A 740 CIBIL score is generally considered a good credit score in India and places you near the range many lenders prefer when evaluating loan and credit card applications. While it can improve your chances of approval, lenders also look at factors such as income, existing debt, and repayment capacity before making a decision.

According to TransUnion CIBIL, the average CIBIL score of consumers actively monitoring their credit reached 728 in 2025, making a score of 740 comfortably above average.

In this guide, you'll learn what a 740 CIBIL score means, how lenders view borrowers in this range, the borrowing benefits you may qualify for, reasons applications can still be rejected, and practical steps to improve your score beyond 750.

TL;DR

-

A 740 CIBIL score is considered good and places you near the upper end of the "good" credit score range, making you a lower-risk borrower in the eyes of many lenders.

-

Loan and credit card approvals are more likely with a 740 score, but lenders also evaluate factors such as income, existing EMIs, employment stability, and recent credit enquiries.

-

A good score does not guarantee approval. High debt levels, multiple recent loan applications, repayment issues, or documentation errors can still lead to rejection.

-

Borrowers with a 740 score may access better credit opportunities, including a wider choice of lenders, easier credit card eligibility, potential pre-approved offers, and more competitive borrowing terms.

-

To move from 740 to 750+, focus on paying all bills on time, keeping credit utilisation below 30%, limiting unnecessary credit applications, checking your credit report for errors, and maintaining older credit accounts responsibly.

What Does a 740 CIBIL Score Tell Lenders?

If you have a 740 CIBIL score, lenders generally see you as a lower-risk borrower. The score reflects how responsibly you have managed credit in the past, including loan repayments, credit card usage, and overall borrowing behaviour.

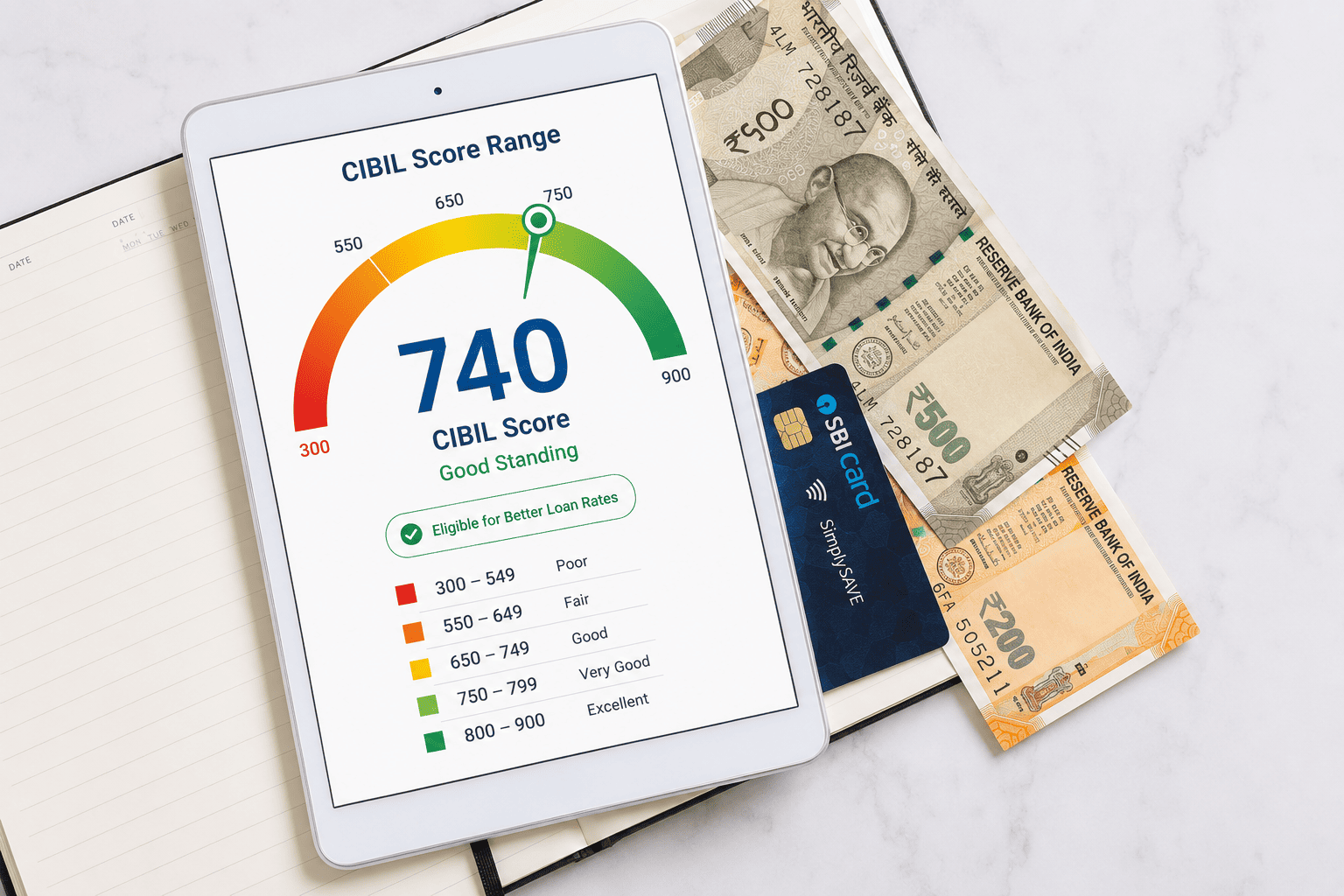

Where Does a 740 CIBIL Score Fall?

|

CIBIL Score Range |

General Interpretation |

|

300–549 |

Poor |

|

550–649 |

Fair |

|

650–749 |

Good |

|

750–900 |

Very Good to Excellent |

A score of 740 sits near the upper end of the “good” category, placing you close to the range many lenders prefer for unsecured credit products.

Is a 740 CIBIL Score Good Enough for Loan Approval?

A 740 CIBIL score is generally considered a good score and can improve your chances of qualifying for various credit products. Most lenders view borrowers in this range as relatively responsible with credit, which may make loan and credit card applications easier compared to applicants with lower scores.

Personal Loans

Many banks and NBFCs consider a this score favourably when assessing personal loan applications. However, approval is not based on credit score alone. Lenders also evaluate factors such as income, employment stability, existing loan obligations, and repayment capacity.

Credit Cards and Consumer Finance Products

With this score, you may be eligible for a wider range of credit cards and consumer finance options, including financing for electronics, appliances, or other planned purchases. Some lenders may also extend higher credit limits based on your overall financial profile.

Greater Chance of Receiving Pre-Approved Offers

Banks and financial institutions sometimes extend pre-approved loan or credit card offers to customers with strong credit profiles and a positive repayment history. While these offers are never guaranteed, a 740 score can make you a more attractive candidate for such opportunities.

Easier Credit Card Eligibility

Many entry-level and mid-tier credit cards become more accessible when you maintain a good credit score. Lenders may also be more comfortable offering higher credit limits to applicants who have demonstrated responsible credit usage over time.

|

Factor |

Borrower With 740 Score |

Borrower With Lower Score |

|

Loan approval chances |

Generally stronger |

May face additional scrutiny |

|

Lending options |

Wider selection |

Fewer available options |

|

Credit card eligibility |

Easier qualification for many cards |

More restrictions possible |

|

Pre-approved offers |

More likely to receive consideration |

Less common |

|

Risk assessment |

Viewed more favourably |

Considered higher risk |

Approval Does Not Always Mean the Best Terms

While this score can support approval, the most competitive interest rates and premium credit products are often reserved for borrowers with scores above 750 or 800. In other words, a good score can help you access credit, but a higher score may unlock more favourable borrowing terms.

This raises an important question: if 740 is a strong score, why do some applicants still face rejection? The next section explores the factors beyond credit score that lenders consider.

Why Some Borrowers With a 740 Score Still Face Rejection

A 740 CIBIL score is generally a positive sign, but it does not guarantee loan approval. Lenders use credit scores as one part of a broader assessment. If other aspects of your financial profile raise concerns, an application may still be declined despite having a good score.

High Existing Debt Can Reduce Approval Chances

Lenders look at how much of your income is already committed to existing EMIs and credit card payments. If a large portion of your monthly income goes towards debt repayment, taking on additional borrowing may appear risky.

Multiple Recent Credit Applications

Submitting several loan or credit card applications within a short period may signal financial stress. Each lender enquiry becomes part of your credit history, and frequent applications can make lenders cautious about extending new credit.

Income Stability

A strong credit score reflects past borrowing behaviour, but lenders also need confidence in your ability to repay future obligations. Frequent job changes, irregular income, recent unemployment, or inconsistent business earnings can affect eligibility, particularly for unsecured loans.

Documentation Problems Can Delay or Derail Approval

Simple issues such as mismatched KYC details, outdated address information, missing income documents, or incorrect application details can result in rejection. Lenders need accurate documentation to verify identity, income, and repayment capacity.

Employer or Business Risk Profiles Influence Decisions

Some lenders consider the applicant's employer, industry, or business segment during underwriting. For salaried professionals, employment with a stable organisation may strengthen an application. For self-employed individuals, lenders may review business vintage, cash flow consistency, and industry risk before making a decision.

Signs of Repayment Stress Raise Red Flags

Even with a good score, recent missed payments, heavy credit card utilisation, loan restructurings, or overdue balances can indicate financial pressure. Lenders often examine recent account activity rather than relying solely on the headline score.

Quick checklist before applying:

-

Keep existing EMIs manageable relative to income

-

Avoid applying to multiple lenders simultaneously

-

Ensure all KYC and income documents are current

-

Maintain timely repayments across all credit accounts

-

Reduce outstanding credit card balances where possible

The next step is to explore the specific advantages a 740 CIBIL score can provide when applying for loans and other credit products.

How to Improve a 740 CIBIL Score to 750 and Beyond

Moving into the 750+ range can further strengthen your credit profile and may improve access to premium credit cards, competitive loan terms, and a wider choice of lenders. The good news is that reaching this level often requires consistent financial habits rather than major changes.

Never Miss a Payment Due Date

Payment history is one of the most important factors influencing your credit score. Even a single missed EMI or credit card payment can affect your score and remain visible on your credit report.

To stay on track:

-

Set up automatic payments where possible

-

Use payment reminders for due dates

-

Pay at least the minimum amount due if facing temporary cash-flow constraints

-

Monitor all active credit accounts regularly

Keep Credit Utilisation Under Control

Credit utilisation refers to the percentage of your available credit limit that you use. Consistently using a large portion of your credit limit can signal higher dependence on credit, even if payments are made on time.

A practical approach is to:

-

Keep utilisation below 30% whenever possible

-

Spread spending across multiple cards if available

-

Pay outstanding balances before the billing cycle closes

Also read: How to Calculate and Improve Credit Utilisation Ratio

Avoid Applying for Multiple Credit Products at Once

Every formal loan or credit card application generates a hard enquiry on your credit report. A few enquiries are normal, but several applications within a short period may make lenders question your financial stability.

Before applying:

-

Compare options carefully

-

Apply only when there is a genuine need

-

Avoid submitting applications to multiple lenders simultaneously

Review Your Credit Report for Errors

Mistakes in credit reports can occasionally affect your score. Incorrect payment records, duplicate accounts, or outdated information may create unnecessary obstacles when applying for credit.

Check your report periodically for:

-

Incorrect personal information

-

Unrecognised loan or credit accounts

-

Incorrect overdue balances

-

Reporting errors from lenders

If you identify an issue, raise a dispute with the credit bureau and the reporting lender for correction.

Maintain Older Credit Accounts Responsibly

A longer credit history helps lenders understand your borrowing behaviour over time. Closing your oldest credit card or account without a good reason may reduce the average age of your credit history.

Instead:

-

Keep older accounts active if they remain useful

-

Continue using them responsibly

-

Make timely repayments consistently

A Simple 90-Day Credit Improvement Checklist

If your goal is to move from 740 to 750+, focus on these habits over the next few months:

-

Pay every EMI and credit card bill on time

-

Keep credit utilisation below 30%

-

Avoid unnecessary loan and card applications

-

Check your credit report for errors

-

Maintain older credit accounts in good standing

Also read: How to Achieve a Perfect 900 CIBIL Score?

Common Myths About a 740 CIBIL Score

Understanding the myths can help you make better financial decisions and avoid unnecessary disappointment.

Myth 1: A 740 CIBIL Score Guarantees Loan Approval

Reality: A good credit score improves your chances of approval, but it is not a guarantee.

Lenders assess multiple factors before approving an application, including:

-

Monthly income

-

Employment stability

-

Existing loan obligations

-

Credit utilisation

-

Recent credit enquiries

Even with a score of 740, an applicant with high debt or inconsistent income may still face rejection.

Myth 2: Checking Your Own CIBIL Score Lowers It

Reality: Reviewing your own credit score does not affect it.

When you access your own credit report, it creates a soft enquiry, which has no impact on your score. Only lender-initiated credit checks associated with loan or credit card applications are recorded as hard enquiries.

Regularly checking your score can actually help you spot errors and monitor your financial progress.

Myth 3: Credit Score Is the Only Thing Lenders Care About

Reality: A credit score is only one part of the evaluation process.

As mentioned above, lenders want to understand whether you can comfortably repay future borrowing. Along with your score, they may examine:

-

Income and salary credits

-

Employment or business stability

-

Existing EMIs

-

Bank account activity

-

Debt-to-income ratio

A borrower with a slightly lower score but strong income stability may sometimes be viewed more favourably than someone with a higher score and significant financial commitments.

Myth 4: Income Does Not Matter if Your Score Is Good

Reality: Income remains a critical factor in lending decisions.

A 740 score indicates responsible credit behaviour, but lenders also need evidence that you can manage future repayments. This is why loan eligibility often depends on both creditworthiness and repayment capacity.

For example, two applicants with identical scores may receive different outcomes if one has a stable monthly income and the other has irregular earnings.

Myth 5: First-Time Borrowers Are Automatically Rejected

Reality: Having little or no credit history does not automatically disqualify you from accessing credit.

While lenders may have less information to assess risk, many also consider factors such as income, education, employment status, banking behaviour, and overall eligibility criteria. Building a positive repayment record over time is often more important than simply having a long credit history.

Need Help Covering an Essential Expense While Maintaining Healthy Credit Habits?

A good credit score can improve access to borrowing options, but unexpected expenses can still put pressure on your monthly budget. A medical bill, insurance premium, exam fee, urgent repair, rent shortfall, or a temporary business cash-flow gap can affect your sanity.

Avoid situations that require a relatively small amount of funding. Pocketly is a digital lending platform working with RBI-registered NBFCs that helps eligible users access short-term credit through a fully digital process.

About Pocketly

-

Loan amounts ranging from ₹1,000 to ₹25,000

-

Interest starting from 2% per month

-

Processing fee between 1% and 8%

-

No collateral required

-

Fast digital application process

-

Quick digital KYC verification

-

Eligibility and visible loan limits may vary by profile

How the Process Works

Getting started is designed to be simple:

-

Download the app or visit the website

-

Complete the digital KYC process

-

Select your preferred loan amount

-

Receive approval and funds if eligible

Before borrowing, consider whether the repayment comfortably fits within your budget and existing financial commitments. Responsible borrowing and timely repayments can help protect the positive credit history you've worked to build.

If you're facing a temporary cash shortfall for an essential expense, explore whether a small-ticket loan matches your needs and repayment capacity before committing.

Final Thoughts

A 740 CIBIL score can improve your chances of getting loans and credit cards, but lenders also consider factors like income, existing EMIs, and repayment history before approving applications. Building healthy credit habits such as paying bills on time and keeping credit utilisation low can help strengthen your score further over time.

If you're facing a short-term cash crunch for an essential expense, Pocketly offers a simple digital borrowing experience for eligible users. Download the Pocketly app to explore loan options and manage urgent financial needs responsibly.

Frequently Asked Questions

1. Is a 740 CIBIL score considered good in India?

Yes, a 740 CIBIL score is generally considered a good credit score in India. It indicates a history of responsible credit behaviour and timely repayments. Many lenders view borrowers with scores in this range favourably when evaluating loan and credit card applications.

2. Can I get a personal loan with a 740 CIBIL score?

In many cases, yes. A 740 score can improve your chances of qualifying for a personal loan. However, approval depends on more than your credit score alone. Lenders may also assess your income, employment stability, existing debt obligations, repayment capacity, and documentation before making a decision.

3. Can I get a credit card with a 740 score?

A 740 CIBIL score is often sufficient to qualify for many entry-level and mid-tier credit cards. Depending on the lender and your overall financial profile, you may also be eligible for cards with additional rewards, benefits, or higher credit limits.

4. How long does it take to improve a 740 score to 750?

There is no fixed timeline because credit scores are influenced by individual financial behaviour. Consistently paying bills on time, keeping credit utilisation low, avoiding unnecessary credit applications, and maintaining a healthy credit history can help improve your score over time. Some borrowers may see improvements within a few months, while others may take longer depending on their credit profile.

5. Does checking my own CIBIL score reduce it?

No. Checking your own credit score creates a soft enquiry, which does not affect your CIBIL score. Regularly reviewing your credit report can help you track progress, identify reporting errors, and monitor your overall credit health.

6. Why was my loan application rejected despite having a 740 score?

A good credit score does not guarantee approval. Lenders also consider factors such as income level, employment or business stability, existing EMIs, debt-to-income ratio, recent credit enquiries, and document verification. An application may be declined if one or more of these areas does not meet the lender's eligibility criteria.