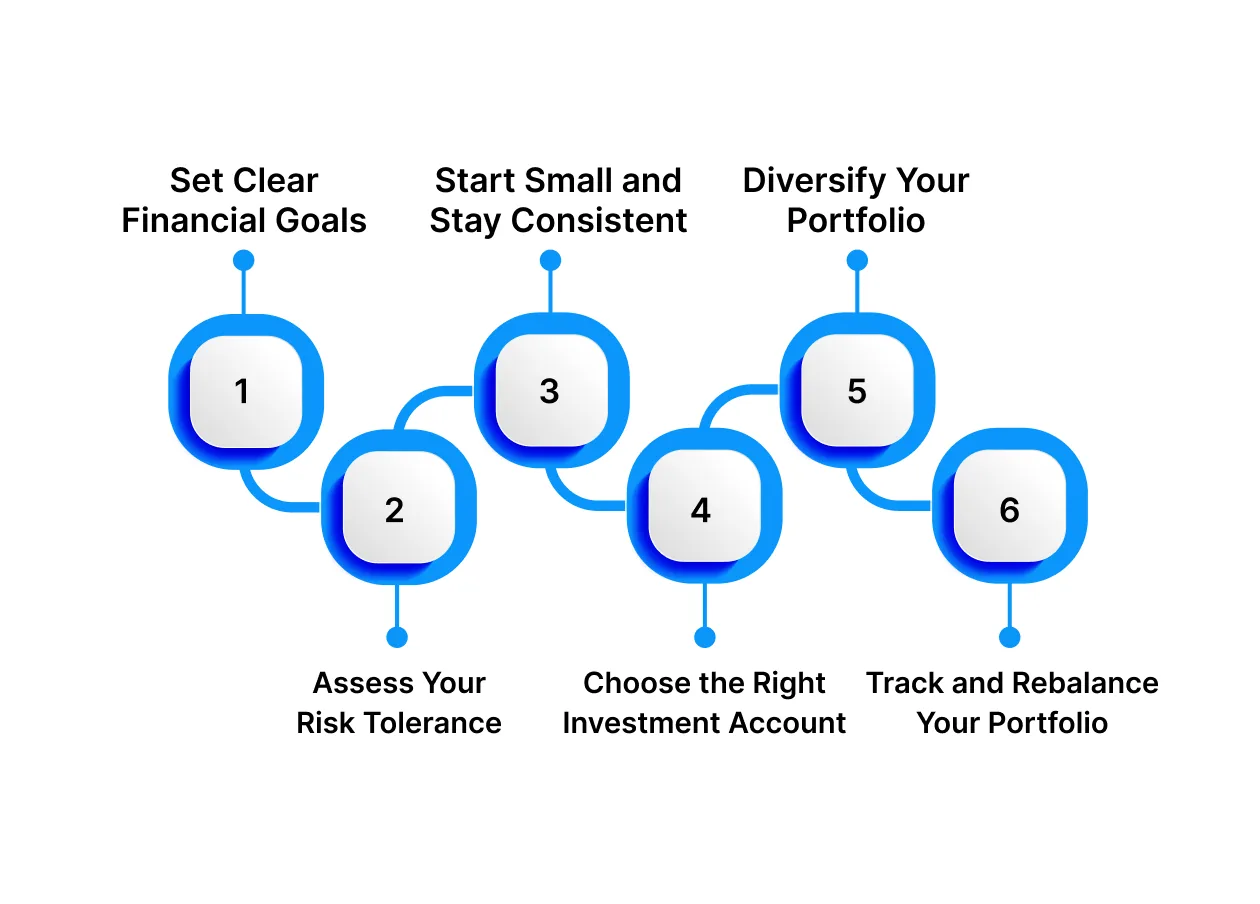

Step 1: Set Clear Financial Goals

To begin investing, identify your objectives. What are you investing in? Is it retirement, buying a house, or building an emergency fund? Setting clear targets will help you determine your time horizon, risk tolerance, and the best investment strategies for your situation.

- Short-term goals: Less than 3 years (e.g., buying a car)

- Medium-term goals: 3-10 years (e.g., buying a home)

- Long-term goals: 10+ years (e.g., retirement)

Step 2: Assess Your Risk Tolerance

Investing involves risks, and understanding how much risk you're willing to take on is crucial. Your risk tolerance relies on several factors, such as age, income stability, financial obligations, and your investment time horizon. Generally, younger investors can take on more risk, while those closer to retirement should be more conservative.

- High risk tolerance: Suitable for stocks, ETFs, and growth-focused investments.

- Low risk tolerance: Opt for bonds, savings accounts, or fixed deposits.

Step 3: Start Small and Stay Consistent

It’s important to start investing even with small amounts. Consistency is key in creating wealth over time. Consider starting with a set monthly investment amount. This approach, often called Dollar-Cost Averaging, involves buying investments at regular intervals, reducing the impact of market volatility.

- Start with affordable amounts: Even ₹1,000–₹5,000 monthly can make a big difference over time.

- Set automatic contributions: It ensures you invest consistently, even during busy months.

Step 4: Choose the Right Investment Account

Once you've set your goals and understand your risk tolerance, the next move is to open an investment account. Depending on the type of investment you’re interested in, you’ll need the appropriate account:

- Brokerage accounts: For individual stocks, ETFs, and bonds.

- Mutual fund accounts: For managed funds that invest in various assets.

- Retirement accounts (e.g., NPS, PPF): For long-term savings and tax advantages.

Ensure the account you select aligns with your investment goals and offers low fees

Step 5: Diversify Your Portfolio

Avoid putting all your cash into one investment. Diversification helps to balance risk by spreading investments across different asset classes (stocks, bonds, real estate, etc.). A well-diversified portfolio can minimise the risk of significant losses in any one area.

- Stocks: Offer higher returns but come with greater risk.

- Bonds: Provide stable returns and lower risk.

- Real estate & Mutual Funds: Provide added stability to your portfolio.

Step 6: Track and Rebalance Your Portfolio

Your investment portfolio isn’t static. Regularly monitor it to see if it’s still aligned with your goals, especially as market conditions change. Rebalancing is the process of adjusting your portfolio back to its target asset allocation if it drifts over time due to market fluctuations.

- Review quarterly or annually: Ensure you’re on track with your goals.

- Adjust as necessary: If your risk tolerance or financial situation changes, reallocate investments to stay aligned with your strategy.

By following these steps, you’ll be on your way to becoming a confident investor, building wealth and securing your financial future, one step at a time.

Also Learn: Applying for Instant ₹5000 Personal Loan Online for Urgent Needs

Smart Risk Management: Safeguarding Your Investments in 2026

Investing can be a profitable journey, but it’s important to understand the risks involved. Every investment carries some level of uncertainty, and knowing how to handle these risks can help you safeguard your capital and increase the chances of long-term success.

Below, we outline the key risks that new investors often face and practical strategies to mitigate them:

1. Market Risk (Volatility)

Market risk refers to the possibility that your investments could lose value due to changes in the overall market. This can happen as a result of economic fluctuations, political instability, or shifts in investor sentiment.

Mitigation:

- Diversification: Distribute your investments among different asset classes like stocks, bonds, real estate, and commodities. This reduces the impact of any one investment's downturn.

- Focus on Long-Term Goals: Avoid reacting to short-term market swings. Stay committed to your long-term investment plan to ride out market volatility.

2. Inflation Risk

Inflation erodes the purchasing power of money over time. If your investments do not outpace inflation, you may find that your returns are not enough to maintain your lifestyle in the future.

Mitigation:

- Invest in Growth Assets: Look for investments with the chance for higher returns, such as stocks or real estate, which historically outpace inflation.

- Inflation-Protected Securities: Consider bonds that adjust with inflation, such as Treasury Inflation-Protected Securities (TIPS), for a more stable, inflation-adjusted return.

3. Credit Risk (Default Risk)

Credit risk is the uncertainty that a bond issuer (e.g., a company or government) will default on its debt obligations, resulting in to conceivable losses for bondholders.

Mitigation:

- Research and Due Diligence: Always check the credit rating of issuers before purchasing bonds. Prefer highly-rated, low-risk bonds and avoid high-yield (junk) bonds unless you understand the risks.

- Diversify Bond Holdings: Spread your investments across different bonds and issuers to avoid the impact of any single default.

4. Liquidity Risk

Liquidity risk arises when you can’t quickly sell or convert an asset into cash without a significant loss. Assets like real estate or some bonds may be hard to liquidate in times of need.

Mitigation:

- Invest in Liquid Assets: Focus on investments like stocks, ETFs, or mutual funds that can be quickly bought and sold.

- Keep Cash Reserves: Maintain an emergency fund in liquid, low-risk assets to cover unexpected expenses without having to sell investments at a loss.

5. Emotional Risk (Behavioural Risk)

Emotional risk comes from letting fear, greed, or panic drive your investment decisions. During market downturns, it’s tempting to sell off investments at a loss, or conversely, during market highs, to chase risky, high-reward opportunities.

Mitigation:

- Create a Clear Investment Plan: Set clear goals, asset allocation, and risk tolerance. Stick to this strategy, even during market fluctuations.

- Avoid Market Timing: Rather than attempting to time the market, invest consistently and focus on long-term gains. Stay disciplined and avoid emotional reactions to market fluctuations.

6. Regulatory and Political Risk

Changes in government policies, taxation, or political instability can affect your investments. Regulatory shifts can have significant impacts on certain sectors or companies.

Mitigation:

- Stay Informed: Monitor political and regulatory news, especially if you’re invested in industries sensitive to policy changes (e.g., energy, healthcare).

- Diversify Across Regions: Spread your investments across different countries or markets to reduce exposure to any one country's political or regulatory risks.

Also Learn: Understanding the Ideal CIBIL Score Range for Personal Loan Applications

Tracking Investment Performance: Key Metrics You Need to Know

Tracking your investments is crucial for ensuring they align with your financial goals. Simply putting money into the market isn’t enough; you need to measure your portfolio’s performance regularly to see if you're on the right path.

Here’s how to evaluate your investments and make adjustments when necessary:

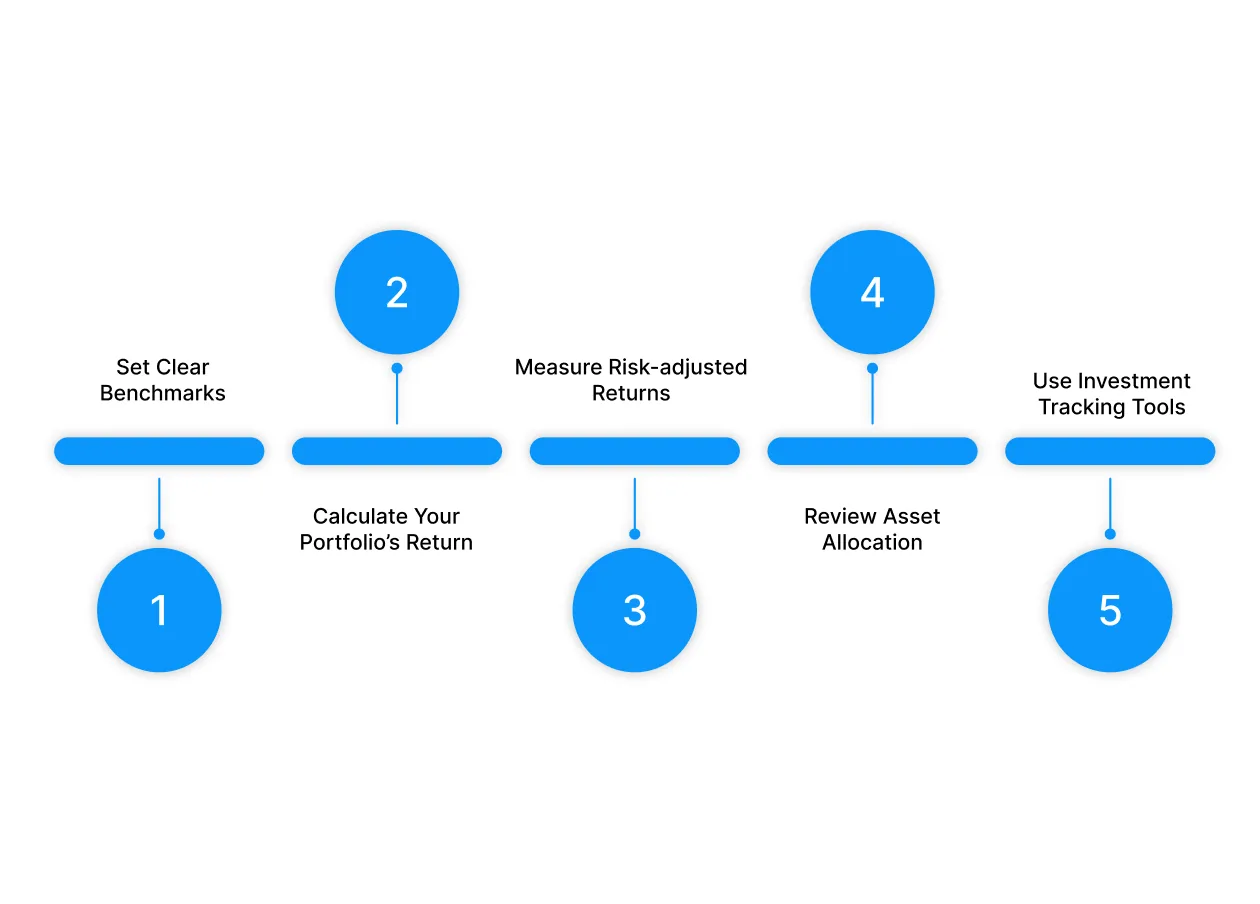

1. Set Clear Benchmarks

Before you start tracking your investments, establish clear benchmarks to measure their performance. A benchmark could be a market index (like the S&P 500 or Nifty 50) that reflects the overall market or a specific sector. Comparing your portfolio’s performance against these benchmarks helps you assess whether you’re outperforming or underperforming.

Example: If you’re investing in large-cap stocks, compare your portfolio’s performance to the Nifty 50 index.

2. Calculate Your Portfolio’s Return

To understand how well your investments are performing, calculate your portfolio return. This includes both the income (such as dividends or interest) and the capital gains (the increase in the value of your investments). A positive return means your investments are growing, while a negative return may signal that it’s time to reassess.

Formula:

Portfolio Return = (Ending Value - Beginning Value + Income) / Beginning Value

3. Measure Risk-adjusted Returns

Simply looking at the return on your investments doesn’t give you the full picture. It’s important to understand how much risk you’re taking to achieve those returns. Risk-adjusted returns are a measure that evaluates the return based on the level of risk taken.

Example: A Sharpe ratio compares the portfolio's excess return to its volatility. A higher Sharpe ratio suggests better risk-adjusted performance.

4. Review Asset Allocation

As you track your investments, regularly review your asset allocation. Over time, some investments may grow faster than others, causing your allocation to drift away from your original plan. Rebalancing your portfolio ensures it remains aligned with your goals and risk tolerance.

Example: If stocks have done well and now make up a larger percentage of your portfolio, you might sell some stocks and acquire bonds to restore balance.

5. Use Investment Tracking Tools

There are many tools and platforms available that can help you track your investments in real time. These tools can give you an overview of your portfolio’s performance, provide insights into market trends, and even alert you when it’s time to rebalance.

Example: Seek platforms that offer free tracking and analysis tools to evaluate your investment performance and risk.

When Life’s Expenses Hit Hard, Pocketly Offers Quick Financial Relief

For students and young professionals, unexpected expenses are a common challenge. Rent, textbooks, travel costs, and last-minute plans all add up quickly, often before payday. When your budget is stretched thin due to these expenses, waiting for a paycheck or external payments can leave you scrambling for cash. Borrowing from friends feels uncomfortable, and traditional loans can be slow and inconvenient.

That’s where Pocketly steps in. Designed to bridge the gap during tight financial times, Pocketly provides small, flexible loans tailored for short-term needs. Whether it's covering urgent bills, unexpected travel costs, or paying for study materials, Pocketly offers a fast, paperless solution that puts money directly into your bank account.

Key Features that Help You Manage Expenses Smoothly:

- Flexible loan amounts from ₹1,000 to ₹25,000, ensuring you only borrow what you need.

- No collateral or guarantors required for approval.

- Quick approval after basic digital checks, allowing you to access funds faster.

- Direct bank transfers ensure immediate access to your loan amount.

- Repayment schedules are aligned with your cash flow, making it easier to manage your budget.

- Transparent pricing, with interest starting from 2% per month and processing fees ranging from 1% to 8%.

Pocketly works with regulated NBFCs to ensure proper compliance and security in the loan process. Whether you're dealing with unexpected expenses or simply need a little financial breathing room, Pocketly makes it easy to cover short-term gaps without disrupting your day-to-day life.

Conclusion

Investing is more than just putting your capital into stocks or bonds; it’s about building wealth, gaining financial independence, and preparing yourself up for long-term success. By knowing the basics of investing, you can make smart decisions that help you navigate the complexities of the market, manage risk, and stay focused on your financial goals.

Keep in mind that, investing is a journey, not a sprint. Be patient and give time for your investments to grow. Start small, stay consistent, and don’t be hesitant to adjust your strategy as you learn more. The key is to make informed decisions and keep progressing.

Life happens, and sometimes unexpected expenses can throw off your plans. If you need extra financial support, don’t hesitate to explore options like Pocketly, which offers fast, short-term loans to help you bridge temporary gaps without disrupting your investment strategy. Download the Pocketly app on iOS or Android and stay on top with your financial goals.

FAQs

1. What are investing basics?

Investing basics include fundamental principles such as understanding risk, return, diversification, asset allocation, and compounding. It's about knowing how to make your money work for you over time.

2. Is investing different from saving?

Yes, saving is about preserving money with minimal risk, typically in low‑interest accounts, while investing is about growing money over time through riskier options like stocks, bonds, or mutual funds.

3. How much should a beginner invest?

As a beginner, start with a small amount you’re comfortable with. Many experts recommend investing at least 10‑15% of your income towards your long‑term goals. It's important to start small and gradually increase your investment as you learn more.

4. Can I lose money when investing?

Yes, investments come with risks, and there’s always a possibility of losing money. That’s why it’s important to diversify and have a long‑term perspective when investing.

5. Do I need a lot of money to start investing?

No, you don’t need a large amount to start investing. Many platforms let you to begin with small amounts, especially through options like mutual funds, ETFs, and fractional shares.