Life doesn’t wait for payday. Unexpected bills, urgent medical expenses, or last-minute travel can arrive before your salary does, leaving your wallet empty and your stress high.

Reaching for fast cash might feel like the only solution, but not all short-term loans are created equal. Payday loans and cash advances can seem similar, yet they differ in costs, repayment terms, and risk. Choosing the wrong one can trap you in debt instead of solving your problem.

Knowing the difference between payday loans and cash advances helps you make smarter decisions when time and money are tight. In this blog, we break down how each works, highlight the hidden costs, and show practical ways to use them responsibly. With the right approach, you can cover urgent expenses quickly while keeping your finances under control.

TL;DR

- Quick Cash Options Explained: Payday loans give short-term cash against your next paycheck; cash advances let you borrow using your credit card or bank account.

- Cost Matters: Payday loans often have steep interest and hidden fees, while cash advances can be cheaper if repaid promptly.

- Credit Impact: Payday loans may stay off your credit report unless missed; cash advances affect credit utilisation, and timely repayment influences your score.

- When to Use: Ideal for true emergencies covering bills, medical needs, or urgent expenses, not lifestyle spending.

- Responsible Borrowing Wins: Understand fees, repayment timelines, and limits before choosing to avoid debt traps and stay financially stable.

What Is a Payday Loan?

A payday loan is a short-term, small-dollar loan designed to cover urgent expenses until your next paycheck. Unlike traditional loans, it’s meant to quickly bridge temporary cash gaps rather than fund long-term goals.

A payday loan is a short-term, small-dollar loan designed to cover urgent expenses until your next paycheck. Unlike traditional loans, it’s meant to quickly bridge temporary cash gaps rather than fund long-term goals.

Key Features of Payday Loans

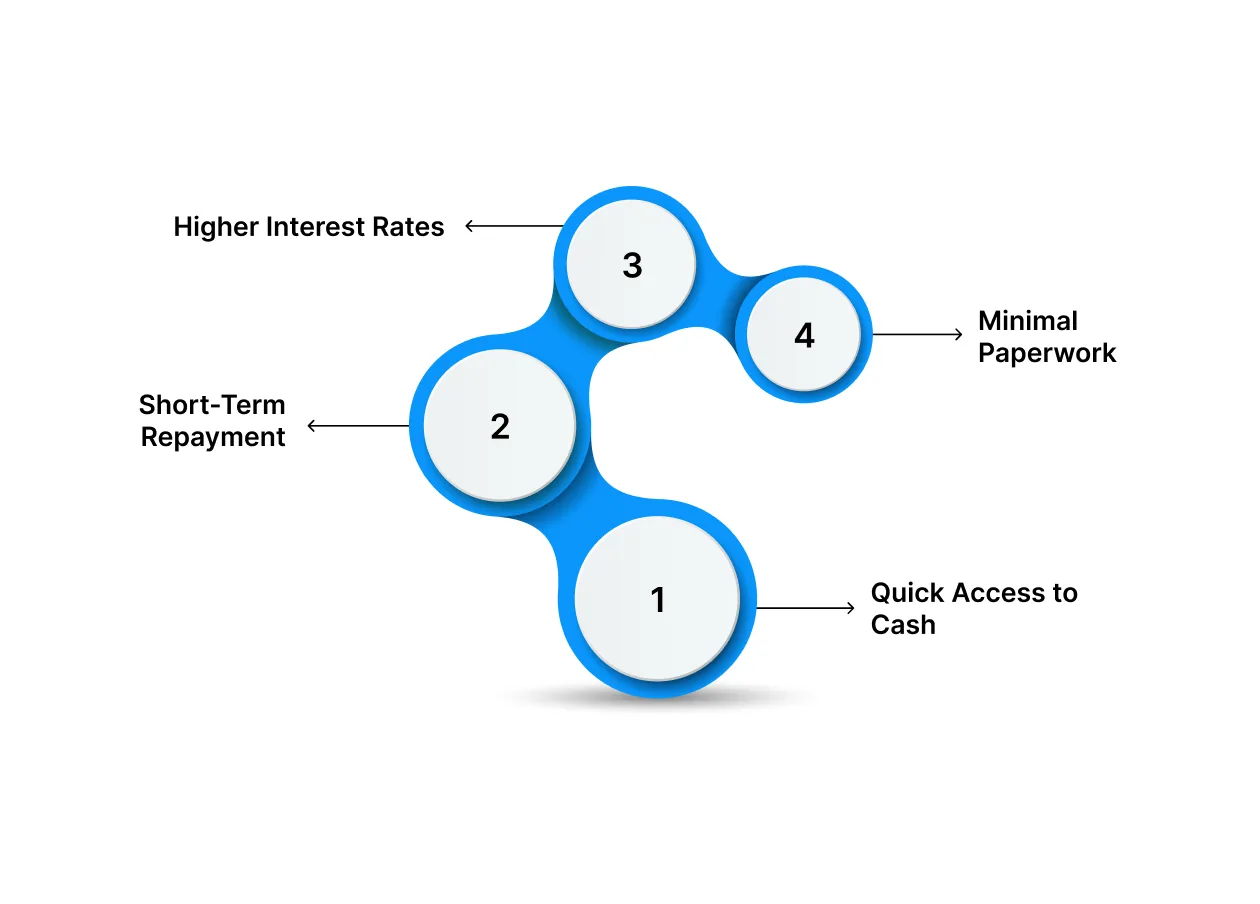

- Quick Access to Cash: Loans typically range from ₹1,000 to ₹25,000, giving you immediate funds for urgent needs.

- Short-Term Repayment: Repayment is usually due within two to four weeks, often aligned with your salary cycle.

- Higher Interest Rates: Payday loans carry higher interest rates due to the convenience and speed they offer.

- Minimal Paperwork: Only basic KYC documents and proof of income are needed for approval.

Real-Life Example: Suppose an unexpected medical bill of ₹8,000 pops up before your salary arrives. A payday loan can provide instant funds to cover the expense, with repayment scheduled for your next paycheck, preventing financial stress.

What Is a Cash Advance?

A cash advance is a short-term loan taken directly from your credit card or a line of credit. It allows you to access funds instantly, but unlike payday loans, it uses your existing credit limit and comes with its own set of costs and rules.

Key Features of Cash Advances

- Borrow from Your Credit: Funds are drawn from your credit card limit or line of credit, so you don’t need a separate loan application.

- Immediate Availability: Cash is accessible instantly via ATMs or bank transfer.

- Interest and Fees: Cash advances often have high interest rates and additional service fees, with interest starting immediately from the day you borrow.

- Short-Term Repayment: While flexible, repayment is tied to your credit card billing cycle or line of credit terms.

Real-Life Example: Imagine your wallet is empty, and you need ₹10,000 urgently for car repairs. A cash advance lets you withdraw the amount immediately using your credit card. While convenient, the high interest and fees mean you should repay it as soon as possible to avoid escalating costs.

Payday Loan vs Cash Advance: Key Differences

When you need cash quickly, both payday loans and cash advances can provide short-term relief, but they work very differently. Understanding their features, costs, and repayment terms can help you choose the option that won’t trap you in debt.

Here’s a clear side-by-side comparison:

| Feature | Payday Loan | Cash Advance |

| Source | Borrowed from a lender or payday loan provider | Borrowed from your credit card or line of credit |

| Loan Amount | Usually small, ₹5,000–₹25,000 | Limited by your available credit limit |

| Repayment Timeline | Short-term, typically due on next payday (2–4 weeks) | Flexible, repaid according to credit card billing cycle or line of credit terms |

| Cost | High interest + fees | Immediate interest + cash advance fee (often 2–5%) |

| Application Process | Quick approval, minimal documentation | Instant via card, but requires sufficient credit |

| Ideal Use | Urgent expenses without access to a credit card | Short-term cash needs using your existing credit line |

| Risks | Easy to get trapped in a debt cycle | Interest compounds daily, increasing the overall cost |

Also Read: Understanding Minimum and Maximum CIBIL Score for Personal Loans and Credit Cards

When to Use a Payday Loan vs a Cash Advance

Choosing the right short-term borrowing option depends on your urgency, available resources, and repayment ability. Here’s a guide to help you decide:

When a Payday Loan Makes Sense

- Emergency without credit access: If you don’t have a credit card or line of credit, payday loans can provide instant cash for urgent needs.

- Small, one-time expense: Ideal for a single short-term cost, like an urgent medical bill, travel emergency, or utility payment.

- Predictable repayment: You can repay the loan on your next payday without relying on revolving credit.

When a Cash Advance Is Better

- Credit card available: If you have a credit card with enough available limit, a cash advance is often faster and simpler.

- Short-term flexibility: Useful for small, immediate needs where you can pay off the amount quickly within the billing cycle.

- Avoiding multiple lenders: Keeps your borrowing within existing credit facilities, reducing paperwork and new applications.

Key Takeaway: Use a payday loan only when you lack credit access or need a predictable short-term repayment plan. Use a cash advance if you have available credit and can repay quickly to avoid compounding interest.

Tips to Avoid Payday Loan and Cash Advance Traps

Short-term loans can be lifesavers, but if mismanaged, they can trap you in a cycle of debt. Follow these practical tips to stay in control:

Short-term loans can be lifesavers, but if mismanaged, they can trap you in a cycle of debt. Follow these practical tips to stay in control:

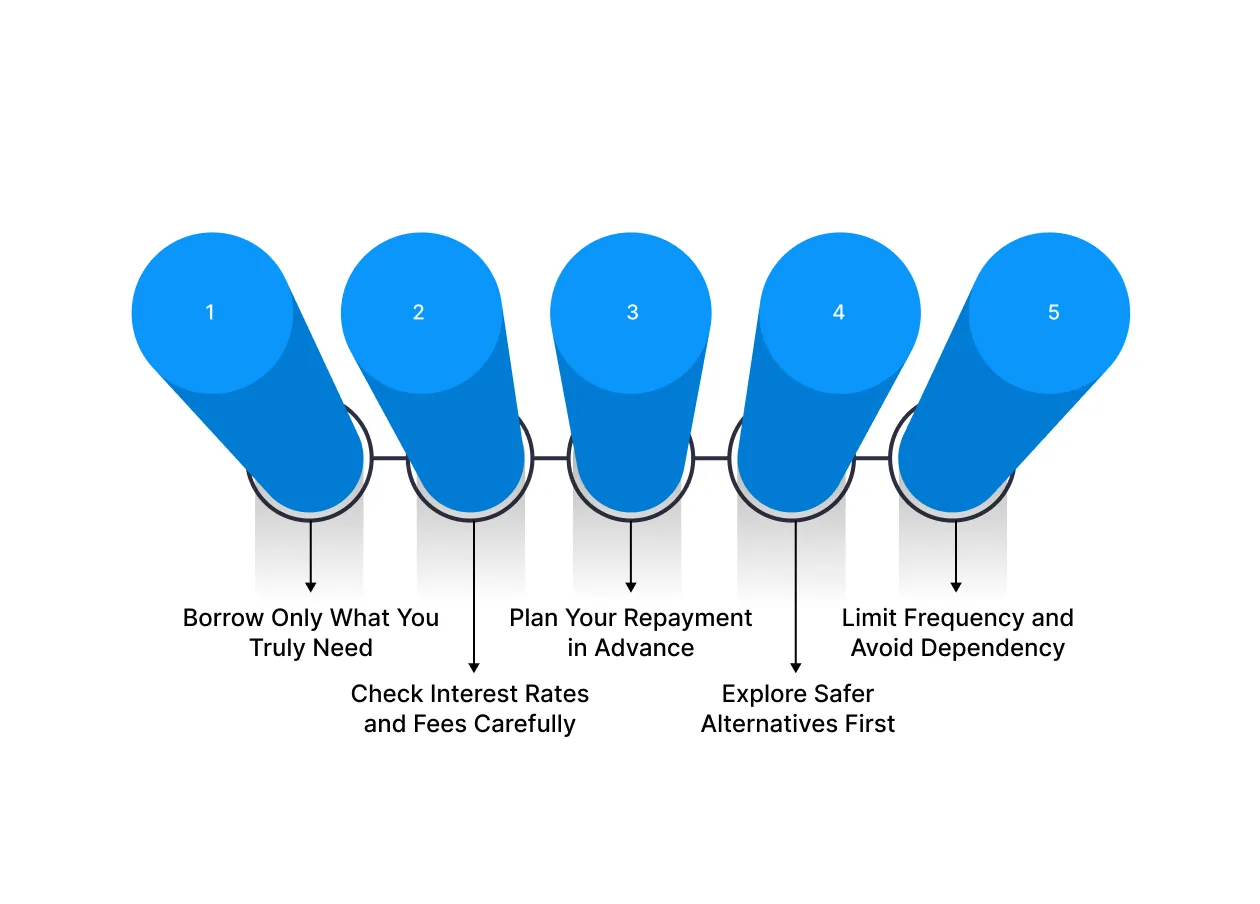

Borrow Only What You Truly Need

Taking more than necessary might seem convenient, but it can backfire with higher repayments and unnecessary interest costs. Always evaluate the exact amount required for the urgent situation and stick to it. This reduces financial stress and keeps your repayment manageable.

For example, imagine you need ₹7,000 for an urgent medical test. If you take a ₹15,000 payday loan instead, the extra ₹8,000 might tempt you to spend it on non-essentials, and you’ll pay interest on the full amount. Borrowing only what’s needed ensures you cover the emergency without creating avoidable debt.

Check Interest Rates and Fees Carefully

Payday loans and cash advances often appear quick and easy, but their costs can vary significantly. Understanding interest rates, processing fees, and hidden charges is crucial before committing. A small difference in rates can translate into hundreds or even thousands of rupees in extra payments.

For example, two lenders may offer a ₹10,000 loan for 15 days. Lender A charges 2% interest per month, while Lender B charges 4%. Even though both loans provide the same amount, choosing Lender A could save you ₹100–₹200 or more, depending on fees. Always read the fine print to avoid surprises.

Plan Your Repayment in Advance

Failing to plan repayment can trigger late fees, additional interest, and a spiral of debt. Treat payday loan or cash advance repayment dates like any other fixed bill. Knowing how and when you’ll repay ensures you maintain control over your finances.

For example, if your ₹10,000 loan is due in 15 days, mark it on your calendar and ensure the money is set aside. Missing the deadline could add 2–3% extra interest, meaning a small gap can become a larger burden quickly. Planning ahead prevents stress and keeps your credit record clean.

Explore Safer Alternatives First

Payday loans and cash advances should be last-resort options. Whenever possible, tap into safer alternatives like emergency savings, personal loans with lower interest, or trusted friends and family. These options often cost less and carry fewer risks.

For example, if you need ₹5,000 to cover an unexpected bill, using your emergency fund avoids the 3–4% interest typical of payday loans. Alternatively, borrowing from a friend with a clear repayment plan can cost zero interest. Choosing alternatives can save money and protect your financial health.

Limit Frequency and Avoid Dependency

Using payday loans regularly can trap you in a cycle of debt. Treat them strictly as emergency tools and not a monthly financial crutch. Over time, frequent borrowing can increase stress, reduce financial flexibility, and harm your creditworthiness.

For example, if you take a payday loan every month to cover lifestyle gaps rather than adjusting your budget, you may end up paying significant interest over a year—money that could have gone into savings. Limiting use ensures these loans serve their purpose without undermining long-term financial stability.

Also Read: Applying for an Instant Personal Credit Line Online

Short on Cash Before Payday? Pocketly Makes Borrowing Simple and Safe

When unexpected expenses hit, and your salary is still a few days away, Pocketly provides a quick, reliable way to bridge the gap. Designed for young professionals in India, Pocketly offers instant loans with clear terms, helping you manage urgent payments without falling into high-interest debt.

Here’s why Pocketly stands out:

- Borrow only what you need: Loan amounts range from ₹1,000 to ₹25,000, so you never take on more than necessary.

- No collateral or guarantor required: Apply easily without pledging assets or finding a co-signer.

- Fast approval: Quick KYC-based verification ensures near-instant decisions.

- Instant fund transfer: Get money directly in your bank account immediately after approval.

- Flexible repayment: Choose a plan that aligns with your budget, keeping EMIs manageable.

- Transparent pricing: Interest starts from just 2% per month with processing fees between 1–8%.

- 24/7 access via mobile app: Apply, track, and manage your loan anytime, anywhere.

Used responsibly, Pocketly acts as a financial bridge during short-term cash crunches, letting you handle urgent expenses without derailing your monthly budgeting goals.

Conclusion

Payday loans and cash advances can help you cover urgent expenses, but each comes with its own costs and risks. Payday loans provide quick cash without collateral but can carry high fees if not repaid promptly. Cash advances use your existing credit and may be slightly cheaper, yet missed payments can impact your credit score.

Choosing the right option means understanding your needs, repayment ability, and long-term financial goals. Borrow only what you need, plan repayments carefully, and consider safer alternatives when possible.

When used responsibly, these tools can bridge short-term gaps without harming your financial stability. Stay informed, make intentional choices, and keep control of your money.

Download the Pocketly app today on [Android] or [iOS] to access funds instantly and keep your finances steady, no matter what comes your way.

FAQs

1. What is the main difference between a payday loan and a cash advance?

A payday loan is a short-term loan that you borrow from a lender against your next salary, usually with high interest rates and fees. A cash advance, on the other hand, is borrowing money using your credit card limit or through your bank, sometimes with lower interest if repaid quickly.

2. Which is cheaper in India: a payday loan or a cash advance?

Cash advances generally have lower interest rates compared to payday loans, especially if you repay within your credit card’s interest-free period. Payday loans tend to be more expensive due to high short-term interest and fees.

3. Can taking a payday loan or cash advance affect my credit score?

Yes. Payday loans usually do not report to credit bureaus if repaid on time, but defaults can still impact your financial record with lenders. Cash advances affect your credit utilisation, and late repayments can negatively affect your credit score.

4. What is the safest alternative to payday loans in India?

Short-term personal loans from regulated banks or NBFCs, like Pocketly, are safer. They offer transparent interest rates, flexible repayment, and smaller loan amounts without hidden charges, making them a responsible option for urgent expenses.

5. How quickly can I get money from a payday loan vs a cash advance?

Payday loans can provide funds within a few hours to one business day after approval. Cash advances from credit cards or bank accounts are usually instant or same-day, depending on your bank and transaction method.