For students, salaried professionals, and entrepreneurs in India, managing multiple loans can be a complex task. With the pressure of monthly repayments and unexpected financial challenges, many find themselves juggling both a car loan vs a home loan. The dilemma often arises: Which loan should you prioritise paying off first? Should you focus on the smaller car loan to reduce monthly obligations, or target the larger home loan for long-term financial freedom?

Factors like interest rates, loan tenure, and your current financial circumstances are key when making this decision. This blog will explore how understanding these elements can help you choose the best option that suits your financial objectives.

Key Takeaways

- Amortized Loans: Loans have fixed repayment terms that cover both principal and interest, offering a clear path to becoming debt-free.

- Car vs. Home Loans: Car loans have higher interest rates (8.50% to 12.65%) and are secured by the vehicle, while home loans have lower rates (7.70% to 8.75%).

- Repayment Strategy: Prioritize paying off car loans first due to higher interest and depreciation, while home loans provide long-term tax benefits.

- Improved Cash Flow: Paying off car loans can free up cash flow quickly and provide motivation through the Debt Snowball Effect.

How do Loans Work?

Loans provide a way to borrow money for purchasing assets or covering expenses, with the understanding that the borrowed amount (principal) will be repaid along with interest over a set period.

Unlike credit card debt, where you can choose to pay the minimum or the total amount, loans are amortized. This means they have fixed repayment terms with structured payments that gradually cover both principal and interest.

Both car loans and home loans follow this amortization structure, ensuring borrowers have a clear timeline to become debt-free.

Understanding Car Loan

Car loans in India are structured as secured loans, with the vehicle itself serving as collateral. Interest rates vary from 8.50% to 12.65% annually, driven by factors like your credit score, the length of the loan term, and the vehicle type.

For instance, ICICI Bank offers rates starting at 9.10% p.a. onwards, while Bank of Baroda has floating interest rates. Defaulting on a car loan can impact your credit score and repossession of the vehicle.

Understanding Home Loan

Home loans in India offer longer loan repayment modes, ranging from 10 to 30 years, and interest rates that are often lower than those for other loans. Interest rates generally range from 7.70% to 8.75% annually, depending on the lender and the borrower's creditworthiness.

For instance, as of July 2025, the State Bank of India offers home loan interest rates starting at 7.50% per annum, while ICICI Bank's rates begin at 7.70% per annum. These rates are subject to change based on factors such as the applicant's credit score and the prevailing market conditions.

While traditional car and home loans can come with high-interest rates and lengthy approval processes, Pocketly offers an alternative that simplifies borrowing. You can access personal loans ranging from ₹1,000 to ₹25,000

Key Considerations for Car vs. Home Loan Repayment

Car loans vs home loans serve distinct purposes and come with their own sets of advantages and considerations. Car loans offer quicker access to vehicles with shorter tenures, while home loans provide long-term financing for property acquisition with potential tax benefits.

Let’s explore the key considerations. It’s important to evaluate your financial situation, loan eligibility, and long-term objectives before choosing which loan best fits your needs.

| Feature | Car Loan | Home Loan |

| Collateral | The vehicle itself serves as collateral. | The property being purchased or constructed serves as collateral. |

| Loan Amount | Ranges from ₹1 lakh to ₹1 crore, depending on the vehicle's value and eligibility. | Can range from ₹5 lakh to ₹10 crore or more, based on property value and eligibility. |

| Interest Rates | 8.50% to 12.65% per annum. | 7.70% to 8.75% |

| Loan Tenure | 1 to 7 years. | 10 to 30 years. |

| Tax Benefits | No direct tax benefits. | Section 80C (principal repayment) and Section 24(b) (interest paid) of the Income Tax Act. |

| Processing Fees | Generally lower; varies by lender. | Can be higher; varies by lender. |

| EMI Structure | Fixed or floating rates; prepayment options available. | Fixed or floating rates; prepayment options available. |

| Default Consequences | Repossession of the vehicle; impact on credit score. | Foreclosure of the property; impact on credit score. |

Also Read: Overdue Payment in Loan: Meaning, Consequences, and How to Clear It

Now that you have a clear understanding of the key features of both car loans vs home loans, the next step is to determine how to manage their repayment. The timing and strategy for prioritizing repayment can affect your financial health.

Car Loan vs Home Loan: How to Prioritize Your Loan Repayments

When managing multiple loans, the decision between prioritizing car loan or home loan repayments requires careful consideration of several financial factors that can significantly impact your long-term wealth and cash flow. Here's how to approach prioritizing your car and home loan repayments:

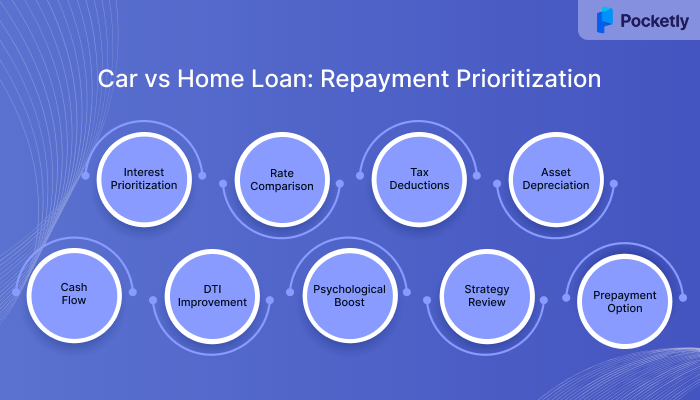

- Debt Avalanche Method: Prioritize paying off loans with the highest interest rates first. Car loans have higher interest rates than home loans, making them a priority for extra payments.

- Interest Rate Comparison: As of July 2025, car loan interest rates range from 8.50% to 12.65%, while home loan rates range from 7.70% to 8.75%. Prioritizing car loan repayment can save you money on interest over time.

- Tax Benefits: Home loans offer significant tax deductions under Sections 80C (principal repayment) and 24(b) (interest payments), while car loans offer limited tax benefits, mostly for business use.

- Asset Depreciation: Cars depreciate quickly (10-30% in the first year), making it more financially beneficial to pay off car loans first. Homes appreciate in value over time, making home loan repayments less urgent.

- Cash Flow Considerations: Car loans have shorter tenures (3-7 years) compared to home loans (15-30 years). Paying off the car loan first will free up monthly cash flow sooner, providing more flexibility for other financial goals.

- Improved Debt-to-Income Ratio: Paying off the car loan improves your debt-to-income (DTI) ratio, which is crucial for future borrowing and maintaining a healthy financial status.

- Psychological Benefits: The Debt Snowball Effect suggests that paying off the smaller car loan balance first can provide motivation and momentum for continued debt reduction.

- Regular Review: The optimal repayment strategy depends on your individual financial situation, risk tolerance, and goals. It's important to reassess and adjust your plan as per circumstances.

- Partial Prepayments: For borrowers with surplus funds, making partial prepayments on the car loan can save interest while maintaining liquidity.

If you’re looking for more financial flexibility and quick access to funds, Pocketly could be a great option with interest rates starting as low as 2% per month.

What are the Benefits of Paying Off Your Car Loan First?

Paying off your car loan ahead of schedule can provide you with multiple financial advantages. By eliminating your car loan early, you can save on interest, improve your creditworthiness, and free up funds for other financial goals.

Here’s a breakdown of the key benefits of paying off your car loan first:

- Save on Interest: Paying off the loan early reduces the principal, saving you money on accumulated interest, especially in loans with simple interest structures.

- Improve Debt-to-Income Ratio: By eliminating monthly loan payments, your debt-to-income ratio improves, which can help with future loan approvals.

- Free Up Monthly Cash Flow: Without the car payment, you can allocate funds to other financial priorities like savings, investments, or debt reduction.

- Avoid Negative Equity: Paying off your car loan early lowers the risk of owing more than your car’s value, which can be problematic in case of accidents or selling the vehicle.

- Lower Insurance Premiums: Once the loan is paid off, you may have the option to reduce coverage or adjust your policy, potentially lowering insurance costs.

While prioritising loan repayment is crucial, there's another strategy that can help reduce your interest burden across all loans: refinancing.

How to Refinance a Car Loan or Home Loan to Save on Interest?

Refinancing your car or home loan can lower interest rates and reduce your monthly payments. It allows you to pay off your existing loan with a new one that offers better terms, potentially saving you money over the life of the loan. Here’s how you can refinance effectively to save on interest:

- Evaluate Your Current Loan: Review the existing loan's interest rate, balance, and terms to determine if refinancing will lead to savings.

- Credit Score: A better score will help you to secure a more favorable interest rate.

- Compare Lenders: Shop around to compare refinancing offers from different banks or financial institutions.

- Consider Loan Tenure: Decide whether to shorten or extend the loan term to lower your monthly payment or interest cost.

- Understand the Costs: Be aware of any fees, such as processing or prepayment charges, that may apply when refinancing.

- Apply for Refinancing: Provide the necessary documents like income proof, KYC, and property/vehicle details.

Sometimes, even with the best repayment and refinancing strategies, you might need additional financial flexibility to manage your loan obligations effectively. This is where alternative financial tools can provide support.

Pocketly: A Smart Financial Tool for Managing Loan Repayments

When juggling multiple loans, having quick access to additional funds can provide the flexibility needed to manage repayments effectively. Pocketly offers small, short-term loans to help manage unexpected expenses or ease the repayment burden on your existing loans, while staying on track with your repayment goals.

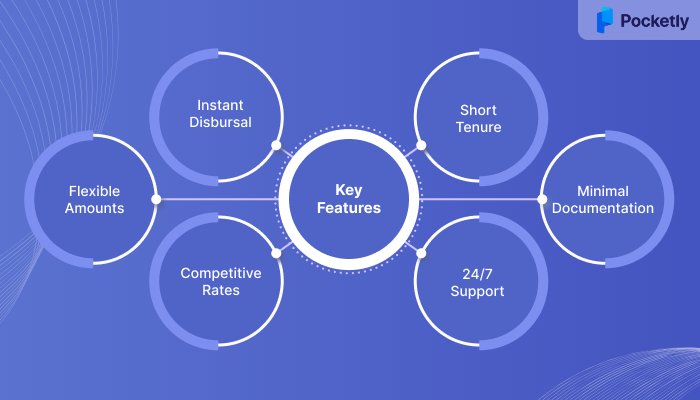

Key Features of Pocketly

- Instant Loan Disbursal: Apply and receive funds directly in your bank account within minutes.

- Flexible Loan Amounts: Borrow between ₹1000 and ₹25,000, catering to various financial needs.

- Competitive Interest Rates: Enjoy interest rates starting from 2% per month, offering affordable borrowing options.

- Short Tenure Options: Choose flexible repayment periods or partial repayments and loan closure at any time.

- Minimal Documentation: Experience a hassle-free application process with minimal KYC requirements.

- 24/7 Customer Support: Access dedicated assistance anytime to address your queries and concerns.

Conclusion

Handling loans requires a well-thought-out plan to maintain financial stability and reduce interest costs in the long run. Now that you understand the features and differences between car loans vs home loans, you can make decisions about which loan to prioritise. Whether you use the debt avalanche method to focus on higher-interest loans or choose a strategy that aligns with your financial goals, staying proactive about repayment is essential.

If you’re looking for a simple way to handle short-term borrowing, Pocketly is here to help. Download Pocketly on Android or iOS to skip the paperwork and manage your borrowing with clarity.

FAQ’s

1. What happens if you pay off a car loan early?

Paying off a car loan early can save you money on interest, especially if your loan uses simple interest. However, some lenders may impose prepayment penalties, so it's essential to review your loan agreement. Additionally, while paying off the loan reduces your debt, it might slightly lower your credit score temporarily due to changes in your credit mix.

2. Does paying for a car loan or home loan increase your credit score?

Making timely payments on both car and home loans can impact your credit score by demonstrating responsible credit behavior. However, the effect on your score can vary based on your credit profile and the types of credit you have.

3. Is it better to save money or pay off a loan?

The decision depends on your financial situation. If your loan has a high interest rate, paying it off may be beneficial. However, it's also crucial to maintain an emergency fund to cover unexpected expenses. Balancing both saving and paying off debt is often the most prudent approach.

4. What are the consequences of missing a loan repayment?

Missing a loan repayment can lead to late fees and may affect your credit score negatively. Prolonged non-payment can result in the loan defaulting, leading to more severe consequences like debt collection actions and potential legal issues.

5. Is there a difference between a loan and a debt?

A loan is a specific type of debt where a lender provides money to a borrower with the expectation of repayment under agreed terms. Debt, in a broader sense, refers to any amount of money borrowed that needs to be repaid, including loans, credit card balances, and other financial obligations.