Managing money as a young Indian can feel like juggling too many balls at once. Tuition fees, month-end expenses, and unexpected bills often pile up faster than your savings, leaving you wondering how to get ahead.

It is frustrating when opportunities like investing in a course, buying your first property, or starting a side hustle feel just out of reach. Turning to high-interest credit can make things worse, adding stress instead of progress.

Debt does not have to be your enemy. When used smartly, it can fund opportunities, smooth cash flow, and help you grow wealth faster. In this blog, you will learn how to spot good debt, use it strategically, and leverage tools like Pocketly to manage short-term financial needs responsibly.

TL;DR

- Debt can be a tool, not a burden: Using loans strategically can help you invest in assets, education, or business opportunities that grow your wealth over time.

- Know good vs. bad debt: Good debt adds value or income, like mortgages or education loans; bad debt is for consumption and high-interest purchases.

- Practical strategies: Leverage education loans, property loans, small business loans, or short-term personal loans to grow income or acquire appreciating assets.

- Manage risk: Borrow only what you can repay, choose low-interest options, and avoid over-leveraging to protect your financial stability.

- Pocketly for short-term needs: Quick loans from ₹1,000–₹25,000 with instant approval help manage month-end or unexpected expenses without falling into high-interest debt.

Good Debt vs Bad Debt: How to Make Debt Work for You

Not all debt is created equal. Understanding the difference between good debt and bad debt is the first step to using borrowing as a tool to build wealth rather than a trap that drains your finances.

| Aspect | Good Debt | Bad Debt |

| Purpose | Borrowed to create value or generate income | Borrowed for items that depreciate or don’t add value |

| Examples | Student loans for professional courses, mortgages for rental property, and small business loans | Credit card debt for luxury items, payday loans, and high-interest personal loans |

| Financial Impact | Can increase net worth and future earnings | Drains savings and increases financial stress |

| Interest & Repayment | Often lower interest, manageable repayment | High interest, difficult to manage repayment |

| Outcome Over Time | Accelerates wealth creation | Limits financial freedom, increases debt burden |

| Strategy | Borrow strategically, for growth or income-generating purposes | Avoid impulsive borrowing for non-essential expenses |

Tip: Focus on good debt that builds wealth and supports your financial goals. Avoid bad debt that reduces your financial flexibility and adds stress.

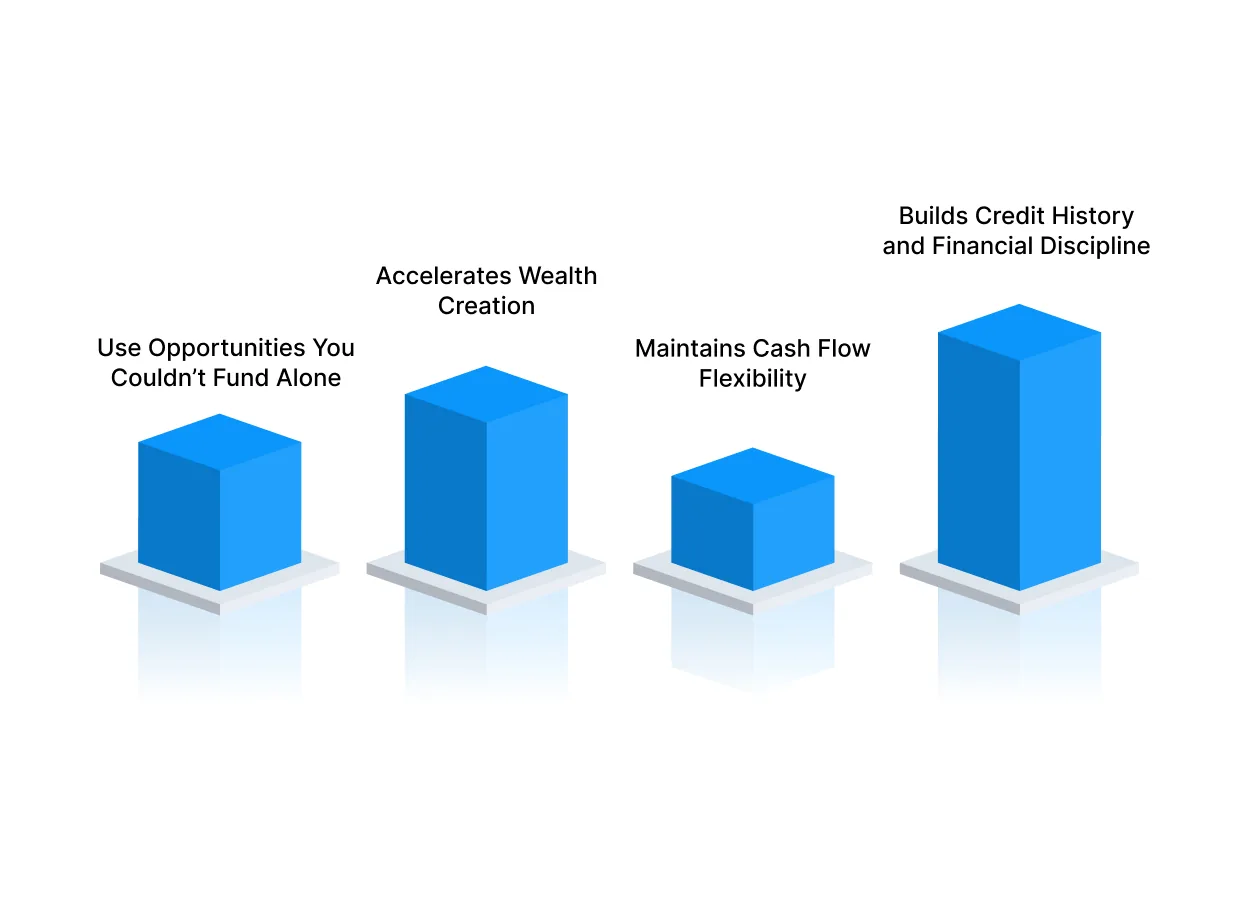

Why Using Debt Can Help You Build Wealth?

Debt often gets a bad reputation, but when used strategically, it can actually accelerate your path to financial growth. Here’s why:

Debt often gets a bad reputation, but when used strategically, it can actually accelerate your path to financial growth. Here’s why:

Use Opportunities You Couldn’t Fund Alone

Using debt lets you take advantage of opportunities that might be out of reach if you relied only on savings. By borrowing strategically, you can invest in education, property, or business ventures without waiting years to accumulate the full amount.

For instance, a student might take a low-interest loan to complete a professional certification that opens doors to higher-paying jobs. Similarly, a young professional could use a business loan to start a side hustle that generates extra income, turning borrowed money into a wealth-building asset.

Accelerates Wealth Creation

When the returns from borrowed money exceed the cost of debt, you can grow your wealth faster than by relying solely on savings. Debt allows you to multiply your investment potential and take calculated risks that produce long-term gains.

For example, taking a mortgage to buy a rental property can generate steady rental income while the property appreciates over time. This combination of cash flow and asset growth lets you build wealth more quickly than saving for years to buy the same property outright.

Maintains Cash Flow Flexibility

Debt can help you preserve your cash for emergencies or other investments. Instead of depleting your savings for a big purchase, responsible borrowing keeps funds available for other wealth-building activities.

For instance, a salaried professional might use a small personal loan to cover urgent expenses while continuing to invest in mutual funds or stocks. This approach ensures that short-term needs do not derail long-term financial plans.

Builds Credit History and Financial Discipline

Successfully managing debt improves your credit profile, which can lead to better borrowing opportunities in the future. Regular repayments also instil financial discipline and responsible money management habits.

For example, a young borrower who repays a student loan on time strengthens their credit score. Later, this can help them secure a mortgage with favourable interest rates, enabling larger investments and faster wealth accumulation.

Also Read: Simple Money Management Tips for Personal Finances

How to Use Debt to Build Wealth Smartly?

Using debt to grow wealth requires planning, strategy, and discipline. Here are practical ways young Indians can leverage borrowing to build financial security and accelerate growth:

1. Consolidate High-Interest Debt

Carrying multiple high-interest debts can silently drain your finances and limit your ability to invest or save. Consolidating these into a single, lower-interest loan reduces repayment stress while freeing up cash for wealth-building opportunities.

For example, a young professional might use a personal loan at a lower interest rate to pay off multiple credit card balances, keeping monthly repayments manageable while redirecting savings into investments.

Core Habit: Replace inefficient debt with lower-cost borrowing to improve financial flexibility and reduce unnecessary interest payments.

2. Make Your Money Work Harder for You

Efficient cash flow management prevents unnecessary borrowing and reduces financial pressure. Small adjustments, like paying loans more frequently or timing payments to maximise interest-free periods, can free up cash for strategic investments.

For instance, a salaried professional might direct their salary into an offset account against a home loan, reducing interest costs while keeping funds accessible for emergencies or investment opportunities.

Core Habit: Track and manage payments to reduce costs and maintain financial stability.

3. Borrow to Invest in Assets or Skills

Debt can fund opportunities that increase your earning potential or generate long-term income. The key is to borrow for investments that grow in value rather than for short-term consumption.

For example, a student taking a loan to complete a professional certification in digital marketing can immediately access higher-paying projects, turning the borrowed amount into an investment in future income.

Core Habit: Borrow strategically to invest in income-generating assets or skills that enhance your long-term financial potential.

4. Use Windfalls to Strengthen Your Finances

Unexpected funds, such as bonuses or gifts, are opportunities to accelerate wealth creation. Using these amounts to pay off high-interest debt or invest in appreciating assets ensures that windfalls contribute to growth rather than short-term spending.

For example, a young professional receiving a bonus might clear a high-interest credit card and then use the remaining funds to invest in a managed mutual fund, combining debt reduction with asset growth.

Core Habit: Direct windfalls toward reducing bad debt or building wealth to maximise long-term financial impact.

5. Practice Debt Recycling

Debt recycling transforms existing obligations into tools for wealth creation. By using the equity built up in assets like a home loan to invest in income-generating assets, debt becomes productive rather than a burden.

For instance, as a home loan is paid down, a borrower could redraw equity to invest in shares, earning returns that help pay off the loan faster while benefiting from potential capital appreciation.

Core Habit: Convert existing debt into income-generating opportunities to accelerate wealth creation.

6. Access Professional Use for Investments

Professionally managed geared funds allow investors to utilise borrowing at wholesale rates without taking personal loans. This approach amplifies potential returns while managing risk with professional oversight.

For example, a young investor might put money into a managed share fund that uses leverage internally, allowing exposure to higher-value investments without the complexity of arranging a personal margin loan.

Core Habit: Use professionally managed investments to grow wealth safely and efficiently.

Key Tip: Only borrow amounts you can repay comfortably. Focus on debt that creates income, builds assets, or improves skills rather than funding short-term consumption.

Also Read: How to Manage Monthly Expenses Smartly in 2025

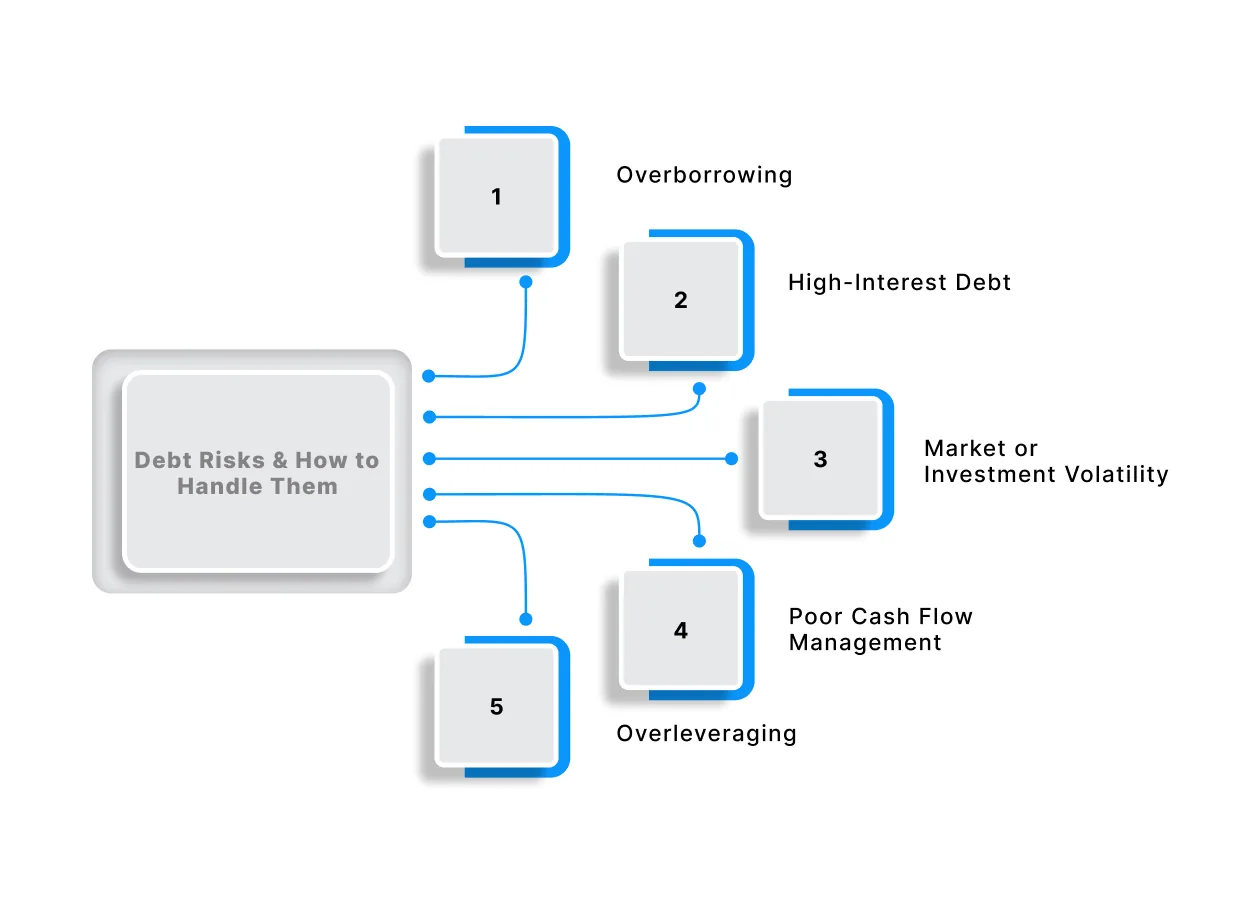

Debt Risks You Need to Know and How to Handle Them

Debt can be a powerful tool for building wealth, but it comes with potential pitfalls that can derail your financial growth if not managed carefully. Understanding these risks and knowing how to mitigate them is crucial to using debt effectively.

Debt can be a powerful tool for building wealth, but it comes with potential pitfalls that can derail your financial growth if not managed carefully. Understanding these risks and knowing how to mitigate them is crucial to using debt effectively.

Risk 1: Overborrowing

Taking on more debt than you can realistically repay can lead to missed payments, rising interest costs, and stress that affects both your finances and peace of mind.

Mitigation: Only borrow amounts that fit comfortably within your monthly budget. Before taking a loan, calculate your repayment capacity and maintain an emergency fund to cover unexpected shortfalls.

Risk 2: High-Interest Debt

Borrowing from expensive sources like credit cards or payday loans can quickly offset any benefits of using debt strategically. The cost of borrowing may end up exceeding the returns from your investment.

Mitigation: Opt for low-interest loans or platforms with transparent pricing, like Pocketly, which offers small, short-term loans with clear interest rates and flexible repayment terms.

Risk 3: Market or Investment Volatility

Debt used for investments is only effective if the returns exceed the cost of borrowing. A market downturn or underperforming asset can turn a promising strategy into a financial setback.

Mitigation: Diversify your investments and focus on low-to-moderate risk assets, such as rental property, government-backed schemes, or stable mutual funds. Use debt judiciously, avoiding high-leverage speculation unless you fully understand the risks.

Risk 4: Poor Cash Flow Management

Even small loans can become burdensome if you do not track your spending or have multiple repayment obligations. Overlapping loans may leave you short on cash for essentials.

Mitigation: Maintain a clear repayment plan and monitor all your obligations. Prioritise loans strategically, and avoid borrowing beyond your capacity to service debt without affecting daily expenses.

Risk 5: Overleveraging

Relying too heavily on debt amplifies both gains and losses. If your assets do not generate expected returns, you could face a financial crunch.

Mitigation: Limit total debt relative to your income or assets. Review your financial position regularly, adjust borrowing limits, and ensure each loan serves a purpose aligned with your long-term wealth-building goals.

When Not to Use Debt?

Not all debt helps you build wealth; borrowing without a clear purpose or plan can lead to financial stress. Avoid taking debt in the following situations:

- For Non-Essential Spending: Borrowing for luxury items, vacations, or lifestyle indulgences that don’t generate income or appreciation.

- To Cover Recurring Expenses: Using debt to pay everyday bills or monthly living costs instead of budgeting properly can trap you in a cycle of borrowing.

- Multiple Unmanaged Loans: Holding several loans at once without a repayment plan can strain your cash flow and increase default risk.

- Without a Repayment Strategy: Borrowing without the ability to repay on time can result in penalties, higher interest, and damage to your credit profile.

- Speculative Investments Beyond Your Knowledge: Avoid using debt for high-risk investments or trading unless you fully understand the risks and can afford potential losses.

Using debt wisely means only borrowing when it’s likely to generate value or improve your financial situation

How Pocketly Can Help You Use Debt Wisely

Even with careful planning, unexpected expenses can pop up, such as medical emergencies, urgent repairs, or sudden fees, which can disrupt your financial growth plans. Having a reliable, flexible solution helps you manage these short-term needs without derailing your long-term wealth-building strategy.

Pocketly provides that support. As a digital lending platform, we offer quick access to funds for students, salaried professionals, and self-employed individuals, making it easier to bridge financial gaps responsibly and keep your plans on track.

- Quick and Flexible Loans: Borrow amounts from ₹1,000 to ₹25,000, ideal for handling unforeseen expenses or investment opportunities.

- Affordable Rates: Interest starts at 2% per month, with transparent processing fees from 1–8%, so you know exactly what you’re paying.

- Fully Digital Process: No paperwork, no long waits. Complete your KYC online and get funds directly into your account.

- Flexible Repayment Options: Pick the repayment plan that fits your cash flow—either in full or via EMIs, depending on your convenience.

How to Apply for a Pocketly Loan:

1. Download: Get the Pocketly app from Google Play or Apple App Store.

2. KYC: Complete the simple online KYC with basic personal details.

3. Choose: Select the loan amount you need (up to ₹25,000).

4. Disbursal: Funds are instantly transferred to your bank account once approved.

Conclusion

Using debt wisely isn’t just about borrowing money; it’s about cultivating a mindset that leverages financial tools to create opportunities and build long-term wealth. By understanding the difference between good and bad debt, prioritising investments that generate returns, and managing repayment responsibly, you set the stage for sustainable financial growth.

True wealth isn’t built by avoiding debt entirely, but by using it strategically to fund education, grow a business, or acquire appreciating assets. When approached thoughtfully, debt becomes a tool that accelerates progress rather than a source of stress.

Unexpected expenses and month-end cash crunches are part of life, but with careful planning and smart borrowing, you can manage them without derailing your financial journey.

Ready to maintain control of your finances even during tight weeks? Download the Pocketly app today on Android or iOS and access quick, transparent loans to manage urgent expenses and stay on track toward your financial goals.

FAQs

1. Can students or young professionals use debt to build wealth?

Yes. Borrowing strategically for education, professional certifications, or income-generating opportunities can increase earning potential and build long-term wealth when managed responsibly.

2. What is considered good debt for beginners?

Good debt is money borrowed to acquire assets or skills that appreciate in value or generate income, such as education loans, business loans, or home mortgages.

3. How can Pocketly help manage short-term cash flow?

Pocketly provides small, fast personal loans (₹1,000–₹25,000) with minimal documentation and quick approval, helping users cover urgent expenses without resorting to high-interest debt.

4. Is it risky to borrow for investments or education?

Any borrowing carries risk, but careful planning, assessing repayment capacity, and choosing low-interest debt can minimise risks and make it a tool for wealth creation.

5. How do interest rates impact wealth-building loans?

Lower interest rates reduce borrowing costs, making it easier for the return on investment (like higher income or asset appreciation) to exceed the cost of debt, thus building wealth faster.