An urgent expense rarely comes with a warning. It could be a medical bill, a rent gap, or a repair you cannot delay. In such moments, a pawn loan often feels like the quickest way to access cash.

You pledge an item, receive money, and plan to repay it soon.

But here’s where most borrowers misjudge the situation: A pawn loan may look simple, but the total repayment is often higher than expected.

Interest is usually charged monthly on the full amount, and additional fees such as appraisal, storage, and penalties can increase the cost further. What starts as a short-term solution can become more expensive if the structure is not clearly understood.

This blog breaks down how pawn loan interest and fees are calculated, what actually drives the total cost, and how to evaluate whether this option fits your situation before borrowing.

Key Takeaways

-

Pawn loan interest is usually charged monthly on the full loan amount, so the cost can rise quickly if repayment is delayed.

-

The total repayment includes more than the interest. Fees such as appraisal, processing, storage, and late penalties can add up.

-

Missing the due date can do more than increase the amount payable. It can also lead to the loss of your pledged item.

-

Focusing only on interest rates can be misleading. The total payable amount, including all charges, gives the real cost.

-

Pawn loans may meet urgent needs quickly, but they come with higher costs, visibility issues, and asset risk if repayment is uncertain.

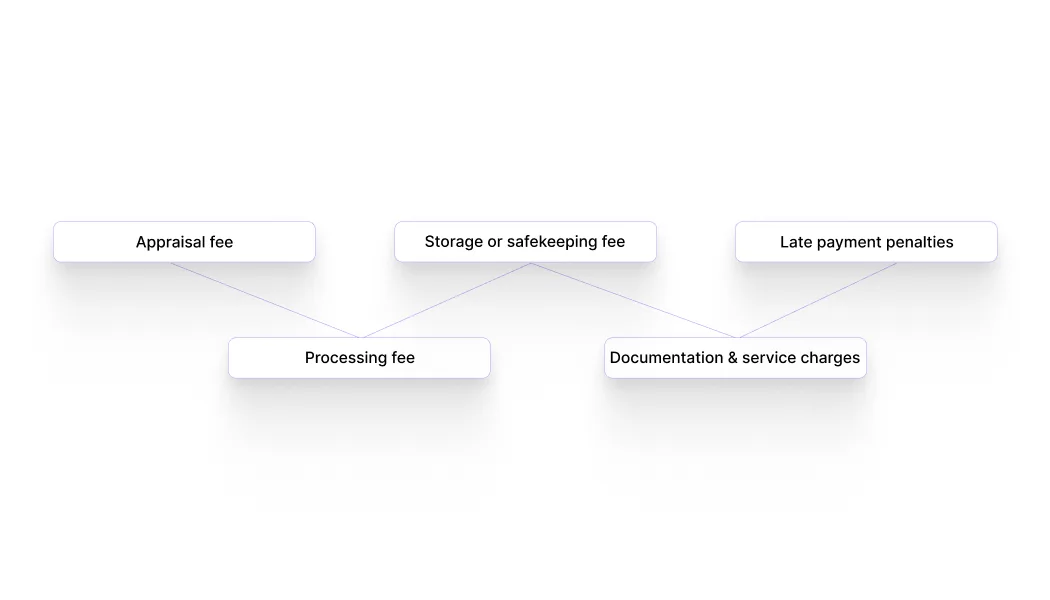

All Pawn Loan Charges That Increase Your Total Cost

Interest is only one part of what you pay in a pawn loan. The total cost increases because of multiple charges that are added at different stages of the loan.

If these are not checked upfront, the final repayment amount can be higher than expected.

Here are the key charges that affect your total cost:

-

Appraisal fee: Charged for evaluating the value of the item you pledge. This may be deducted from the loan amount or added separately.

-

Processing fee: A one-time charge for setting up the loan. It reduces the amount you receive or increases the total payable.

-

Storage or safekeeping fee: Applied for holding your pledged item securely during the loan period. This can continue until the loan is closed.

-

Documentation or service charges: Small administrative fees that may be included in the agreement.

-

Late payment penalties: Added if you miss the repayment date or extend the loan duration.

Individually, these charges may seem small. But when combined with monthly interest, they can significantly increase the total repayment.

Also Read: Applying for an Instant Personal Credit Line Online

How Pawn Loan Costs Add Up Over Time

The real cost of a pawn loan is not just the interest rate. It is the total amount you repay after combining interest, fees, and time.

Here is how it builds:

Total repayment = Principal + Monthly interest + All fees + Any penalties

The challenge is that these costs are not always presented together. They are added at different stages, making it harder to see the full picture upfront.

For example, a small loan may look manageable at first. But if repayment is delayed, another cycle of monthly interest is added, along with possible storage or penalty charges. Even a short extension can increase the final amount noticeably.

This is why focusing only on the interest rate can be misleading. The real impact comes from how long the loan stays active and how many additional charges get applied during that period.

Don’t let unexpected fees and interest rates surprise you. Understand the true cost of a pawn loan before borrowing. Pocketly offers a clear, upfront breakdown of all costs, ensuring you’re prepared for repayment without risking your valuables. Get in touch now!

What Happens If You Miss Pawn Loan Repayment

A pawn loan is directly tied to the item you pledge. This means the consequence of missing repayment is not limited to additional charges. It can lead to losing your assets.

Here is what typically happens:

-

Additional charges are applied: Missing the due date can trigger late fees and another cycle of monthly interest

-

Loan extension increases cost: If the loan is renewed, new interest and service charges are added, raising the total repayment.

-

Ownership of the item is at risk: If the loan remains unpaid, the lender has the right to sell the pledged item to recover the amount.

-

No recovery after sale: Once the item is sold, you cannot reclaim it, even if you arrange the money later

For example, a borrower who pledges jewelry for a short-term need may plan to repay quickly. If repayment is delayed, the loan may move into extension or default, increasing the cost and risking permanent loss of the item.

This makes repayment timing critical. Before taking a pawn loan, it is important to be clear about when and how you will repay, not just how quickly you can borrow.

Also Read: How to Pay Off Loans Quickly and Easily

Common Pawn Loan Cost Traps Borrowers Miss

Even when borrowers understand interest and fees, the real cost often increases because of how the loan is used.

Here are the most common mistakes:

-

Focusing only on the interest rate: The total repayment includes multiple charges, not just the monthly rate

-

Extending the loan duration: Each extension adds another cycle of interest and fees, increasing the final cost

-

Paying only interest without closing the loan: This keeps the loan active and raises the total amount paid over time

-

Not checking total repayment upfront: Without clarity on the full amount, it becomes difficult to plan repayment

-

Ignoring penalty terms: Even short delays can trigger additional charges that increase cost quickly

For example, many borrowers plan to repay quickly but end up extending the loan. This adds new interest cycles and fees, making the final repayment higher than expected.

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

When Pawn Loans Make Sense and When They Don’t

Pawn loans can be useful in certain situations, but they are not the right choice for every type of borrowing need.

When a Pawn Loan Makes Sense

-

You need immediate cash and have no access to other options: Pledging an asset may be the fastest way to arrange funds.

-

You have a clear and short repayment timeline: Knowing exactly when you can repay helps avoid additional cost and risk.

-

You are comfortable with the risk involved: The pledged item should be something you can afford to lose if repayment is delayed.

When a Pawn Loan May Not Be the Right Choice

-

The required amount is small: For smaller needs, pledging an asset may increase risk unnecessarily

-

Your repayment timing is uncertain: Delays can quickly increase cost and risk loss of the item

-

The pledged item has high personal value: Losing it may have emotional or long-term impact beyond its monetary worth.

-

You want to avoid layered charges and penalties: Fees and extensions can increase total repayment if the loan is not closed quickly.

In simple terms, a pawn loan works when the need is urgent and repayment is certain. It becomes risky when timing is unclear or the amount required is relatively small.

If your requirement is urgent but limited, it may be worth checking whether a smaller unsecured option like Pocketly fits better than pledging a valuable item. Apply for a loan now!

Pawn Loan Options and Alternatives You Should Compare in 2026

Choosing the right borrowing option depends on how much money you need, how quickly you can repay it, and what level of risk you are comfortable taking.

Here are the main options to compare:

Local Pawn Shops

Traditional pawn shops offer quick cash against items such as gold, jewellery, watches, or electronics.

Pros: Fast access to money, minimal documentation, easier approval

Cons: Monthly interest, multiple fees, and risk of losing the pledged item

This option may work when immediate cash is needed and repayment is certain within a short period.

NBFC-Backed Gold Loans

Some borrowers choose gold loans from regulated NBFCs instead of local pawn lenders.

Pros: More structured process, clearer terms, regulated lending

Cons: Your gold is still pledged, and charges may still apply if repayment is delayed

This may be more suitable for borrowers who prefer a formal lending channel but are comfortable using gold as collateral.

Personal Loans or Credit Lines

For borrowers with stronger eligibility, unsecured options like personal loans or credit lines may be available.

Pros: No collateral risk, more structured repayment

Cons: Approval depends on credit profile, and processing may take longer

These options are better suited for borrowers who qualify and need a more formal repayment structure.

Small Loan Options Like Pocketly

If the requirement is smaller, a pawn loan may not be the most practical choice. Pledging a valuable item for a limited borrowing need can increase both cost and risk unnecessarily.

Pocketly is designed for such smaller, short-term needs.

Pros: No collateral, quick digital process, loan amounts suited for short-term gaps

Cons: Not meant for large borrowing requirements

This is more suitable when the goal is to handle a smaller urgent expense without risking a personal asset.

Before choosing a pawn loan, compare the full repayment and check whether a smaller short-term option like Pocketly can solve the gap without collateral risk.

Avoid Pawn Loan Risks for Small Amounts with Pocketly

Pawn loans can solve urgent needs, but they come with a clear trade-off. You are putting a valuable item at risk, often for a relatively small amount.

If your requirement is limited, taking that risk may not be necessary.

This is where Pocketly becomes a more practical option.

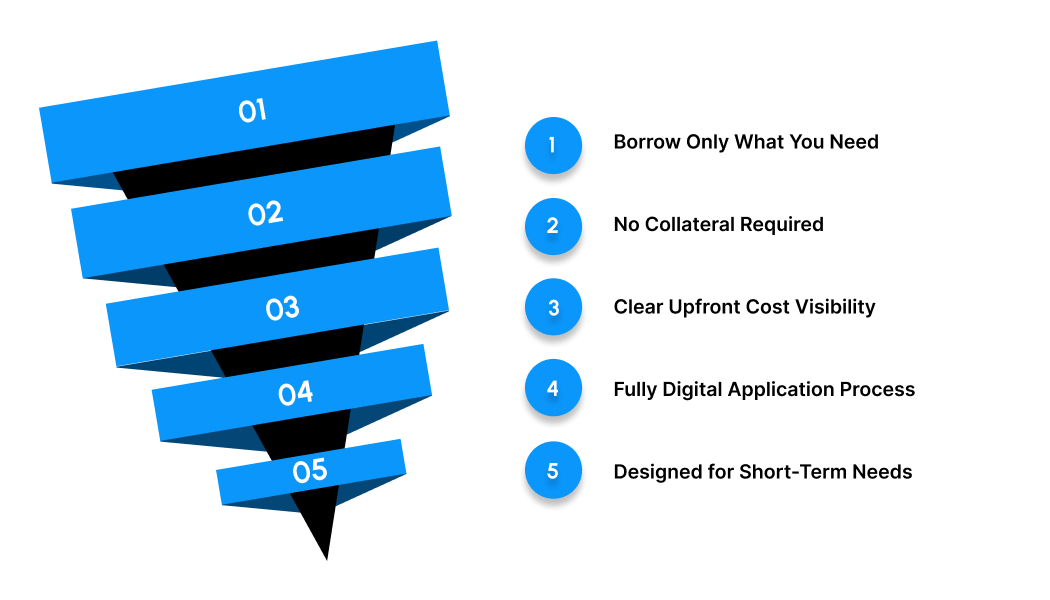

Pocketly is designed for small, short-term borrowing needs, where the focus is on resolving the expense without entering a longer repayment cycle or pledging an asset.

Here is how it fits better in such situations:

-

Loan amounts match smaller needs: You can borrow between ₹1,000 and ₹25,000, so you avoid taking more than required

-

No collateral involved: You do not need to pledge jewellery, gadgets, or any personal asset

-

Clear and upfront cost visibility: Interest and fees are shown before you proceed, helping you understand the total repayment

-

Quick, fully digital process: From application to disbursal, everything happens online without branch visits

-

Faster resolution of short-term gaps: The structure is designed for short repayment cycles instead of long-term debt

For smaller expenses like bill gaps, repairs, or urgent payments, this approach helps you solve the problem without adding unnecessary risk.

If your requirement is small and urgent, check your eligibility on Pocketly and review the total cost before choosing a larger loan or pledging an asset.

FAQs

Q: How is interest calculated on pawn loans in India?

Interest is usually charged monthly on the full loan amount. It does not always reduce with partial payments, so the total cost depends on how long the loan remains active.

Q: What fees are included in pawn loans besides interest?

Common charges include appraisal fees, storage costs, processing fees, and late payment penalties. These increase the total repayment beyond just interest.

Q: Are pawn loans expensive compared to other options?

Pawn loans can become expensive due to monthly interest and added fees, especially if repayment is delayed or the loan is extended.

Q: What happens if I cannot repay a pawn loan?

If the loan is not repaid, the lender can sell the pledged item to recover the amount. Once sold, the item cannot be claimed back.

Q: Is a pawn loan suitable for small expenses?

For smaller amounts, pledging an asset may not be necessary. Unsecured options can help manage short-term needs without the risk of losing valuables.

Q: When is Pocketly a better option than a pawn loan?

Pocketly is more suitable when the requirement is small and short-term, and you want to avoid collateral risk while keeping repayment simple and controlled.