Ever feel like your salary disappears before the month ends, even though you’re careful? You’re not imagining it. As per the stats, Indian household quarterly spending jumped over 33% to ₹56,000 in 2025, showing that everyday costs are rising faster than many budgets can handle.

That means rent, bills, groceries, travel, and surprise expenses squeeze your pocket long before your next paycheck arrives, leaving you guessing where your money went and scrambling to adjust. Without a clear way to track these flows, stress becomes the default, and saving feels impossible.

This is where a monthly expenses checklist becomes your financial compass. Instead of reacting to money surprises, a checklist gives you visibility into every rupee, helps you plan for essentials and planned costs, and lets you budget with confidence.

In this blog, you’ll learn exactly what to include and how to use it to bring clarity, control, and calm to your financial life.

Key Takeaways

-

A monthly expenses checklist doesn’t control your money for you; it shows exactly where every rupee goes.

-

Tracking your bills, groceries, subscriptions, and savings helps you spot leaks before they drain your wallet.

-

Small daily spends add up fast, and irregular costs like festivals or school fees can catch you off guard if not planned.

-

Updating your checklist weekly and comparing planned vs actual spending keeps overspending in check.

-

Consistency, prioritising essentials, and automating payments build financial control, reduce stress, and help you save smarter.

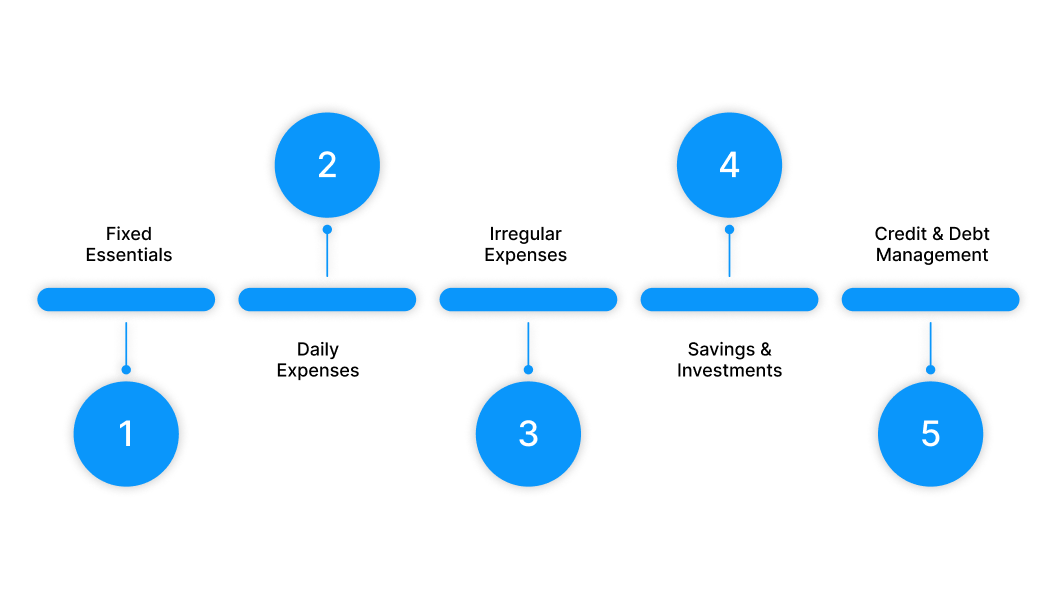

Track Every Rupee: The Monthly Expense Categories You Can’t Ignore

Before you plan, you need clarity. Categorising your spending helps spot leaks, control splurges, and save more without sacrificing lifestyle.

1. Fixed Essentials: Bills, EMIs, and Must-Pays

These are non-negotiable monthly commitments:

-

Rent / Housing: Even if living with family, account for contributions.

-

Utilities: Electricity, water, gas, broadband, and mobile recharge.

-

EMIs & Loans: Home, personal, vehicle loans.

-

Insurance Premiums: Health, life, vehicle insurance.

2. Daily Expenses: The Little Things That Add Up Fast

Small everyday spending often gets overlooked, but can explode your budget:

-

Groceries & Essentials: Weekly meal planning prevents impulsive buys.

-

Transport & Fuel: Fuel, cab rides, metro/auto fares.

-

Food & Drinks Outside: Cafes, takeaways, and occasional dining out.

-

Subscriptions: OTT, news, fitness apps, or music services.

3. Irregular Expenses: Festivals, Gifts, and Life Events

Expenses that don’t occur every month but are predictable in India:

-

Festivals, puja expenses, weddings, birthdays.

-

School/college fees, coaching classes, exam costs.

-

Health check-ups, medicines, vaccinations.

4. Savings & Investments: Paying Your Future Self

Investing consistently now sets you up for financial freedom:

-

SIPs & Mutual Funds: Even ₹500/month grows over time.

-

Emergency Fund: Keep 3–6 months’ worth of expenses ready.

-

Retirement & Long-Term Goals: PPF, NPS, recurring deposits.

5. Credit & Debt Management: Stay Out of Trouble

Managing borrowed money is as important as earning it:

-

Credit card dues

-

Short-term loans or overdraft usage

-

Informal borrowing from friends/family

Also Read: How to Manage Budget vs Expenses Without Stress in 2026

The Ultimate Monthly Expenses Checklist: Plan, Track & Save Smartly

Stop wondering where your money went. With this checklist, you’ll see exactly where every rupee goes and take control of your finances like a pro.

Why This Checklist Works

-

Avoid surprises: Know your upcoming bills and EMIs before they hit.

-

Control overspending: Identify the leaks in your monthly budget.

-

Build smart habits: Regular tracking trains financial discipline and improves your credit profile.

What to Include in Your Checklist?

Here’s a template you can use and tweak for your lifestyle:

|

Category |

Planned (₹) |

Actual (₹) |

Notes/Comments |

|

Rent & Utilities |

12,000 |

12,000 |

Paid via UPI |

|

Groceries & Essentials |

5,000 |

4,800 |

Switched to weekly budgeting |

|

Transport / Fuel |

2,000 |

2,200 |

Extra for Ola/Uber |

|

EMIs / Loans |

6,000 |

6,000 |

Auto-debit |

|

Subscriptions |

1,000 |

1,000 |

Netflix, Spotify |

|

Savings / Investments |

3,000 |

3,000 |

SIPs & RD |

|

Misc / Unexpected |

1,500 |

2,000 |

Gifts, festival shopping |

Freelancers can add irregular income & client payments, while students can track tuition, coaching, or study material costs.

How to Use It Effectively?

-

Set It Up Before the Month Starts: Fill in planned amounts based on last month’s spending.

-

Track Weekly: Record actual spending every 5–7 days. Small delays make it hard to spot trends.

-

Compare & Adjust: Mid-month check-ins help you curb overspending before it becomes a problem.

-

Review & Optimise: End-of-month review highlights patterns, unnecessary costs, and opportunities to save more next month.

Go Digital for Maximum Ease

-

Google Sheets / Excel: Fully customisable and shareable.

-

Apps: Money View, Walnut, and Jupiter automatically track transactions.

-

Smart Reminders: Set UPI reminders or calendar alerts for recurring bills.

Stay in control of your money and your credit. Pocketly gives you instant access to ₹1,000–₹25,000 so you never miss a payment. Apply now and build a better financial future.

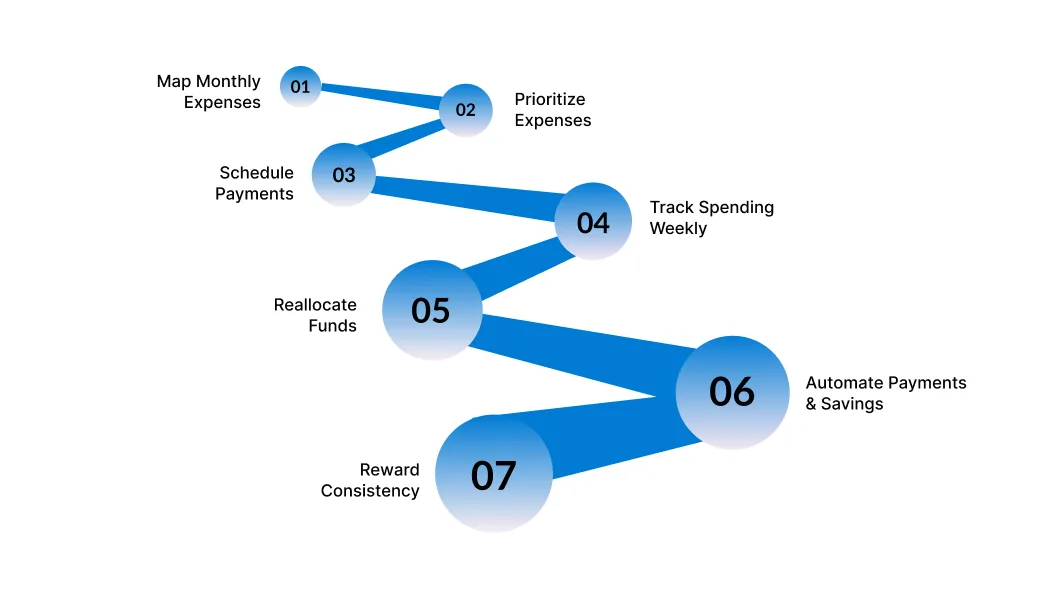

From Chaos to Control: How to Use Your Monthly Expenses Checklist Effectively

Tracking your money is only useful if you follow a clear system. Here’s how to turn your checklist into a powerful money management tool:

Step 1: Map Out All Your Monthly Expenses

The first step to controlling your money is knowing where it goes. List every expense, including fixed, variable, and occasional costs. Fixed expenses include rent, EMIs, insurance, and utilities. Variable expenses are groceries, transport, dining, and fuel. Don’t forget occasional or annual costs like festivals, birthdays, or subscription renewals.

Example: Reviewing your last 3 months of bank statements may reveal a ₹499 music streaming app you rarely use or multiple food delivery subscriptions you’ve forgotten about.

Step 2: Prioritise and Categorise Expenses

Divide your list into essential (needs) and non-essential (wants). Essentials include rent, EMIs, groceries, electricity, and transport. Non-essentials include OTT subscriptions, dining out, shopping, and premium memberships.

Example: Your grocery budget is ₹5,000, and your entertainment budget is ₹3,000. If a festival month stretches your cash, you might reduce dining or shopping while ensuring groceries and EMIs are covered.

Step 3: Schedule Payments and Set Reminders

Assign due dates to every bill, EMI, and subscription. Use a digital calendar, reminder apps, or WhatsApp alerts. Paying on time avoids late fees and prevents negative marks on your credit record.

Example: Set reminders 2–3 days before your electricity, mobile, or credit card bill is due. Paying a ₹500–₹1,000 late fee monthly is unnecessary stress you can avoid.

Step 4: Track Spending Weekly

Weekly monitoring prevents small overspending from snowballing. Compare your planned budget vs actual spend. Use notebooks, Excel, or apps like Money View or Walnut.

Example: You budgeted ₹2,500 for groceries, but by the 15th, you’ve spent ₹3,500. By adjusting dining or cutting non-essential shopping, you can stay within limits and avoid debt.

Step 5: Reassess and Reallocate Funds

At the end of the month, analyse where your money went. Identify patterns: overspending categories, unused subscriptions, or recurring cash leaks. Reallocate surplus money to savings, emergency funds, or investments.

Example: Spent ₹1,200 on OTT apps you rarely use? Cancel them and move that money to a recurring deposit or mutual fund SIP.

Step 6: Automate Payments and Savings

Set auto-debit for EMIs, insurance, mutual fund SIPs, and utility bills. Pre-schedule transfers to savings or emergency funds.

Example: Auto-debit your ₹5,000 SIP on the day your salary arrives. This ensures consistent investing without waiting or forgetting, building wealth slowly but surely.

Step 7: Reward Yourself for Consistency

Budgeting shouldn’t feel like deprivation. Reward yourself for hitting your monthly targets, staying within limits, or saving extra.

Example: Stayed under your entertainment budget this month? Treat yourself to a small outing, coffee, or snack while still keeping total spending within limits.

Stay on top of your monthly expenses without stress. Pocketly gives you ₹1,000–₹25,000 instantly to cover urgent bills or EMIs, so your checklist stays on track. Apply in minutes and manage your finances with ease.

Hidden Monthly Expenses Draining Your Salary and How to Fix Them

Even with a monthly checklist, some costs slip under the radar, like micro-fees, delayed payment penalties, or overlapping subscriptions. Catching these hidden drains early can reclaim hundreds or even thousands of rupees that silently vanish each month.

1. Ignoring Small Daily Expenses

Risk: Tiny daily spends like morning coffee, snacks, quick online orders, or app subscriptions may seem harmless, but over a month, they can silently drain hundreds or even thousands of rupees from your budget. Ignoring these adds up to gaps between planned and actual spending.

Mitigation: Track every expense, no matter how small. Use a budgeting app, digital notes, or a simple spreadsheet. Categorise each spend to spot patterns and identify recurring “hidden leaks". Over time, even trimming a few small purchases can make a noticeable difference in your monthly savings.

2. Forgetting Irregular Bills

Risk: Quarterly or annual payments such as insurance premiums, festival shopping, school fees, or subscriptions often catch people by surprise. Missing these payments can lead to penalties or disrupt your monthly cash flow.

Mitigation: Include a section in your checklist specifically for irregular or seasonal expenses. Set calendar reminders and maintain a small buffer in your account to cover them. This ensures that even big one-time payments don’t throw your monthly budget off balance.

3. Overestimating Income or Underestimating Spending

Risk: Overestimating your disposable income or underestimating monthly expenses can lead to overspending, leaving you short of essentials or unexpected costs. This often happens when budgeting is based on wishful thinking rather than actual numbers.

Mitigation: Budget conservatively by tracking past spending patterns. Allocate 10–15% of your income as an emergency buffer and adjust your projections weekly. Comparing planned vs actual spending helps you fine-tune your budget and prevent shortfalls.

4. Failing to Update Weekly

Risk: Many people create a monthly budget but rarely review it, causing blind spots in tracking. Without weekly updates, overspending or accumulating debts can go unnoticed until it’s too late.

Mitigation: Dedicate 5–10 minutes each week to update your checklist. Note all new expenses, compare them to planned spending, and adjust accordingly. Regular updates provide a clear picture of your cash flow and help catch issues before they escalate.

5. Mixing Savings and Expenses

Risk: Treating all your income as available for spending without separating savings, investments, or emergency funds can easily derail your financial goals. This often leads to impulsive purchases that eat into long-term plans.

Mitigation: Follow a “pay yourself first” strategy. Automate transfers to savings, investments, or emergency funds as soon as your salary is credited. Only budget with the money left after these allocations. This creates a disciplined spending pattern and ensures you’re building wealth while covering monthly expenses.

6. Ignoring Credit Card & Loan Repayments

Risk: Forgetting or delaying EMIs, credit card bills, or loan repayments can attract late fees, increase interest costs, and hurt your credit score. Even small lapses get tracked by banks and credit bureaus.

Mitigation: Add a dedicated section in your checklist for fixed financial obligations. Set up auto-debit wherever possible and note due dates in your budget. This ensures timely payments, avoids penalties, and keeps your credit profile healthy.

7. Spending Without Prioritisation

Risk: Splurging on non-essential items first often leaves insufficient funds for bills, savings, or necessary expenses. Without prioritisation, important obligations can get neglected.

Mitigation: Categorise expenses in your checklist: essentials, discretionary, and savings. Allocate money for essentials first, then savings, and finally discretionary spending. This keeps your finances balanced while still allowing room for enjoyment.

8. Not Accounting for Inflation & Price Hikes

Risk: Ignoring gradual increases in costs like groceries, fuel, or utility bills can slowly erode your purchasing power and throw off your monthly budget.

Mitigation: Update your expense estimates every few months to reflect rising costs. Factor in a small inflation buffer for variable expenses. This proactive approach ensures your budget remains realistic and protects your financial stability over time.

Running Short on Cash? Pocketly Helps You Cover Urgent Expenses Instantly

No matter how well you plan your monthly expenses, timing gaps can create shortfalls. A bill or EMI might be due before your salary arrives, or sudden costs can disrupt your budget. Even small delays can lead to late payments, impacting your credit score and overall financial stability.

Pocketly is designed to support you during these short-term gaps. It provides quick access to small amounts of money so you can manage urgent payments without stress.

Here’s how it helps:

-

Manage urgent payments on time: Avoid late fees or missed EMIs, even during tight financial situations.

-

Borrow only what’s necessary: Access ₹1,000–₹25,000 to cover immediate needs without extra burden.

-

Fast access when you need it most: A simple digital process ensures quick approval and direct transfer to your bank account.

-

No complicated eligibility barriers: You don’t need a strong credit history, collateral, or a guarantor to get started.

-

Repay in a way that fits your income cycle: Flexible repayment options let you manage your cash flow comfortably.

-

Clear, upfront costs: Interest starts at 2% per month, with processing fees between 1%–8%, so you always know the total cost.

-

Avoid unnecessary financial stress: Handle urgent payments without disrupting your monthly budget or savings goals.

-

Simple, app-based experience: From applying to tracking repayments, everything is managed in one place.

Pocketly works best as a short-term financial cushion, not a regular crutch. Used wisely, it helps you manage timing mismatches without disturbing your overall financial flow.

With instant access, easy approvals, and flexible repayments, you can take control of your monthly expenses and ensure your bills and EMIs are always paid on time.

Download Pocketly on iOS or Android and stay in control of your finances, even when unexpected costs come up.

FAQs

1. What exactly is a monthly expenses checklist?

A monthly expenses checklist is a simple tool to track all your income, bills, subscriptions, groceries, and savings. It helps you see where your money is going and plan better so you don’t overspend.

2. Why should I use a monthly expenses checklist in India?

Even small daily expenses like UPI payments, groceries, fuel, or OTT subscriptions can add up. A checklist helps you track everything, avoid late fees, and save for bigger goals like festivals, travel, or investments.

3. How often should I update my checklist?

Ideally, update it weekly or whenever you spend. This ensures your records are accurate, helps spot overspending early, and keeps your budget realistic.

4. Should I include savings and investments in my checklist?

Yes! Include SIPs, emergency funds, recurring deposits, and insurance. Tracking these alongside expenses gives a full picture of your finances and ensures you don’t overspend your income.

5. Can I use a checklist if my income isn’t fixed?

Absolutely. For freelancers or irregular salaries, use average past income and plan expenses in categories: fixed, variable, and occasional. This helps you stay on track even when cash flow changes.

6. What tools or apps can help me track my monthly expenses?

Google Sheets, Excel, or apps like Walnut, Money View, Jupiter, and UPI app history (Google Pay, PhonePe, Paytm) work well. Automate reminders for bills and recurring payments for better control.