As an entrepreneur, managing finances can quickly become overwhelming. With so many expenses to track, decisions to make, and cash flow challenges, it’s easy to lose sight of your financial health. Without the right financial knowledge, you might find yourself stuck in a cycle of stress, constantly worrying about whether your business will survive or grow.

The impact of poor financial management is not just theoretical; it can lead to missed opportunities, financial strain, or even business failure. Many entrepreneurs, especially in the early stages, lack the financial literacy needed to make smart, sustainable decisions.

But here's the solution: Financial literacy doesn’t require you to be a number-crunching expert; it’s about understanding key concepts that directly impact your business. With the right knowledge, you can take control of your finances, make better decisions, and discover opportunities for growth.

In this blog, we’ll walk you through the essential financial skills every entrepreneur needs to succeed, helping you set your business up for long-term financial stability.

TL;DR

- Financial literacy is crucial for business success, enabling better decision-making and sustainable growth.

- Key concepts include managing cash flow, budgeting, and understanding financial statements.

- Setting clear financial goals and regularly tracking expenses is essential for staying on top of finances.

- Common mistakes include mixing personal and business finances and lacking proper financial planning.

- Regular review of financials ensures you stay agile, reduce risks, and adapt to changing market conditions.

What Financial Literacy Means for Entrepreneurs?

Financial literacy for entrepreneurs involves the ability to interpret and use financial data effectively to make informed decisions. Here’s what it empowers entrepreneurs to do:

- Manage Cash Flow

- Assess Business Health

- Make Smart Investment Decisions

- Set Realistic Budgets

- Plan for Growth

This knowledge is essential for driving business success and ensuring long-term stability.

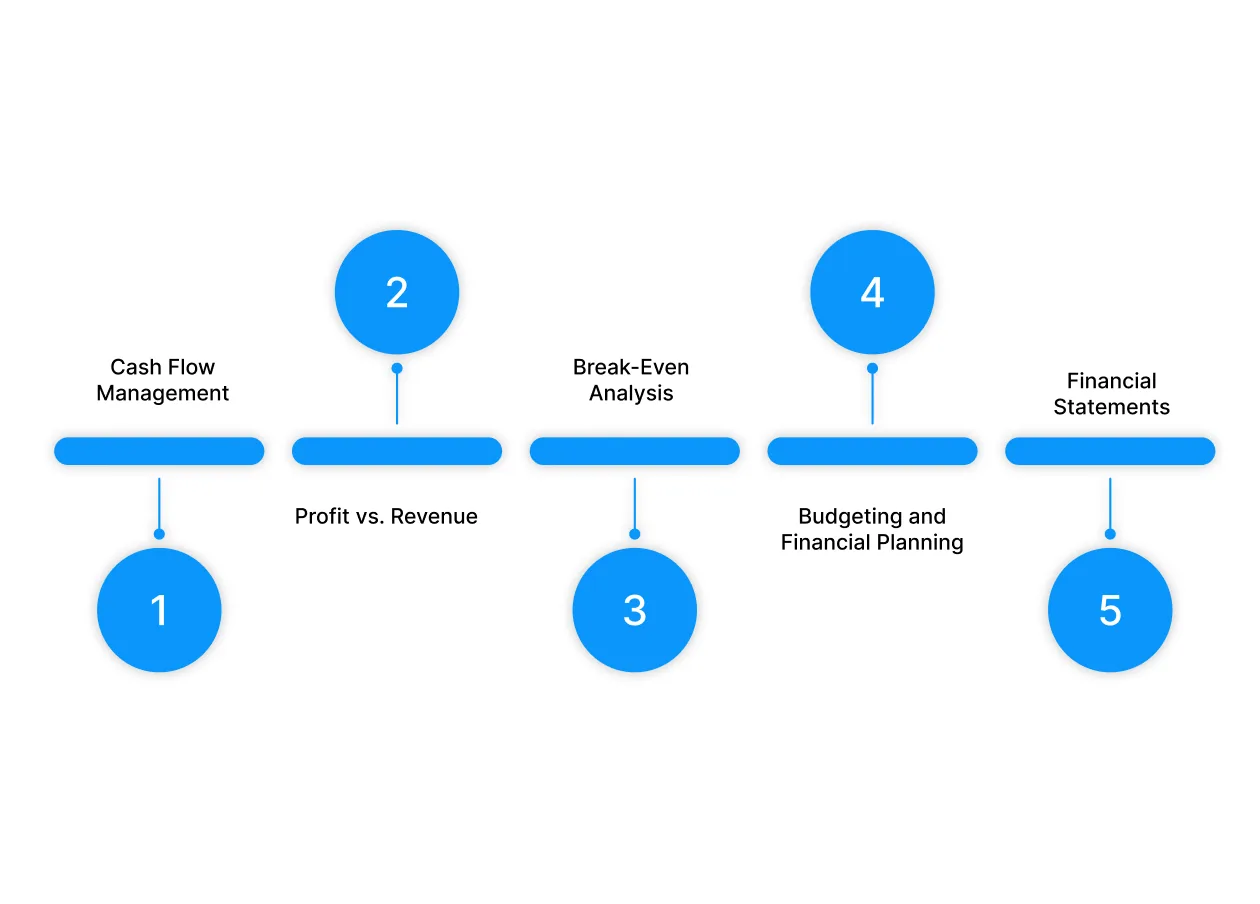

Key Financial Concepts Every Entrepreneur Should Master

As an entrepreneur, mastering key financial concepts is crucial for making informed decisions that can drive the success and growth of your business. Below are the essential financial concepts you need to understand:

As an entrepreneur, mastering key financial concepts is crucial for making informed decisions that can drive the success and growth of your business. Below are the essential financial concepts you need to understand:

1. Cash Flow Management

Cash flow is linked to the movement of money in and out of your business. Positive cash flow makes sure that you can cover expenses, invest in growth, and avoid financial strain. Without good cash flow management, even profitable businesses can struggle.

Example: If your business generates ₹100,000 in sales but has ₹90,000 in expenses, your cash flow is ₹10,000. However, if your customers take 60 days to pay, and you have bills due in 30 days, you might face cash flow issues despite being profitable.

2. Profit vs. Revenue

Revenue is the total amount of money generated from sales or services, while profit is what remains after all expenses are deducted. It's essential to know the difference because many entrepreneurs confuse revenue with profit, leading to unrealistic expectations.

Example: If your business generates ₹500,000 in revenue but incurs ₹400,000 in costs, your profit is ₹100,000, not ₹500,000. This distinction helps you make better pricing and cost-control decisions.

3. Break-Even Analysis

The break-even point is the level of sales at which your revenue covers your costs, and you’re neither making a profit nor a loss. It helps you figure out how much you need to sell to pay for fixed and variable costs, allowing for better pricing and sales targets.

Example: If your fixed costs (e.g., rent, salaries) are ₹50,000 per month and your product has a profit margin of ₹5,000 per unit, you’ll need to sell 10 units per month to cover your costs and break even. Anything beyond that is profit.

4. Budgeting and Financial Planning

Budgeting means creating a financial plan that allocates funds to various aspects of your business, such as operations, marketing, and salaries. Financial planning helps you avoid overspending, ensure liquidity, and strategically invest for growth.

Example: If you allocate ₹20,000 per month for marketing, ₹10,000 for salaries, and ₹5,000 for software subscriptions, budgeting ensures that your total expenses don’t exceed your income. Regularly reviewing your budget helps you adapt to changing circumstances.

5. Financial Statements

Financial statements, such as the balance sheet, income statement, and cash flow statement,t are essential for understanding your business’s financial health. These statements provide critical insights into your assets, liabilities, revenue, and profitability.

Example: A balance sheet shows your business’s assets, like cash and equipment, and liabilities, like loans. An income statement shows your profits or losses over a period, and the cash flow statement records the movement of cash, showing how much cash is available for operations.

By mastering these financial concepts, you gain the confidence and tools necessary to guide your business toward sustainable growth and profitability.

A Step-by-Step Financial Framework for Entrepreneurs

Creating a solid financial basis is essential for every entrepreneur. Follow these steps to ensure you're managing your business finances effectively and building a sustainable, profitable business.

Step 1: Set Clear Financial Goals

Establishing clear financial goals helps you define your business's direction. Whether your goal is to increase revenue, reduce costs, or become profitable within a specific timeframe, setting these objectives provides focus and a clear path forward.

For example, set a specific target such as "increase revenue by 20% in the next year" or "reduce overhead costs by 10% in six months." These measurable goals will guide decision-making and keep you accountable.

Step 2: Build a Realistic Budget

A well-thought-out budget is key to allocating resources effectively. Ensure that your budget accounts for both fixed and variable expenses, such as rent, salaries, raw materials, and marketing costs. Regularly review and alter your budget to reflect any changes in your company operations or market conditions.

For example, if you're planning a new marketing campaign, include all expected costs ads, content creation, tools, and resources and ensure the projected return justifies the investment. Regularly revisit your budget as expenses fluctuate.

Step 3: Monitor Cash Flow Regularly

Creating a positive cash flow is essential for business survival. Track your cash flow consistently, whether weekly or monthly, to ensure that the money coming in is enough to cover your expenses. Use accounting software to gain real-time insights into your financial standing.

For example, if your cash flow shows a consistent deficit, you might need to adjust your pricing strategy, reduce costs, or speed up the collection of accounts receivable. Regular cash flow checks will help you address these issues early.

Step 4: Review Financial Statements Monthly

Monthly reviews of your income statement, balance sheet, and cash flow statement offer a snapshot of your financial health. These documents allow you to see if you're on track to meet your goals and can highlight potential issues before they become problems.

For example, if you notice a decrease in profit margins over consecutive months, review your operating expenses to identify areas for cost-cutting or evaluate whether your pricing needs adjustment. Regularly assessing your financial statements will help keep your business aligned with its goals.

Step 5: Plan for Future Growth and Emergencies

Prepare for future expansion and unforeseen circumstances. Set aside a reserve fund for emergencies, and use projections to identify the best times to reinvest in your business for growth. Having a plan for both opportunities and risks helps maintain stability and flexibility.

For example, allocate a percentage of your profits to a savings fund dedicated to unforeseen expenses or economic slowdowns. This fund can act as a buffer during slow months, preventing you from having to take on debt or cut essential services.

Also Learn: Understanding the Ideal CIBIL Score Range for Personal Loan Applications

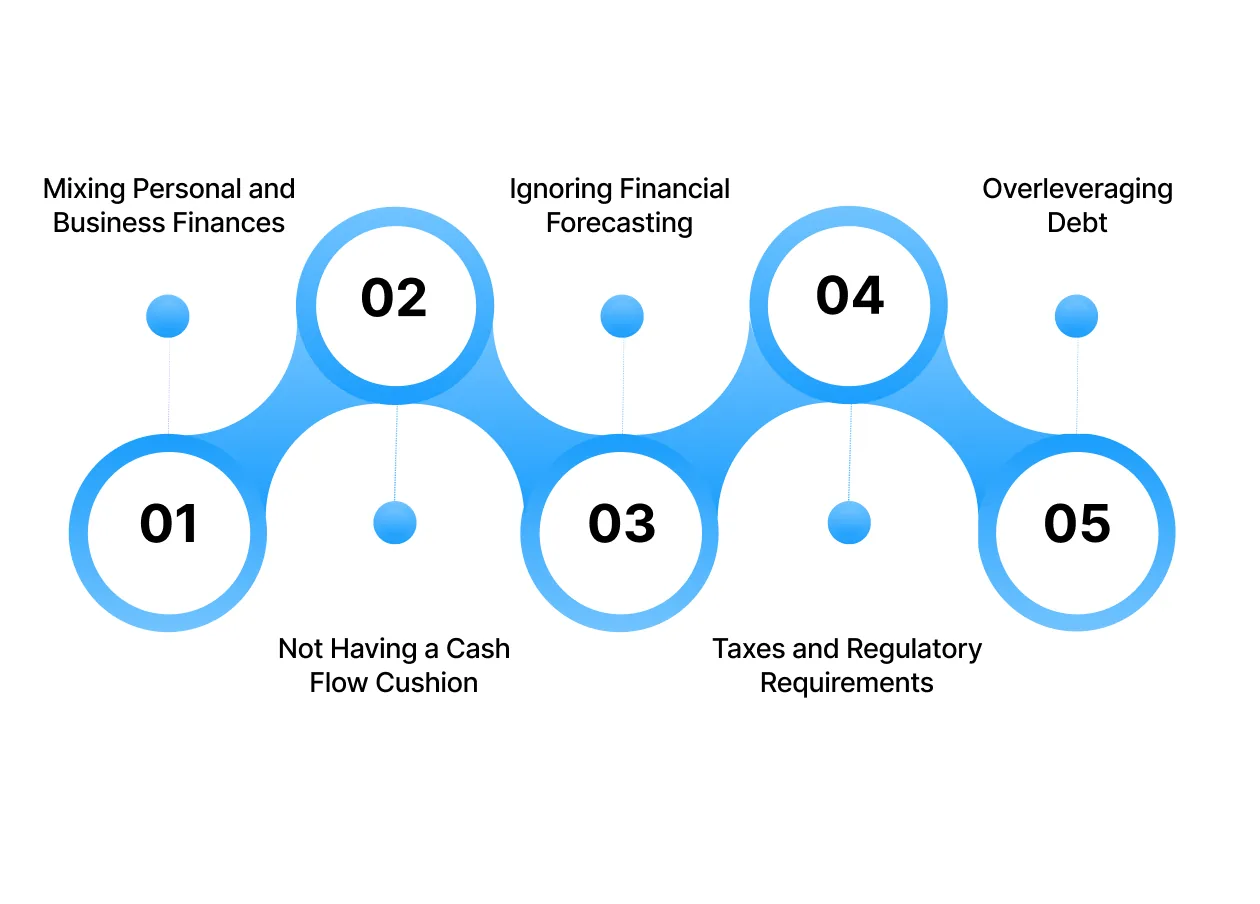

Common Financial Blunders Entrepreneurs Make and How to Avoid Them

Many entrepreneurs make financial missteps that can jeopardise their business’s growth. Understanding these mistakes and how to avoid them can help you keep your business on track. Here are some of the most common financial errors and strategies to mitigate their impact.

Many entrepreneurs make financial missteps that can jeopardise their business’s growth. Understanding these mistakes and how to avoid them can help you keep your business on track. Here are some of the most common financial errors and strategies to mitigate their impact.

1. Mixing Personal and Business Finances

Keeping your personal and business finances separate is crucial for maintaining clarity in your business’s financial health. Blurring these lines can lead to confusion, mismanagement, and difficulty in tracking expenses.

How to Avoid: Open a separate business account for all your transactions. This makes it easier to track business spending, prepare for taxes, and understand your financial position clearly.

2. Not Having a Cash Flow Cushion

Many entrepreneurs underestimate the importance of a cash reserve and find themselves in trouble when unexpected costs arise or when cash flow slows down.

How to Avoid: Set aside a portion of your profits into a dedicated emergency fund that covers 3-6 months of operating expenses. This will provide the financial cushion needed to manage lean periods without resorting to loans.

3. Ignoring Financial Forecasting

Failing to plan for future income and expenses can lead to missed possibilities and financial strain. Without forecasting, it becomes difficult to anticipate cash flow gaps or necessary investments.

How to Avoid: Develop regular financial forecasts and projections based on realistic assumptions. Use tools and software to model various scenarios and ensure you’re prepared for different business cycles.

4. Overlooking Taxes and Regulatory Requirements

Entrepreneurs often overlook their tax obligations or mismanage them, leading to penalties and unanticipated financial strain. Not staying compliant can harm both the business and your personal finances.

How to Avoid: Consult a tax professional regularly and keep track of your tax liabilities throughout the year. Set aside a chunk of revenue for taxes to avoid last-minute scrambling.

5. Overleveraging Debt

While debt can be a useful tool for business growth, overreliance on loans and credit can create long-term financial instability, especially if cash flow becomes inconsistent.

How to Avoid: Use debt strategically, ensure you can comfortably cover monthly repayments with your business’s cash flow. Focus on building a solid revenue base before seeking loans, and avoid taking on debt for non-essential expenses.

By recognising these common financial mistakes and taking proactive steps, entrepreneurs can build a more resilient business and avoid costly pitfalls.

Also Learn: Applying for Instant ₹5000 Personal Loan Online for Urgent Needs

Framework for Measuring Financial Literacy Progress for Entrepreneurs

Building financial literacy is a gradual process, and it’s crucial to track your growth to ensure you're managing your business finances effectively. Here’s a framework to help you measure your financial literacy growth:

1. Financial Forecasting Accuracy

Regularly compare your financial forecasts with actual outcomes. If you can predict your revenue, costs, and profits with high accuracy, it demonstrates strong financial literacy.

Key Action:

- Compare projected vs. actual numbers on a monthly or quarterly basis.

- Look for discrepancies, especially in areas like cash flow, profits, and growth.

Outcome:

- Accurate forecasting indicates that you understand key business metrics and are able to make realistic projections for the future.

2. Confidence in Financial Decision-Making

Track your decision-making process and confidence level in financial choices such as budgeting, pricing, and investment. If you're consistently making sound decisions without seeking external advice, your financial literacy is improving.

Key Action:

- Reflect on your comfort with decisions related to financial goals, loans, investments, and cost management.

- Record key decisions and assess whether they were based on sound financial analysis.

Outcome:

- Increased confidence shows that you're using financial knowledge to make decisions that align with your business goals.

3. Mastery of Financial Statements

Being able to interpret and analyse financial statements is a key indicator of financial literacy. If you can evaluate your balance sheet, income statement, and cash flow to assess business health, you’re progressing well.

Key Action:

- Review your financial statements monthly and analyse areas like profit margins, liabilities, and working capital.

- Use these insights to adjust business strategies accordingly.

Outcome:

- A strong understanding of financial statements shows that you’re prepared to assess the financial health of your business at any given moment.

4. Effective Cash Flow Management

Track your ability to manage cash flow—keeping enough liquidity for operations, anticipating shortfalls, and avoiding cash flow crises. Effective cash flow management is indispensable for the sustainability of any business.

Key Action:

- Monitor cash inflows and outflows weekly or monthly, and project cash flow for the upcoming months.

- Plan for seasonal variations and unexpected expenses.

Outcome:

- Efficient cash flow management shows that you can keep the business operational even during slow periods, ensuring steady growth and stability.

5. Reduced Reliance on Short-Term Loans

As your financial literacy improves, your reliance on short-term loans should decrease. This indicates that you are better managing business expenses and building reserves for unexpected costs.

Key Action:

- Track how often you use loans or credit lines for operational costs.

- Aim to build enough cash reserves to cover emergencies or slow periods.

Outcome:

- A reduced need for borrowing demonstrates that you’ve mastered the fundamentals of business finance, including budgeting, saving, and forecasting.

Pocketly: Your Quick Solution for Unexpected Financial Gaps

Life is full of surprises, and sometimes those surprises come with unexpected expenses, whether it's paying rent, buying last-minute study materials, or covering unplanned travel costs. For students and young professionals, these expenses can put a burden on your budget, leaving you scrambling for cash before your next paycheck. Traditional loans can be slow, and borrowing from friends is often uncomfortable.

That’s where Pocketly steps in. Designed to provide fast financial relief during tight times, Pocketly offers small, flexible loans that fit your short-term needs. Whether you need to cover an urgent bill or fund an unexpected expense, Pocketly provides an easy, paperless solution that quickly deposits funds into your bank account.

How Pocketly Helps You Manage Unexpected Costs:

- Loan amounts between ₹1,000 and ₹25,000, borrow only what you need.

- No need for collateral or a guarantor for approval.

- Quick approval through basic digital verification, so you get funds faster.

- Instant bank transfers ensure you receive your loan without delays.

- Repayment schedules designed to suit your cash flow.

- Clear, transparent pricing with interest starting from 2% per month and processing fees ranging from 1% to 8%.

Working with regulated NBFCs, Pocketly ensures secure and compliant loan disbursements. So, whether it's covering unplanned expenses or giving you financial flexibility, Pocketly helps you bridge the gap without the stress.

Conclusion

Financial literacy is more than just knowing numbers; it's about mastering the art of managing your business’s finances to secure its future. By knowing the essentials of cash flow, budgeting, and ROI, you can make smart, strategic decisions that enable your business to thrive in the long term. With solid financial knowledge, you’ll be able to manage challenges, avoid costly mistakes, and keep your business on track for sustainable growth.

Remember, financial literacy is a journey that evolves as your business grows. Start by mastering the basics, stay disciplined, and be open to refining your approach as you gain experience. The key is to stay current, adaptable, and proactive in managing your business’s finances.

When the unexpected happens, and you need quick financial support, services like Pocketly offer fast, short-term loans to help you manage cash flow gaps without losing focus on your bigger financial picture. Download the Pocketly app on iOS or Android and keep your business finances in balance.

FAQs

1. What does financial literacy mean for entrepreneurs?

Financial literacy for businessmen is the ability to understand and handle the financial aspects of your business, including cash flow, budgeting, financial statements, and investments.

2. How does financial literacy help small business owners?

It allows entrepreneurs to make informed decisions, optimise resources, track performance, and plan for long-term growth, ensuring financial stability and sustainability.

3. Why is financial literacy important for entrepreneurs?

Without financial literacy, entrepreneurs may struggle with cash flow management, incur unnecessary debt, and make poor pricing or investment decisions, leading to business failure.

4. Which financial concepts should entrepreneurs focus on?

Entrepreneurs should focus on understanding cash flow, profit vs loss, budgeting, financial statements (balance sheet, income statement), and ROI (Return on Investment).

5. How can entrepreneurs improve their financial literacy?

Entrepreneurs can improve their financial literacy through online courses, reading business finance books, using financial tools (like accounting software), and seeking advice from financial experts or mentors.