Have you ever received a salary increase and still wondered where the extra money went by the end of the month? It can feel confusing, especially when you expected things to get easier.

It often begins with small changes. You get a raise and expect some breathing room. For a month or two, it does feel better.

Then your expenses start adjusting. Rent goes up, food choices shift, a few subscriptions get added, and weekends become more expensive. This is something many young professionals, students, and self-employed individuals across Indian cities experience as their income grows.

Before you realise it, the extra income disappears, and you are dealing with the same financial pressure again. Over time, this reduces your ability to save and makes even small unexpected expenses harder to manage.

This pattern is called lifestyle inflation. In this blog, you will understand why it happens, how it affects your money, and what you can do to stay in control.

Key Takeaways

-

Lifestyle inflation happens when your spending rises along with your income without clear planning.

-

Small upgrades in rent, subscriptions, and daily habits can quietly become fixed monthly expenses.

-

This is why many people still face month-end cash gaps even after earning more, especially when unexpected expenses come up.

-

Controlling it means making selective upgrades and keeping part of your income flexible.

-

For short-term gaps, structured options with clear repayment terms can help you stay in control.

What Lifestyle Inflation Looks Like in Everyday Life

Lifestyle inflation rarely feels like a problem when it starts. It usually feels like progress. You move closer to work, upgrade your phone, order food more often, or take more trips. Each decision seems reasonable on its own.

The issue begins when these decisions become permanent expenses. A higher rent or a new EMI is not a one-time cost. It becomes a fixed commitment. Over time, your financial flexibility reduces without you noticing it.

For example, a ₹5,000 salary increase can quickly turn into a higher rent, a few subscriptions, and slightly higher daily spending. The extra income gets absorbed before it can strengthen your savings.

How Lifestyle Inflation Changes Your Spending

Small changes in spending often go unnoticed at first, but over time, they reshape how your money is allocated each month.

|

Situation |

Before Income Increase |

After Lifestyle Inflation |

|

Housing |

Affordable rent |

Higher rent or upgraded location |

|

Food & Dining |

Occasional eating out |

Frequent ordering and dining |

|

Subscriptions |

Limited or none |

Multiple recurring subscriptions |

|

Spending Behaviour |

Planned purchases |

Impulsive or convenience-driven spending |

|

Savings |

Some room to save |

Reduced or inconsistent savings |

|

Financial Flexibility |

Able to handle small expenses |

Frequent month-end cash gaps |

Over time, these small shifts turn into fixed patterns, making it harder to notice where your money is actually going.

Also Read: The Ultimate Guide to Small Business Loans in India (2026)

Why Your Expenses Rise Faster Than You Realise

A salary increase often changes how you think about affordability. What felt expensive earlier starts to feel manageable, and this shift happens without much planning. Over time, small decisions begin to reshape your monthly expenses in ways that are easy to miss.

1. Your Definition of Affordable, Changes Quickly

After a raise, spending limits feel less restrictive. You start accepting higher costs as normal, even when they were avoidable earlier.

For example, a ₹300 meal that felt occasional earlier can become a regular habit without much thought.

2. Social Comparison Influences Spending Decisions

Social comparison influences spending decisions because humans naturally gauge their own success and social standing by comparing themselves to peers, often leading to increased spending to 'keep up' even if it strains personal budgets.

3. Digital Payments Reduce Spending Awareness

Digital payments reduce spending awareness because the ease and speed of transactions minimise the psychological impact of spending money, making it less likely for individuals to monitor and control their expenses.

For example, multiple small UPI payments across the week can add up without you noticing the total impact.

4. Convenience Turns Into Recurring Costs

Services that save time often come with recurring charges that quietly increase your monthly commitments. Like, food delivery, OTT platforms, and ride apps can together form a significant fixed expense.

5. Small Expenses Compound Into Large Monthly Outflows

Individually, these costs feel minor. Combined, they can take up a noticeable portion of your income.

For example, five subscriptions of ₹199 each already add up to nearly ₹1,000 every month.

Note: Household spending in India has seen a sharp rise in recent years, with average quarterly expenses increasing to 33% from 2023 to 2025 as per the Economic Times. This shows how everyday costs are already putting pressure on budgets, even before lifestyle upgrades come into play.

If these patterns sound familiar, reviewing your monthly expenses once can help you identify where your money is actually going before it creates a cash gap.

The Hidden Problem: Why You Still Run Out of Money

The real issue with lifestyle inflation is not higher spending. It is the loss of buffer.

When most of your income is committed to fixed expenses, even a small unexpected cost can create a gap. A medical bill, a repair, or a delayed payment can disturb your entire monthly plan.

This is why many people feel financially stuck even after earning more. The income has increased, but the room for flexibility has reduced.

For instance, if your monthly commitments rise close to your income, even a ₹3,000 or ₹5,000 expense can feel difficult to manage without adjusting something else.

If you are facing frequent month-end gaps, it may not be your income. It is often how your expenses have adapted to it. Platforms like Pocketly can help manage urgent expenses without collateral commitments.

Where Lifestyle Inflation Goes Wrong

Understanding why expenses increase is only one part of the picture. The bigger issue is how these changes turn into long-term financial pressure when decisions are made without planning.

Lifestyle upgrades are not the problem on their own. The issue begins when multiple upgrades happen together without a clear plan. What feels like progress at first can quickly turn into fixed financial pressure.

Here are the patterns where things usually go wrong:

-

Upgrading multiple expenses at the same time: Rent, travel, and daily spending increase together, leaving very little room for flexibility.

-

Turning flexible spending into fixed commitments: What used to be optional becomes a monthly obligation that is harder to adjust later.

-

Relying on future income to justify current spending: Taking EMIs or using credit assumes your income will stay stable, which is not always predictable.

-

Ignoring how much financial buffer remains: Higher income creates a sense of comfort, but it often reduces your ability to handle unexpected expenses.

-

Not reviewing expenses after lifestyle changes: Without checking where your money goes, spending patterns continue unchecked.

Over time, these patterns create a cycle where expenses stay high, but your ability to respond to financial changes becomes limited.

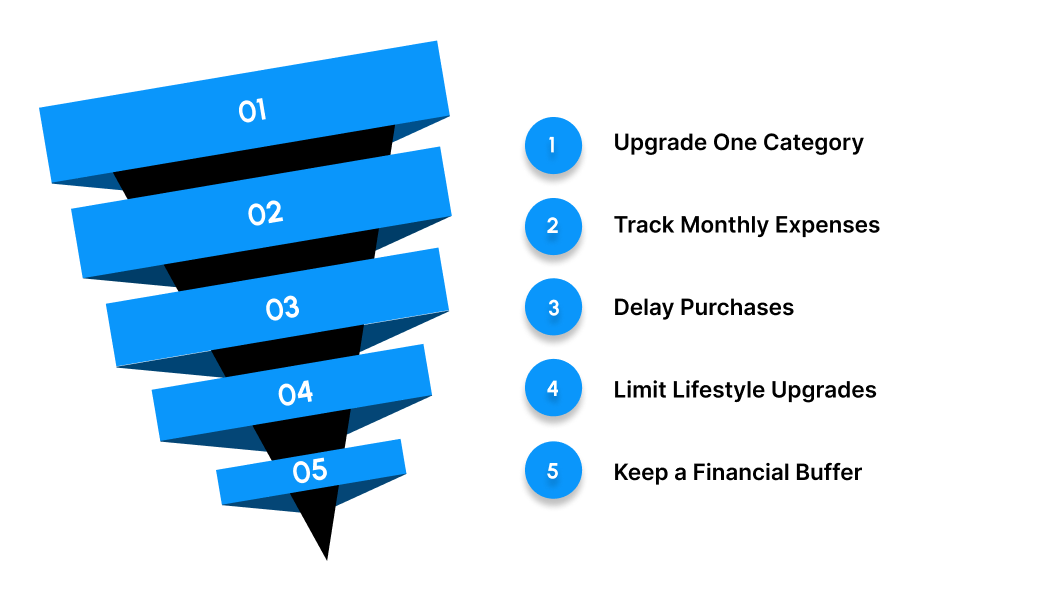

How to Control Lifestyle Inflation Without Feeling Restricted

Controlling lifestyle inflation does not mean cutting everything back. It means making deliberate choices about where your money should grow with your income, and where it should stay stable.

1. Upgrade One Expense Category at a Time

Instead of increasing spending across all areas, focus on one upgrade after a salary increase. You might move to a better apartment while keeping your dining and shopping habits unchanged for a while.

2. Track Recurring Expenses Every Month

Recurring costs often grow without attention. A quick monthly review can reveal subscriptions or services you no longer use but still pay for.

3. Delay Non-Essential Purchases

Giving yourself a short pause before buying helps reduce impulsive decisions. Many purchases feel less necessary after a couple of days.

4. Set a Limit for Lifestyle Upgrades After Every Raise

Not every increase in income needs to reflect in your spending. Deciding in advance how much of your raise goes toward lifestyle changes keeps your finances stable.

5. Protect a Fixed Financial Buffer

Keeping a small portion of your income untouched creates room for unexpected expenses. Without this buffer, even a minor cost can push you toward unnecessary borrowing.

A common mistake is relying on extra funds when they are not truly required, which increases financial pressure later. Maintaining a buffer helps you avoid that situation and keeps your finances stable.

Also Read: Applying for an Instant Personal Credit Line Online

When Cash Gaps Still Happen

Even with careful planning, not every financial gap comes from overspending. In many cases, it is simply a timing issue.

A salary may arrive late, a client payment may be delayed, or an unexpected expense may come up at the wrong time. The challenge here is not how much you earn or spend, but when your money is available.

The problem is that these short gaps can still disrupt your routine. Bills do not wait, and essential expenses cannot always be postponed. Without a buffer, even a small delay can create unnecessary stress or force quick financial decisions.

In such situations, what matters is having a reliable way to bridge the gap without turning it into a long-term burden. Short-term, structured options can help you manage immediate needs while keeping your overall finances stable.

Managing Short-Term Cash Gaps Without Long-Term Stress with Pocketly

When a short-term cash gap comes up, the goal is to handle it without adding long-term financial pressure. Unstructured options can solve the problem quickly, but often make repayment harder later.

Structured, short-term solutions designed for smaller amounts can help bridge this gap more predictably. Platforms like Pocketly, a digital lending platform, offer structured short-term options without collateral. All digital, no hidden charges, with 24/7 support.

Here's how Pocketly supports short-term cash needs in a more structured way:

-

Borrow only what fits your requirement: Loan amounts range from ₹1,000 to ₹25,000, which helps you take only what is needed for the situation instead of overcommitting.

-

No need for collateral or a guarantor: You can apply without pledging assets or involving another person, which keeps the process simple and accessible.

-

Quick verification and approval process: A digital KYC-based flow reduces waiting time and helps you get a decision without lengthy checks.

-

Direct bank transfer after approval: Once your request is approved, the amount is credited to your account, so you can manage urgent expenses without waiting.

-

Repayment that fits your monthly plan: Flexible options allow you to align repayments with your income cycle, so it does not disrupt your budget.

-

Clear and upfront cost structure: Interest starts from 2% per month, with processing fees between 1% and 8%, so you know the cost before making a decision.

-

Access anytime through the mobile app: You can apply, track, and manage everything digitally, which makes it easier to stay in control.

Check your eligibility on Pocketly in a few minutes and manage urgent needs like rent gaps, repairs, or medical expenses without long-term commitments.

How to Stay in Control Going Forward

Lifestyle inflation builds slowly through small decisions that feel justified at the time. Over time, these choices reduce your flexibility and make even small expenses harder to manage.

The key is to stay aware of how your spending evolves with your income. Making selective upgrades, tracking recurring costs, and maintaining a financial buffer can help you avoid unnecessary pressure.

When short-term gaps do appear, addressing them early with a clear plan can prevent them from turning into repeated financial stress. In situations where you need a small amount to manage an immediate expense, using a structured option like Pocketly can help you bridge the gap without disrupting your overall financial balance.

If you are dealing with a short-term expense, reviewing your options early and understanding the total cost can help you make a more confident decision. Download Pocketly on iOS or Android to access funds when you need them and stay in control of your finances.

FAQs

1. How do I know if lifestyle inflation is affecting me?

If your income has increased but your savings have not, and you still face month-end cash gaps, it is a strong sign that your expenses have adjusted to your income.

2. Can lifestyle inflation affect long-term financial goals?

Yes, higher recurring expenses reduce your ability to save consistently, which can delay goals like building an emergency fund or planning larger purchases.

3. Is it okay to upgrade my lifestyle after a salary increase?

Yes, but it works better when upgrades are gradual and planned. Increasing multiple expenses at once can reduce your financial flexibility.

4. Why do small expenses have such a big impact over time?

Individually, they feel manageable, but recurring costs add up every month and can take a significant portion of your income without clear visibility.

5. What should I do if lifestyle inflation has already increased my expenses?

Start by reviewing your recurring costs and identifying what can be reduced or paused. Even small adjustments can help restore balance in your monthly budget.

6. What is the safest way to handle a short-term cash gap without disrupting my finances?

Start by checking if the gap is due to timing or spending. If it is temporary, consider a structured short-term option with clear repayment terms, and always plan repayment before borrowing.