Managing money in the digital age can feel overwhelming. With countless apps, payment methods, and financial services available at your fingertips, it’s easy to feel lost when it comes to making informed decisions. From securing digital payments to understanding interest rates on loans, lack of financial literacy can lead to poor choices, wasted money, and even financial fraud.

This confusion often leads to missed opportunities, hidden fees, and the fear of making the wrong financial move online. You could be unknowingly paying for unnecessary subscriptions, falling victim to scams, or struggling with mismanaged credit.

But here’s the good news: improving your digital financial literacy can help you regain control. With the right knowledge, you can confidently manage digital transactions, understand your credit, and make smarter decisions that align with your financial goals.

In this blog, we’ll break down what digital financial literacy is, why it’s essential, and practical steps you can take to improve your skills.

TL;DR

- Digital financial literacy is understanding and using online financial tools safely, from payments to loans and budgeting apps.

- It empowers you to make smart financial decisions, protect your personal data, and avoid scams.

- Key skills include mastering UPI, mobile wallets, credit management, and digital security.

- It improves access to better financial services and helps manage your money effectively in the digital age.

- Start by learning the basics of digital payments, securing your accounts, and understanding your credit score to improve your financial well-being.

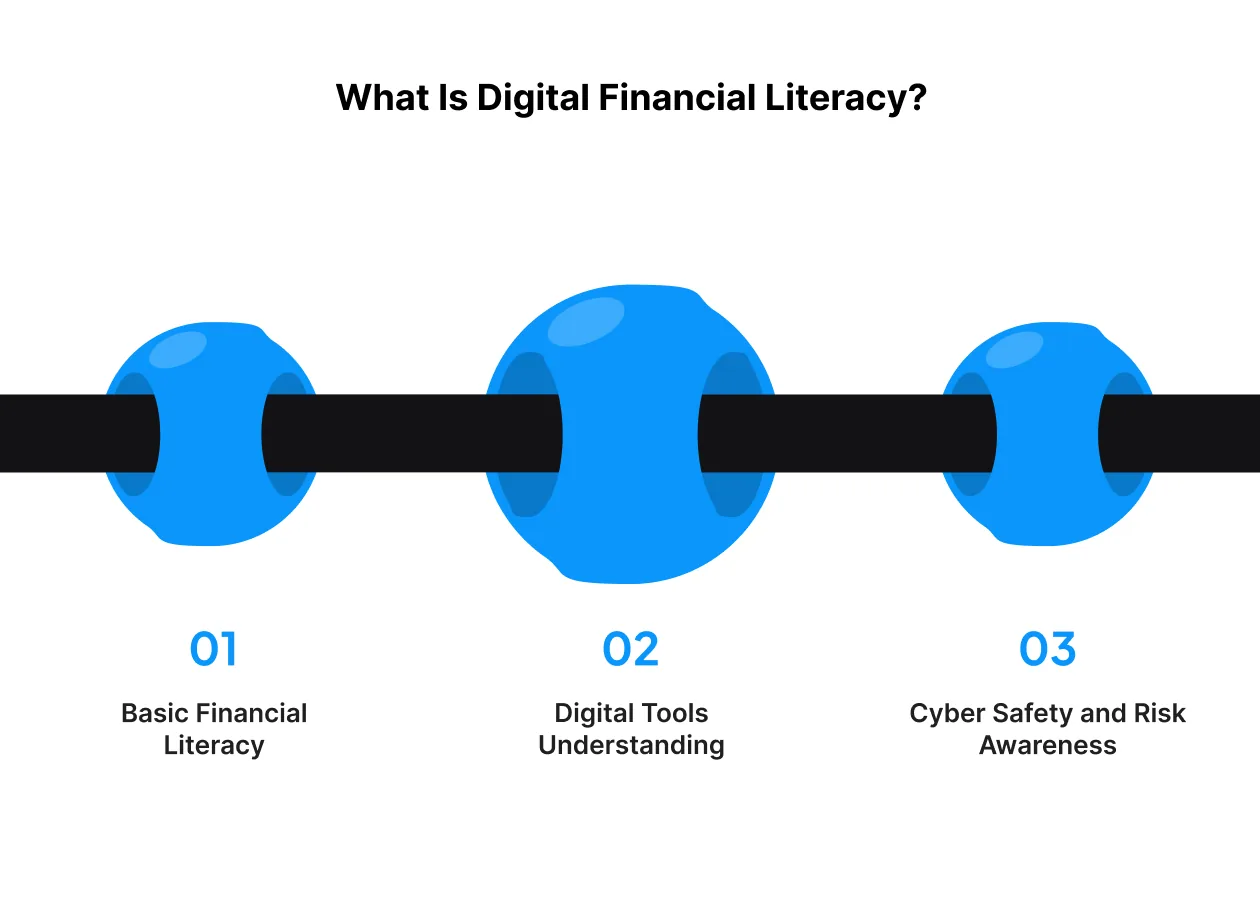

What Is Digital Financial Literacy?

Digital financial literacy is the capacity to understand and effectively use digital financial tools, manage online transactions, and navigate associated risks. It includes three key components:

Digital financial literacy is the capacity to understand and effectively use digital financial tools, manage online transactions, and navigate associated risks. It includes three key components:

1. Basic Financial Literacy (Budgeting, Saving, Credit)

- Budgeting: Managing income and expenses to avoid debt.

- Saving: Setting aside money for future requirements or emergencies.

- Credit: Understanding loans, credit cards, and credit scores.

2. Digital Tools Understanding (UPI, Mobile Wallets, Net Banking)

- UPI: A system for instant bank-to-bank transfers.

- Mobile Wallets: Apps like Paytm or Google Pay to store and transfer money.

- Net Banking: Online banking services to manage accounts and make payments.

3. Cyber Safety and Risk Awareness

- Protecting personal information from fraud and phishing.

- Using two-factor authentication (2FA) to secure accounts.

- Understanding risks in digital payments, lending, and online investments.

Why Digital Financial Literacy Matters Today?

As financial services continue to move online, digital financial literacy has become more important than ever. Here's why:

- Efficient Money Management: Digital literacy helps you track your spending, set budgets, and make better saving and investment choices.

- Avoiding Scams: Knowing how to identify fraud and use secure platforms safeguards your personal information and money.

- Easier Access to Financial Tools: From UPI to mobile wallets, being digitally literate enables you to use financial tools that simplify transactions and budgeting.

- Promoting Financial Inclusion: Digital financial skills allow those in remote areas to access banking, loans, and other essential services, bridging gaps in traditional banking.

- Informed Investment Decisions: With digital literacy, you can confidently navigate investment platforms, helping you make smarter decisions for long-term financial growth.

Mastering digital financial literacy equips you to manage your finances confidently, avoid risks, and find new opportunities in a rapidly evolving digital world.

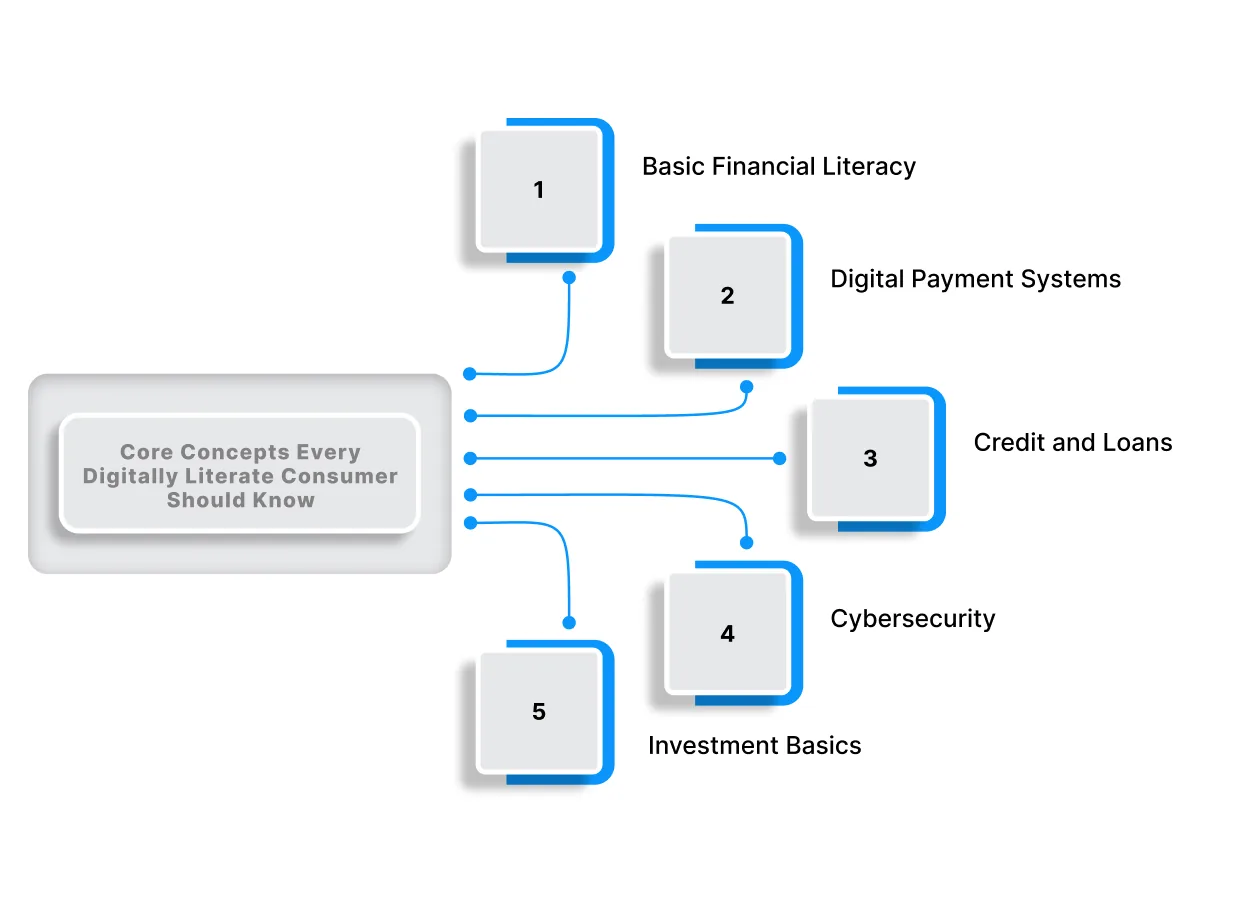

Core Concepts Every Digitally Literate Consumer Should Know

Financial literacy is more than just figuring out how to budget or save. With more financial tools and services moving online, being digitally literate means understanding how to use these tools safely and effectively.

Financial literacy is more than just figuring out how to budget or save. With more financial tools and services moving online, being digitally literate means understanding how to use these tools safely and effectively.

Here’s a breakdown of the key concepts every digitally literate consumer should grasp:

1. Basic Financial Literacy

Understanding core financial principles is still the foundation of good money management. Knowing how to manage your income, track spending, and save for the future is crucial:

- Budgeting: Allocating your income to expenses, savings, and debt repayments helps ensure you’re living within your means and setting aside for future needs.

- Saving: Building good saving habits can provide financial stability and protect you from emergencies.

- Credit Management: Knowing how to manage credit responsibly, understanding interest rates, and maintaining a healthy credit score is essential for accessing loans and credit cards at favourable terms.

2. Digital Payment Systems

Digital payments have transformed how we manage and spend money. Whether it’s sending money to a friend or paying for a meal, understanding these tools is key:

- UPI: UPI allows seamless, instant bank transfers directly from one account to another. It’s fast, simple, and increasingly popular for payments across India.

- Mobile Wallets: Apps like Paytm and Google Pay let you store money digitally, making payments quick and easy, all while offering perks like cashback.

- Net Banking: With net banking, you can manage your bank accounts, pay bills, transfer money, and even apply for loans all from your phone or computer.

3. Credit and Loans

Understanding how digital lending works is crucial in today’s economy. The rise of online loans and credit platforms has made borrowing easier, but also more complex:

- Digital Lending: Platforms like Pocketly allow instant loans through mobile apps. Knowing how to read loan terms, understand fees, and calculate interest is essential before borrowing.

- Credit Scores: Your credit score impacts your ability to get loans or credit cards, and knowing how to build and maintain a good score helps you get the best financial deals.

- Interest Rates: Knowing how interest is calculated on loans and understanding terms like APR and EMIs helps prevent falling into debt traps.

4. Cybersecurity

As we move towards digital banking and payments, cybersecurity becomes a key aspect of digital financial literacy. Protecting your financial data is just as essential as managing your money:

- Fraud Prevention: Recognising scams, phishing attempts, and fraudulent websites is vital to protecting yourself. It’s important to only use trusted and secure platforms for financial transactions.

- Secure Transactions: Always ensure that your bank and payment apps use encryption, and enable two-factor authentication (2FA) for added security.

- Data Privacy: Be mindful of what personal information you share online and make sure you’re using privacy settings to protect your data.

5. Investment Basics

Investing has become more accessible, but it requires understanding the basics. Here’s what you need to know to get started:

- Investment Platforms: Apps like Zerodha or Groww help you to invest in stocks, mutual funds, and ETFs easily. Knowing how these platforms work and how to use them is key to successful investing.

- Mutual Funds: SIPs (Systematic Investment Plans) make investing in mutual funds simple and affordable. You don’t need a large lump sum to start investing, just small, regular contributions.

- Risk Management: Understanding the risks involved in different types of investments, like stocks or bonds, and knowing how to diversify your portfolio helps you protect your wealth.

How Digital Financial Literacy Improves Your Financial Health

Digital financial literacy isn't just about using new tools; it’s about making smarter decisions that improve your overall financial well-being. When you're digitally literate, you can take control of your finances, save smarter, invest more effectively, and protect yourself from risks. Here's how:

1. Smarter Spending and Budgeting

With digital tools like budgeting apps, UPI, and mobile wallets, it’s easier than ever to track where your money is going. You can set budgets, track expenses in real-time, and adjust spending habits instantly, helping you stay within your limits and avoid overspending.

2. Quick Access to Financial Services

Digital financial literacy opens the door to a variety of financial services at your fingertips. From applying for loans to managing investments or even filing taxes online, understanding how to use these services allows you to make informed decisions and access financial products without relying on intermediaries.

3. Building Credit Responsibly

When you understand how digital credit works and the impact of your financial decisions, you can use credit more wisely. Whether it’s using a credit card, managing EMIs, or taking out loans, understanding terms like interest rates and credit limits helps you build and maintain a healthy credit score, which in turn lowers borrowing costs in the future.

4. Avoiding Online Fraud

With increased online activity comes the increased risk of fraud. Digital financial literacy helps you recognise phishing attacks, scam websites, and identity theft. You’ll learn how to secure your accounts and data, preventing financial losses and protecting your personal information.

5. Smart Investing for the Future

Being digitally literate means you can confidently navigate online investment platforms, from stocks and bonds to mutual funds and ETFs. You’ll know how to assess risks, diversify your investments, and use digital tools like SIPs and robo-advisors to make your money work for you. This approach can set you up for long-term financial growth and security.

You can also check our guide on Financial Planning Tips for Young Adults to understand financial planning in detail.

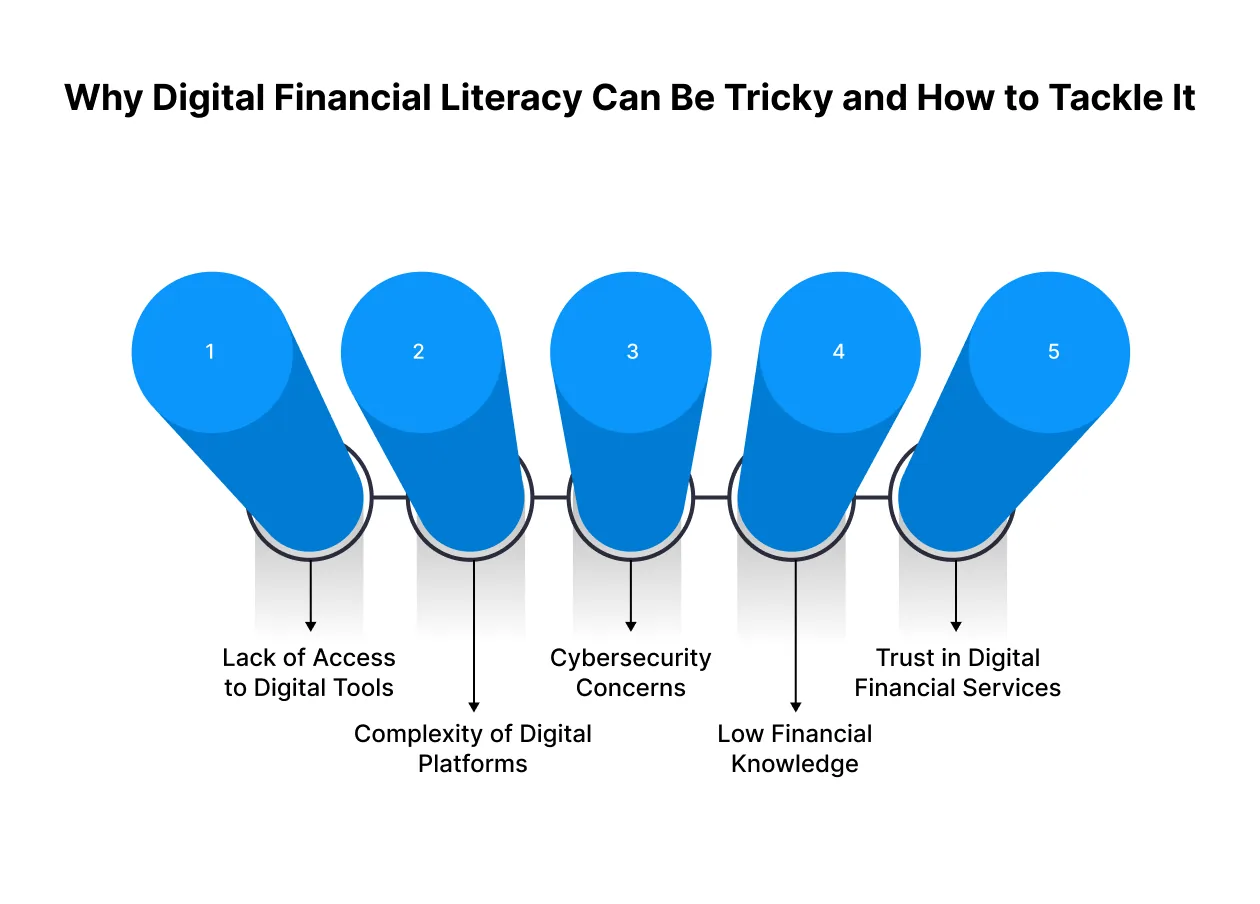

Why Digital Financial Literacy Can Be Tricky and How to Tackle It

While digital financial literacy offers many benefits, the journey to becoming financially literate in the digital world comes with its own set of challenges. From managing complex financial tools to overcoming security concerns, here’s a look at the common obstacles people face and how to overcome them:

While digital financial literacy offers many benefits, the journey to becoming financially literate in the digital world comes with its own set of challenges. From managing complex financial tools to overcoming security concerns, here’s a look at the common obstacles people face and how to overcome them:

1. Lack of Access to Digital Tools

In some regions, access to smartphones, the internet, or even reliable banking infrastructure can be limited. This lack of access makes it difficult for individuals to fully participate in the digital financial world.

- Solution: Work on expanding access to affordable smartphones and the internet, and consider offline methods of financial education to help bridge this gap.

2. Complexity of Digital Platforms

The rapid growth of digital finance has led to an overwhelming number of apps, platforms, and services. For many, figuring out how to use them effectively and understanding their features can be daunting.

- Solution: Simplify the process by focusing on core apps or tools (such as UPI for payments, or a single app for budgeting). Invest time in short, accessible tutorials or guides to become familiar with the basics.

3. Cybersecurity Concerns

One of the biggest barriers to digital financial literacy is the fear of fraud or identity theft. With increasing online transactions, the risk of phishing attacks, data breaches, and cybercrimes is growing.

- Solution: Prioritise cybersecurity education, including how to set strong passwords, enable two-factor authentication (2FA), and recognise fraudulent schemes.

4. Low Financial Knowledge

Many people struggle to understand even basic financial concepts, let alone more complex topics like digital lending, credit scores, and investing online.

- Solution: Focus on building foundational financial knowledge first, budgeting, saving, and debt management,t before moving on to more advanced concepts like investments and loans. Using simple, relatable examples can make the concepts easier to grasp.

5. Trust in Digital Financial Services

The lack of trust in digital financial platforms, whether due to security fears or past bad experiences, can make people hesitant to adopt online tools.

- Solution: Highlight the regulation and security protocols of digital financial platforms. Real-world examples of safe platforms can also help build trust and encourage adoption.

Achieving digital financial literacy is a process, and while there are hurdles, the benefits far outweigh the challenges.

The Future of Digital Financial Literacy

As the financial industry continues to evolve, so does the need for digital financial literacy. The future will bring more sophisticated financial tools, greater reliance on digital payments, and an increased need for security.

Here's a closer look at how digital financial literacy will shape the future and the skills you’ll need to stay ahead:

1. AI and Automation in Personal Finance

- Benefit: AI will simplify financial decision-making, offering more personalised budgeting, saving, and investment strategies.

- Outcome: Automated tools will allow users to make smarter financial choices with minimal effort, optimising their financial health.

2. The Rise of Digital Currencies and Blockchain

- Benefit: With the increasing popularity of cryptocurrencies, understanding blockchain technology will become essential.

- Outcome: Consumers will need to know how to navigate new digital currencies and understand their impact on the traditional financial systems.

3. Expanding Digital Payment Platforms

- Benefit: More payment apps and digital wallets will emerge, offering convenience and ease of use.

- Outcome: Staying digitally literate will help you seamlessly transition to new payment methods, enhancing your financial flexibility and security.

4. Growth in Digital Lending and AI-Driven Credit

- Benefit: Digital lending platforms will provide instant access to credit, revolutionising loan application processes.

- Outcome: Understanding the nuances of digital credit will allow individuals to borrow responsibly and make informed financial decisions.

5. Enhanced Security Features and Consumer Protection

- Benefit: Increased reliance on biometric verification, two-factor authentication, and blockchain security will make digital transactions safer.

- Outcome: Financially literate consumers will better understand and utilise these technologies to protect themselves from fraud and cyber threats.

To learn more about applying for a personal loan, check out our guide on Instant 1000 Personal Loan Online Approval.

When Digital Financial Tools Fall Short, Pocketly Bridges the Gap

For many, managing daily expenses is a challenge, especially when unexpected costs arise. Students, salaried professionals, and self-employed individuals often find that their monthly budgets are tight due to emergencies, delayed payments, or sudden expenses such as medical bills, urgent travel, or home repairs.

In these situations, the problem isn't always having enough money, but timing. With limited savings and no time to wait for paydays, people are often left scrambling for quick solutions.

This is where Pocketly steps in. Pocketly offers fast, flexible, and accessible short-term loans designed to cover urgent needs when timing becomes an issue. Without the need for a long credit history or collateral, Pocketly ensures that even individuals with little financial background can access funds easily.

Key Features of Pocketly During Financial Gaps

- Borrow only what you need, ranging from ₹1,000 to ₹25,000, to avoid over-borrowing

- No collateral or guarantors required

- Fast, paperless approval with basic digital verification

- Instant funds disbursed directly to your bank account

- Flexible repayment terms that align with your cash flow

- Transparent pricing, with interest rates starting at 2% per month and processing fees between 1% and 8%

With Pocketly, you can quickly cover sudden expenses without disrupting your essential payments, giving you the flexibility to manage life’s unpredictability.

Conclusion

Digital financial literacy isn’t just about knowing how to use apps or make payments; it’s about taking control of your finances and setting yourself up for long-term success. Mastering the basics of budgeting, credit management, and online safety today will not only help you avoid costly mistakes but will also pave the way for smarter financial decisions tomorrow.

As you improve your financial literacy, remember that it's a gradual process. You don't need to be an expert overnight. Start small by learning how digital tools like UPI, mobile wallets, and online banking work, and build from there. Over time, you’ll gain the confidence to make informed choices that suit your lifestyle and goals.

When life’s financial challenges arise, whether it’s unexpected bills or a cash flow crunch, don’t let them overwhelm you. Platforms like Pocketly are here to offer support, providing quick, flexible loans when needed. Pocketly helps you stay on top of things without disrupting your goals.

Download the Pocketly app on iOS or Android today to manage short-term expenses with ease and keep moving forward.

FAQs

1. What is digital financial literacy?

Digital financial literacy refers to the understanding and use of digital financial tools, services, and platforms, such as online

payments, digital banking, and mobile wallets, in a safe and informed way.

2. Why is digital financial literacy important in India?

With the rise of digital transactions and mobile banking in India, it is crucial to understand how to manage money, make payments, and avoid digital fraud. Being digitally financially literate ensures greater financial security and helps manage day-to-day finances effectively.

3. What are the core components of digital financial literacy?

The core components include understanding digital payment systems (like UPI and mobile wallets), credit management (such as credit scores), online security (protecting personal data), and making informed financial decisions through digital tools.

4. How can I improve my digital financial literacy?

Start by familiarising yourself with digital payment methods, learning about the importance of credit scores, ensuring online security, and practising safe financial habits with digital tools such as mobile banking and payment apps.

5. Does Pocketly require digital financial literacy?

Yes, understanding how digital lending works and being aware of terms like interest rates, repayment schedules, and digital security is essential when using services like Pocketly for short-term loans. This knowledge ensures safe borrowing and better financial management.