You work hard and earn steadily, and yet by the end of the month, it feels like your money has vanished. Small impulse buys, surprise bills, and everyday expenses quietly chip away at your income, leaving little room for savings or big goals.

This lack of control can quickly turn stress into a constant companion. Financial uncertainty makes even simple decisions, like going out for coffee or buying a gift, feel stressful instead of enjoyable.

Spending management is the solution. By tracking your expenses, setting clear limits, and prioritising what truly matters, you can take charge of your money instead of letting it slip through your fingers.

In this blog, you’ll discover practical strategies, tools, and tips to manage spending effectively, stay on top of your budget, and create room for both security and lifestyle freedom.

Key Takeaways

- Spending management is about taking control of your expenses so every rupee works toward your financial goals instead of slipping away unnoticed.

- Tracking your spending and categorising expenses helps you identify unnecessary habits, avoid overspending, and make smarter decisions.

- Creating simple systems, like tracking daily purchases or setting spending limits for each category, makes managing money easier and more effective.

- Setting aside emergency funds and using short-term solutions like Pocketly can help cover unexpected costs without disrupting your financial plan.

- Consistent monitoring, regular reviews, and mindful adjustments ensure your spending aligns with your priorities, reduces stress, and builds long-term financial stability.

What Is Spending Management?

Spending management is more than just tracking every rupee you spend; it’s about intentionally controlling where your money goes so that your financial decisions align with your goals. Unlike random spending, where money disappears and regret follows, spending management gives you clarity and control.

Spending management is more than just tracking every rupee you spend; it’s about intentionally controlling where your money goes so that your financial decisions align with your goals. Unlike random spending, where money disappears and regret follows, spending management gives you clarity and control.

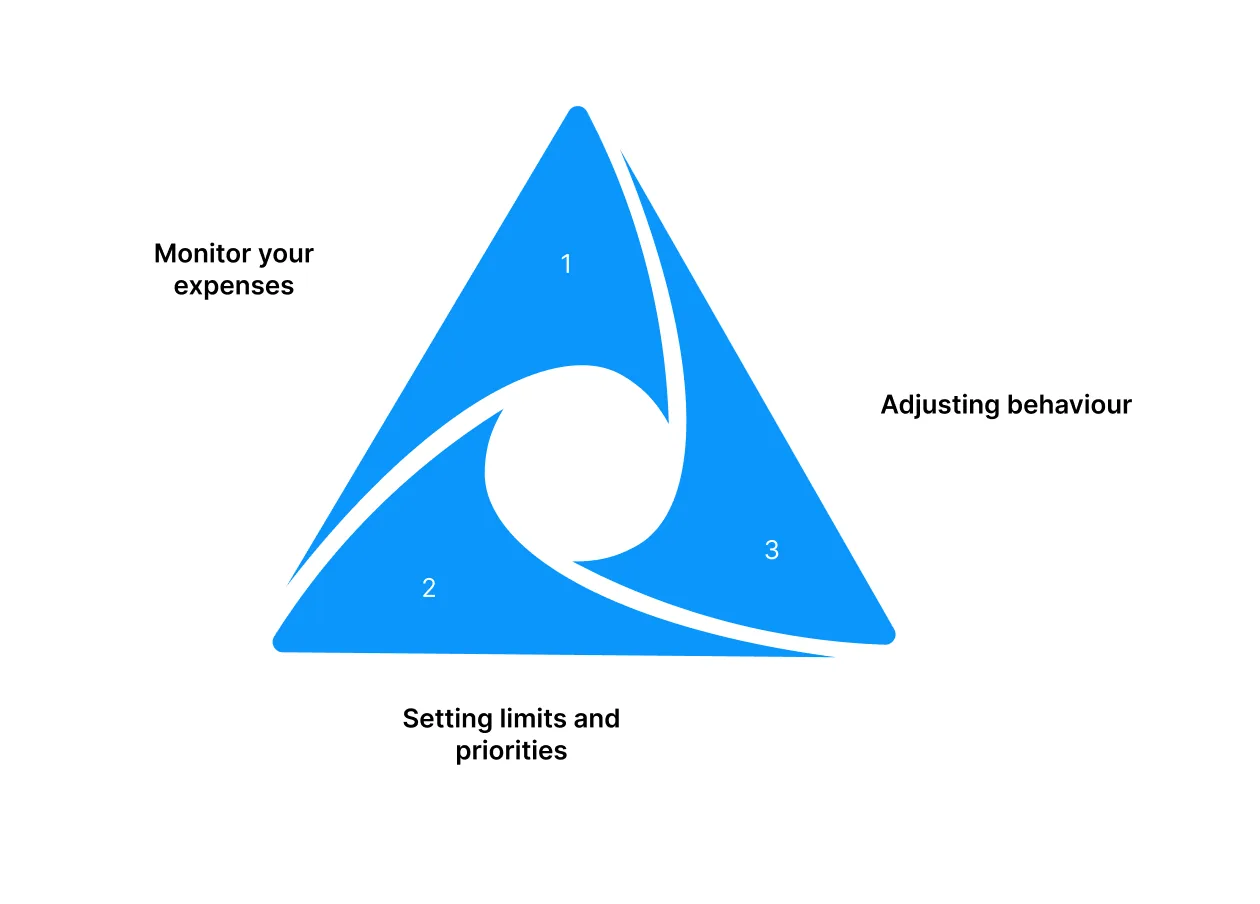

At its core, it involves:

- Monitor your expenses across categories like bills, groceries, lifestyle, and savings.

- Setting limits and priorities so you avoid unnecessary purchases.

- Adjusting behaviour when spending exceeds what’s planned to keep your budget on track.

For example, a young professional in Mumbai might notice that frequent food delivery orders are eating into their savings. By actively managing spending, they can set a monthly limit for dining out while still saving for a vacation.

Why Spending Management Matters?

Effective spending management doesn’t just keep your bank balance healthy; it impacts your financial confidence, decision-making, and long-term goals. Here’s why it matters:

- Better Control Over Your Money: You stop wondering where your income went. Tracking and managing expenses prevents overspending and promotes intentional financial choices.

- Consistent Savings Growth: Setting limits and planning spending ensures savings happen regularly, helping you build an emergency fund, invest, and reach your financial goals faster.

- Reduced Financial Stress: When you know your essential bills and savings are covered, unexpected expenses feel manageable, not overwhelming.

- Smarter Financial Decisions: Clear visibility into income and expenses makes it easier to decide on lifestyle choices, purchases, or investments without guilt or confusion.

- Progress Toward Long-Term Goals: Connecting daily spending to bigger ambitions, like buying a home, travelling, or education, makes your goals achievable instead of distant dreams.

- Healthy Relationship With Money: Spending management shifts your mindset from reacting to money to controlling it, reducing impulsive behaviour and fostering financial confidence.

Steps to Manage Your Spending Effectively

Taking control of your spending doesn’t mean cutting out everything you enjoy. It’s about understanding where your money goes, making intentional choices, and synchronising your spending with your goals. Here’s how to approach it systematically:

Taking control of your spending doesn’t mean cutting out everything you enjoy. It’s about understanding where your money goes, making intentional choices, and synchronising your spending with your goals. Here’s how to approach it systematically:

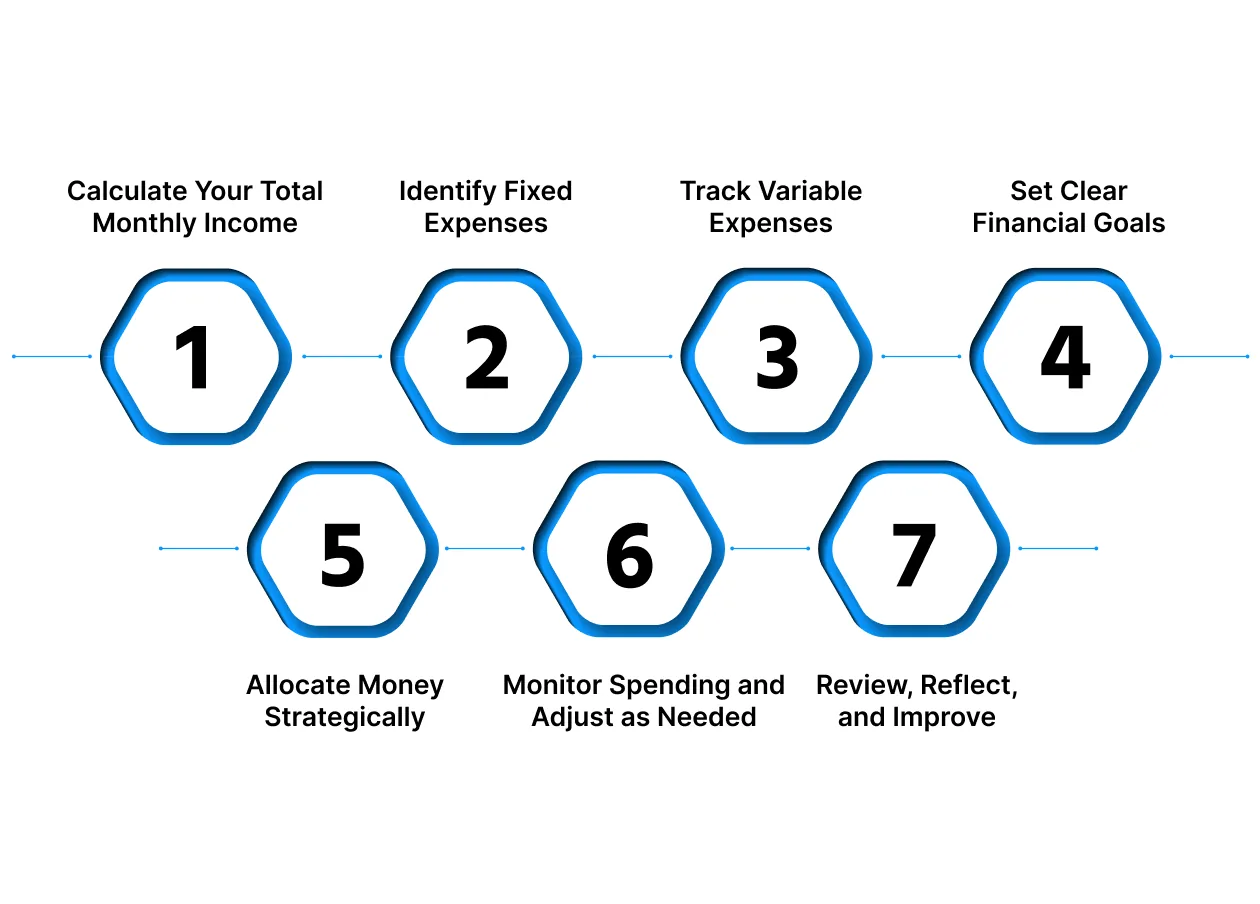

1. Calculate Your Total Monthly Income

Know exactly how much money you have at your disposal. Include salary, freelance work, bonuses, and any side hustles. Understanding your total income allows you to make realistic spending plans rather than guessing or overspending.

Example: Salary ₹50,000 + freelance earnings ₹5,000 → Total income ₹55,000. This number becomes the base for all spending decisions.

2. Identify Fixed Expenses

These are non-negotiable costs that keep your life running smoothly. Covering them first ensures essentials like rent, EMIs, and insurance are protected, preventing stress or late fees.

Example: Rent ₹15,000, EMI ₹4,000, insurance ₹1,000 → Fixed expenses ₹20,000. Knowing this helps you understand how much is left for discretionary spending.

3. Track Variable Expenses

Variable spending includes groceries, transport, dining, and entertainment. Tracking these helps you identify patterns, spot leaks, and make informed adjustments. Use bank statements, UPI history, or expense tracking apps to get accurate numbers.

Example: Groceries ₹6,000, transport ₹3,000, dining out ₹4,000 → Variable expenses ₹13,000. Real data prevents guesswork and impulsive choices.

4. Set Clear Financial Goals

Spending without purpose leads to wasted opportunities. Define short-term and long-term goals, emergency savings, vacations, investments, or debt repayment, and assign funds accordingly. This turns budgeting into a roadmap for your financial future.

Example: Emergency fund ₹5,000, travel savings ₹3,000 → Total savings ₹8,000. Knowing why you’re saving motivates consistency.

5. Allocate Money Strategically Across Categories

Divide your income among essentials, lifestyle spending, and savings. Prioritise necessities first, then goals, and finally flexible spending. This ensures you don’t overshoot your income while still enjoying life responsibly.

Example: Income ₹55,000 → Essentials ₹20,000, Lifestyle ₹15,000, Savings ₹8,000, Flexible ₹12,000. Allocation shows where adjustments can be made without stress.

6. Monitor Spending and Adjust as Needed

A budget is not static. Regularly check your progress weekly or monthly. Overspending in one category can be balanced by reducing another. Tracking fosters awareness and prevents surprises at month-end.

Example: Dining out has already reached ₹4,500 mid-month → Reduce future meals or entertainment spending to stay on track.

7. Review, Reflect, and Improve

End-of-month reviews reveal spending habits, highlight opportunities for savings, and help you refine your plan. Over time, this creates financial awareness, better decision-making, and confidence in handling money.

Example: Notice recurring impulse purchases → Adjust next month’s discretionary budget or set stricter limits.

Effectively managing spending is less about restriction and more about intentionality. When each rupee is tracked, allocated, and aligned with your priorities, your money works for you, not the other way around.

Also Read: Understanding How Positive Cash Flow Works and Why It's Important

Common Spending Mistakes and How to Avoid Them

Even the most well-intentioned budgeting plans can fail if common pitfalls aren’t addressed. Recognising these mistakes early helps you avoid unnecessary stress, overspending, or wasted effort. Here’s what to watch out for and how to fix it:

1. Ignoring Small Daily Expenses

Risk: Frequent small purchases like coffee, snacks, or app subscriptions can quietly add up, creating gaps between planned and actual spending.

Mitigation: Track every expense, no matter how minor. Use a budgeting app, digital notes, or a simple spreadsheet. Categorise even small spends to spot patterns and curb unnecessary spending.

2. Setting Unrealistic Spending Limits

Risk: Extremely strict budgets that eliminate all leisure or lifestyle spending often lead to frustration and eventual overspending.

Mitigation: Include reasonable allowances for entertainment, dining out, or hobbies. Balanced budgets are easier to maintain consistently.

3. Forgetting Irregular or Annual Expenses

Risk: Costs like insurance premiums, festival shopping, or annual subscriptions don’t appear monthly, so they’re often overlooked, disrupting your budget when due.

Mitigation: Break these expenses into smaller monthly allocations. Setting aside ₹500/month for an annual subscription prevents surprises.

4. Neglecting Emergency Savings

Risk: Without an emergency fund, unexpected events like medical bills or urgent repairs can lead to debt or financial panic.

Mitigation: Treat emergency savings as a non-negotiable monthly expense. Even ₹2,000–₹5,000/month builds a safety net over time.

5. Failing to Review and Adjust the Budget

Risk: Life changes, salary increases, moving cities, and new responsibilities can make an old budget ineffective. Sticking to it blindly reduces its usefulness.

Mitigation: Review your budget at least once a month. Adjust allocations to reflect income changes, new expenses, or shifting goals.

By addressing these common mistakes, you transform budgeting from a stressful task into a powerful tool for control, clarity, and smarter financial choices.

Also read: Understanding Cash Flow: Definition, Types, and Analysis

Extra Tips for Smarter Spending Management

Even with a solid spending management system, small habits and tweaks can make a big difference in how effectively you control your money. Here are some practical tips to level up your spending management:

Even with a solid spending management system, small habits and tweaks can make a big difference in how effectively you control your money. Here are some practical tips to level up your spending management:

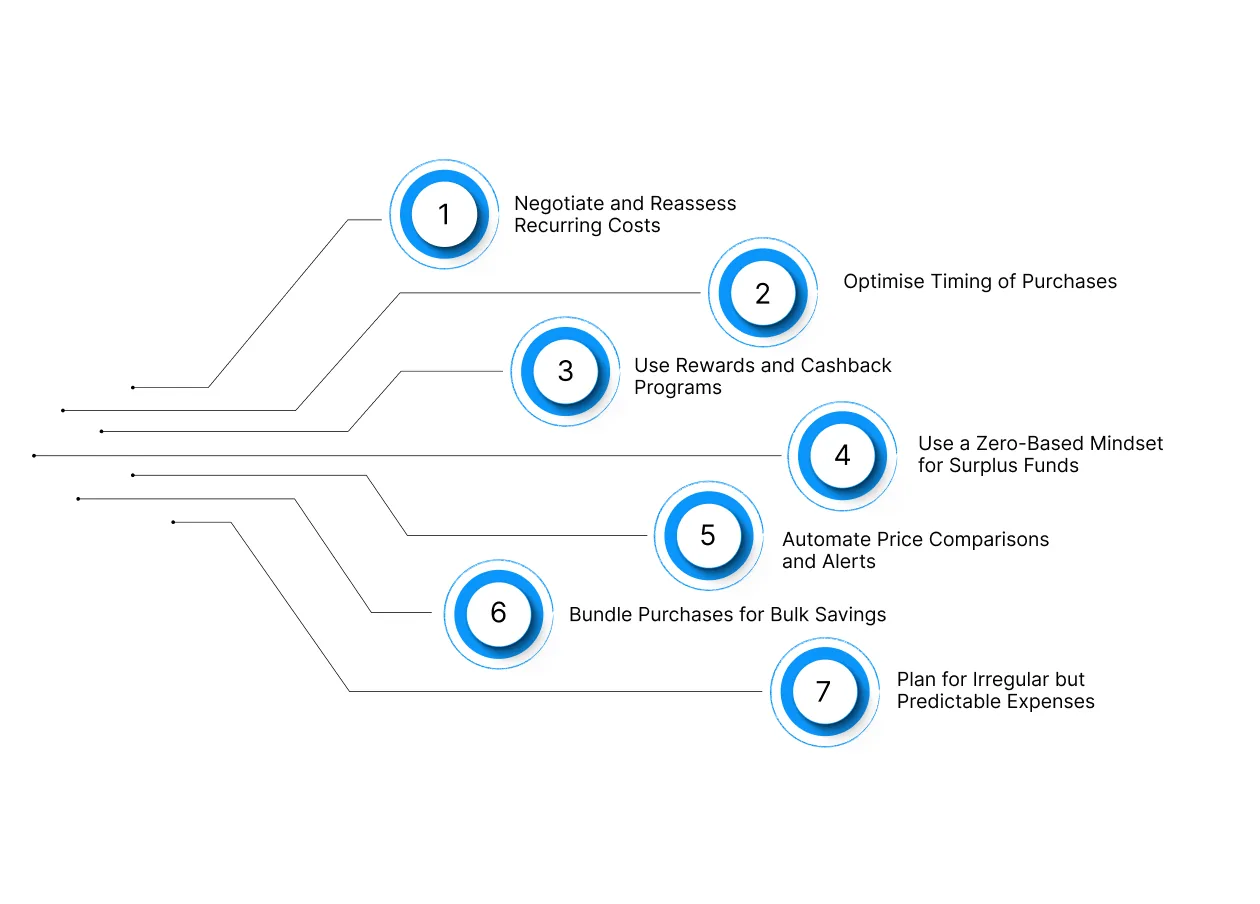

1. Negotiate and Reassess Recurring Costs

Many recurring bills quietly eat into your monthly budget. Regularly reviewing and negotiating these expenses can free up significant cash flow. Check service providers for promotions, discounts, or better plans, and don’t hesitate to switch if it saves money without affecting your quality of life.

For example, you may discover your internet provider offers a lower-cost plan with the same speed, or you may be paying for subscriptions you rarely use. By adjusting or cancelling, you could save ₹1,000–₹2,000 per month effortlessly.

2. Optimise Timing of Purchases

When you buy, it can be just as important as what you buy. Strategic timing allows you to take advantage of sales, seasonal discounts, or bulk deals, helping you stretch every rupee further.

For instance, purchasing winter clothing in February during end-of-season sales, or stocking up on non-perishable groceries when there’s a bulk-buy offer, reduces the need for impulse spending at higher prices later. Over a year, this adds up to substantial savings without limiting your lifestyle.

3. Use Rewards and Cashback Programs

Spending strategically can actually make your money work for you. Credit cards, mobile wallets, and loyalty programs often provide rewards or cashback for regular spending. By aligning everyday expenses with these programs, you can reduce costs or earn bonuses.

For example, grocery shopping via a cashback-linked card could earn ₹500 per month, which you can either save or reinvest into another financial goal. Over a year, this small strategy can translate into thousands of rupees, essentially lowering the real cost of essentials.

4. Use a Zero-Based Mindset for Surplus Funds

Leftover money often gets spent unconsciously. Assigning every extra rupee a purpose ensures that no funds sit idle or get wasted. Decide in advance whether surplus money should go toward savings, debt repayment, or investments.

For example, if you have ₹3,000 extra at the end of the month, you could split it: ₹1,500 toward high-interest debt, ₹1,000 toward an emergency fund, and ₹500 for a small treat. This method keeps your finances intentional and reduces the stress of “unexpected” spending.

5. Automate Price Comparisons and Alerts

Manual checking of prices wastes time and often misses opportunities. Using price comparison tools, browser extensions, or apps that alert you to discounts ensures you never overpay for recurring or planned purchases.

For instance, a price tracker may notify you when a regular grocery brand drops by 10%, letting you stock up without changing your preferred products. Over several purchases, these automated alerts can save hundreds or thousands each year without extra effort.

6. Bundle Purchases for Bulk Savings

Buying items in bulk can reduce unit costs significantly, especially for groceries, toiletries, or household essentials. Proper planning is necessary to avoid overstocking items that expire quickly or create clutter.

For instance, purchasing a six-month supply of rice or cleaning products during a discount period can save 15 to 20 per cent compared to buying monthly. Smart bundling optimises cash flow and prevents last-minute high-cost purchases.

7. Plan for Irregular but Predictable Expenses

Expenses that do not occur monthly, like insurance premiums, festivals, birthdays, or annual travel, are often forgotten. Not accounting for them can disrupt your budget unexpectedly.

Create a separate allocation each month to cover these predictable costs. For instance, if annual insurance is ₹12,000, set aside ₹1,000 monthly so the payment does not create financial strain when it is due. This proactive approach prevents surprises from derailing your spending plan.

Pocketly: Your Ally for Managing Unexpected Expenses

No matter how carefully you plan your spending, life can throw surprises like sudden medical bills, urgent school fees, or emergency home repairs that can disrupt your budget and cause stress. Having a reliable backup can make all the difference.

Pocketly acts as that financial safety net for young Indians. This fully digital lending platform helps you bridge short-term cash gaps quickly and transparently, without the long waits or paperwork of traditional banks. Whether you’re a student, a young professional, or building a side hustle, Pocketly provides funds exactly when you need them.

- Fast and flexible loans: Borrow between ₹1,000 and ₹25,000, ensuring you take only what’s necessary to cover your immediate needs.

- Transparent and affordable terms: Interest rates start at 2% per month, with processing fees ranging from 1% to 8%. There are no hidden charges, making repayment predictable and stress-free.

- Fully digital process: Apply from your phone, complete KYC online, and get approval quickly, no paperwork, no queues.

- Repayment options designed for you: Choose EMIs or full repayment at your convenience. Pocketly adapts to your financial capacity, keeping repayments manageable.

How to Get Started

1. Download the App: Available on iOS and Android.

2. Complete KYC: Simple, paperless verification with basic documents.

3. Select Loan Amount: Borrow up to ₹25,000 based on your requirement.

4. Receive Funds Instantly: Money is credited directly to your bank account once approved.

With Pocketly, short-term financial surprises don’t have to derail your budget. Quick, transparent, and flexible, it’s designed to help you handle unexpected expenses without stress.

Conclusion

Practising mindful spending is one of the most effective ways to strengthen your financial health in 2026. By tracking your expenses, setting clear priorities, and making intentional choices, you can take control of your money instead of letting it control you.

Spending management isn’t about restriction; it’s about aligning your money with your goals and values, reducing stress, and building a more secure future.

When unexpected expenses arise, tools like Pocketly can provide quick, responsible support so short-term gaps don’t derail your long-term plan.

Ready to take charge of your finances? Download the Pocketly app today on [Android] or [iOS] and experience smarter, stress-free spending management.

FAQs

1. What is spending management?

Spending management is the practice of tracking, planning, and controlling your expenses to ensure your income aligns with your financial goals. It helps you prevent overspending and make informed financial decisions.

2. How is spending management different from budgeting?

Budgeting is a plan for your money, while spending management focuses on controlling actual expenses, adjusting habits, and making sure your spending stays within your plan.

3. Why is spending management important for young professionals?

It helps manage lifestyle expenses, avoid debt, save consistently, and maintain financial stability despite rising costs in cities like Bengaluru, Mumbai, or Delhi.

4. Can spending management help with unexpected expenses?

Yes. By tracking spending and maintaining emergency funds, or using short-term solutions like Pocketly, you can cover urgent costs without derailing your financial goals.

5. How often should I review my spending?

Weekly or at least monthly. Regular reviews help you spot overspending, adjust budgets, and stay on track toward your financial objectives.