Feeling overwhelmed by multiple debts is all too common. Between credit cards, personal loans, and EMIs, managing due dates and rising interest rates can feel like a never-ending balancing act. The stress of missed payments or juggling high-interest debt can take a major toll on your finances and your peace of mind.

Debt consolidation could be the solution you need. It combines several debts into a single repayment, often with lower interest rates and simplified terms. This makes managing your monthly payments easier, helps reduce overall interest, and gives you a clear path toward becoming debt-free.

In this blog, we’ll explore what debt consolidation really means, how it works, and when it’s the right strategy. By understanding this tool, you can turn scattered, overwhelming debt into one manageable plan and regain control over your financial future.

TL;DR

- Simplifies Payments: Combines multiple debts into a single loan or repayment plan, reducing the stress of juggling multiple due dates.

- Potential Savings: Lower interest rates on consolidated loans or balance transfer cards can reduce total interest costs over time.

- Flexible Options: Personal loans, balance transfer cards, home equity loans, and debt management programmes cater to different financial situations.

- Mindful Money Habits Required: Consolidation works best when paired with budgeting, tracking spending, and avoiding new debt.

- Boosts Financial Control: Makes repayment manageable, improves cash flow, reduces stress, and provides a clear path toward becoming debt-free.

What Is Debt Consolidation?

Debt consolidation is the method of combining numerous debts into a single loan or repayment plan. Instead of managing several credit cards, personal loans, or other debts individually, consolidation lets you make one streamlined monthly payment, often at a lower interest rate or with more flexible terms.

The goal is simple: make debt easier to handle, reduce the stress of multiple due dates, and potentially save on interest over time.

Common ways to consolidate debt include:

- Personal Loan Consolidation: Taking a new loan to pay off existing debts.

- Balance Transfer Credit Cards: Moving high-interest balances to a card with a low or 0% introductory interest rate.

- Home Equity Loans or Lines of Credit: Using your home’s equity to pay off unsecured debts.

Example: Imagine you have three credit cards with high-interest balances and a personal loan. By consolidating them into a single personal loan at a lower interest rate, you only make one monthly payment instead of four. This makes budgeting easier and could reduce your overall interest costs.

Debt consolidation doesn’t erase your debt; it gives you a clearer, simpler path to pay it off faster and more efficiently.

How Does Debt Consolidation Work?

Debt consolidation works by replacing multiple debts with a single loan or repayment plan, simplifying your financial management. Instead of juggling several monthly payments with different interest rates and due dates, you focus on just one payment.

The process usually involves these steps:

- Assess Your Debts: List all your existing debts, including balances, interest rates, and minimal monthly payments. This gives you a clear picture of what needs to be consolidated.

- Choose a Consolidation Method: Decide whether a personal loan, balance transfer credit card, or home equity loan best suits your situation. The right option depends on interest rates, fees, and your ability to repay.

- Apply and Approve: Submit an application for the consolidation loan or card. Lenders review your creditworthiness and financial history to approve the consolidation plan.

- Pay Off Existing Debts: Use the approved loan or credit facility to pay off all existing debts in full. After this, your old accounts may be closed or left with a zero balance.

- Make Single Monthly Payments: Begin paying the new consolidated loan or card according to the agreed schedule. Ideally, this comes with a lower interest rate or more manageable repayment terms, helping you save money and reduce stress.

Example: If you have two credit cards with 20% interest and a personal loan at 15%, you might take a debt consolidation personal loan at 10%. Paying this single loan every month can lower your total interest and simplify your finances.

Debt consolidation doesn’t eliminate debt, but it makes repayment more structured, easier to track, and potentially less expensive.

Benefits of Debt Consolidation

Debt consolidation offers several advantages for people looking to simplify their finances and reduce overall costs.

Debt consolidation offers several advantages for people looking to simplify their finances and reduce overall costs.

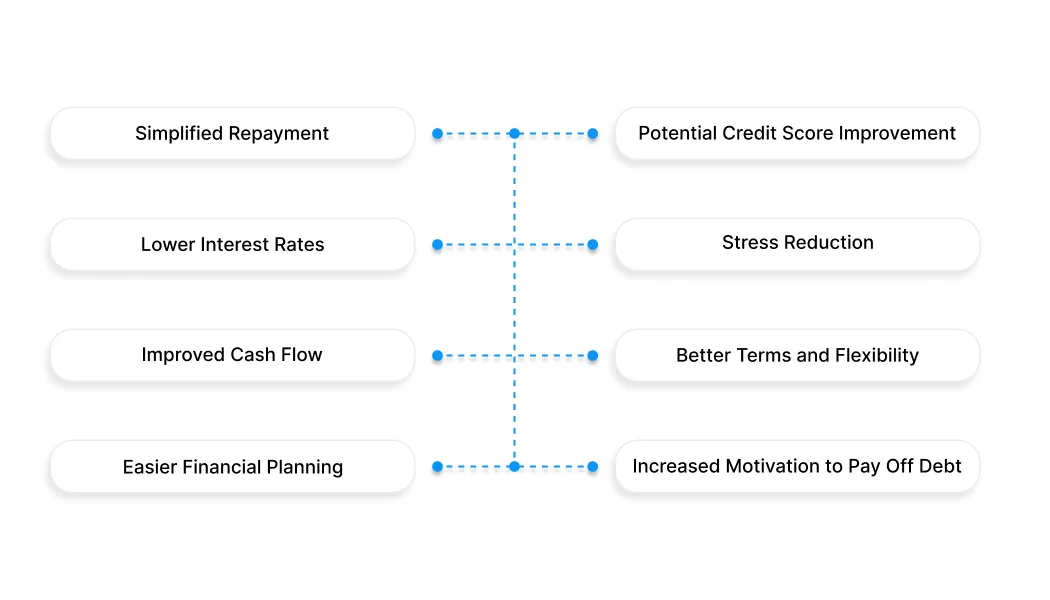

- Simplified Repayment: Instead of managing multiple monthly payments with different due dates, you make just one payment. This reduces confusion and the risk of missed payments.

- Lower Interest Rates: Consolidating high-interest debts into one loan or credit card with a lower rate can reduce the total interest you pay over time, helping you save money.

- Improved Cash Flow: By prolonging the repayment period or lowering the monthly interest, you can reduce your monthly payment amount, freeing up cash for essentials or savings.

- Easier Financial Planning: With a single payment to track, budgeting becomes simpler, giving you a clearer picture of your finances and enabling better long-term planning.

- Potential Credit Score Improvement: Consistently making on-time payments on a consolidated loan can positively impact your credit score, as it reduces the number of active, high-interest accounts.

- Stress Reduction: Managing multiple debts can be overwhelming. Consolidation simplifies your finances, reducing mental strain and helping you focus on paying off debt rather than tracking numerous accounts.

- Access to Better Terms and Flexibility: Some consolidation loans come with adaptable repayment options, such as longer tenures or adjustable monthly instalments, making it easier to manage your financial situation.

- Increased Motivation to Pay Off Debt: Seeing a single loan balance decrease steadily can be more motivating than watching multiple small payments go toward separate debts.

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

Types of Debt Consolidation Options

Debt consolidation is a financial reset, not just a payment shuffle. By strategically combining your debts, you reduce interest, simplify tracking, and create breathing space to tackle what matters most: saving, investing, and planning for your future without the stress of juggling multiple creditors.

1. Personal Loans

A personal loan allows you to pay off multiple debts with a single loan. Typically, these loans have lower interest rates than credit cards, making it easier to pay down principal faster.

Example: Suppose you have three credit cards totalling ₹60,000 at 24% interest. Taking a personal loan of ₹60,000 at 14% interest can reduce monthly payments and save interest while turning multiple payments into just one.

When it works: Ideal for those with good credit scores who want predictable monthly payments without the hassle of multiple due dates.

Caution: Loan approval depends on your creditworthiness, and missing repayments can affect your score.

2. Balance Transfer Cards

Balance transfer cards let you move high-interest credit card debt to a newly issued card with a lower interest rate, sometimes even 0% for an introductory period. This can accelerate debt repayment if used wisely.

Example: Transferring ₹50,000 from a credit card charging 22% interest to a balance transfer card offering 0% for 12 months could save ₹5,000 in interest, provided you pay off the balance before the promo period ends.

When it works: Best for those disciplined enough to pay off the transferred balance within the promotional period.

Caution: Look out for transfer fees (usually 1–5%) and high post-promo interest rates.

3. Home Equity Loans or Lines (HELOCs)

If you own property, you can use your home equity to consolidate high-interest debts. Home equity loans or lines generally offer lower interest rates than unsecured debt.

Example: Using ₹3 lakh of home equity to pay off multiple credit cards at 20%–25% interest can cut monthly payments and free up cash for savings or investment.

When it works: Suitable for homeowners with significant equity, stable income, and the ability to make regular payments.

Caution: Your home is collateral; missing payments could risk foreclosure. It’s essential to plan carefully and treat this as a serious long-term commitment.

4. Debt Management Programs (DMPs)

Non-profit agencies offer DMPs to help you consolidate debts by negotiating lower interest rates or fee waivers with creditors. You make a single monthly payment to the agency, and they give it to your creditors.

Example: A DMP could reduce a total monthly debt obligation from ₹18,000 to ₹12,000 while helping you systematically pay off your creditors over 3–5 years.

When it works: Best for individuals overwhelmed by multiple high-interest debts and struggling to communicate with creditors.

Caution: Programmes may affect your credit score initially, and participation usually requires closing all existing credit card accounts.

Risks and Considerations of Debt Consolidation

While debt consolidation can be helpful, it’s important to understand the possible risks before making a decision.

While debt consolidation can be helpful, it’s important to understand the possible risks before making a decision.

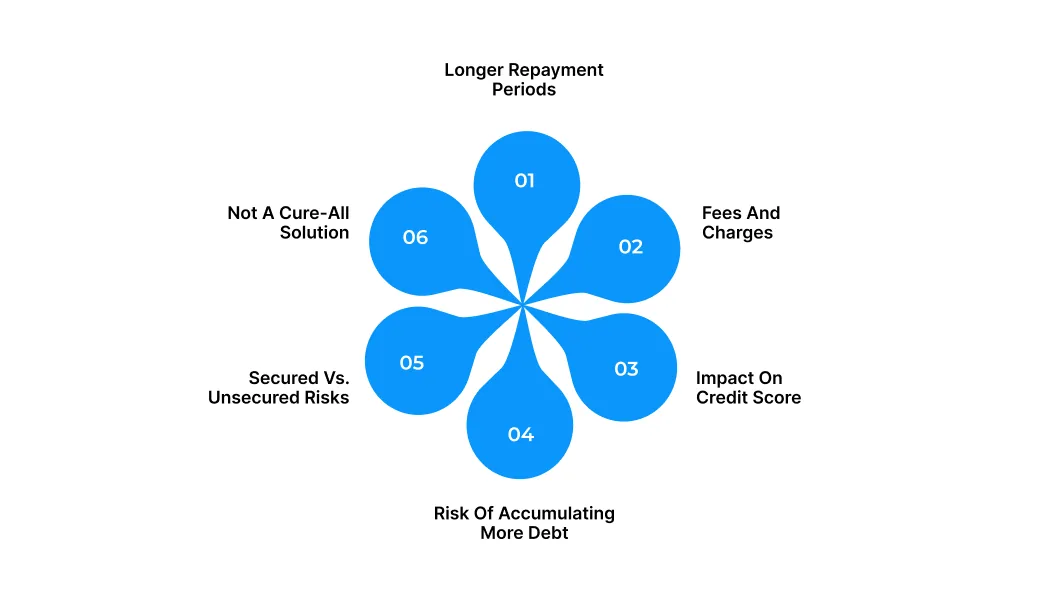

1. Longer Repayment Periods

Risk: Consolidating multiple debts into a single loan often comes with a longer repayment term. While monthly payments may drop, the total interest paid over the life of the loan can increase significantly, sometimes making the debt more expensive in the long run.

Mitigation: Before consolidating, calculate the total interest for different loan durations. For example, if a ₹200,000 consolidation loan at 12% annual interest is paid over 3 years instead of 2, you might save on monthly payments but pay thousands more in interest. Choose a term that balances affordability with overall cost efficiency.

2. Fees and Charges

Risk: Some debt consolidation options include hidden costs such as balance transfer fees, processing charges, annual fees, or prepayment penalties. These fees can offset the financial benefits of consolidation.

Mitigation: Read the loan agreement carefully and ask lenders for a full breakdown of costs. For example, a balance transfer credit card may offer 0% interest for 12 months, but a 3% transfer fee could reduce your savings. Compare multiple offers and factor fees into your decision.

3. Impact on Credit Score

Risk: Applying for a new loan triggers a hard inquiry on your credit report, which may temporarily lower your credit score.

Missing payments on the new consolidated loan can further damage your credit history.

Mitigation: Ensure all existing debts are paid on time until the consolidation is finalised. Limit new credit applications for a few months. For example, consolidating three credit cards into a personal loan may initially drop your score by a few points, but consistent payments can improve it over time.

4. Risk of Accumulating More Debt

Risk: Debt consolidation provides immediate relief but does not solve underlying spending habits. Without proper budgeting, you may accumulate new debts while still paying off the consolidation loan.

Mitigation: Treat the consolidated loan as a priority. For example, if you clear ₹150,000 of credit card debt into a personal loan, avoid opening new credit cards until the loan is repaid. Create a realistic budget and track monthly expenses to prevent overspending.

5. Secured vs. Unsecured Risks

Risk: Secured consolidation options, like home equity loans, use an asset as collateral. Defaulting can lead to losing the asset. Unsecured options like personal loans avoid collateral but often have higher interest rates.

Mitigation: Evaluate your risk tolerance. For instance, if you consolidate ₹300,000 in credit card debt using a home equity loan, a missed payment could risk your property. If you prefer safety, an unsecured personal loan might be better despite slightly higher interest.

6. Not a Cure-All Solution

Risk: Consolidation does not automatically fix debt problems. Poor financial habits, overspending, or a lack of savings will undermine its benefits.

Mitigation: Combine consolidation with budgeting, expense tracking, and a debt repayment plan. For example, set aside ₹5,000 monthly for savings while paying off a ₹200,000 consolidated loan, so you build financial resilience and prevent new debt.

Read More: How to Achieve a Perfect 900 CIBIL Score?

How to Choose the Right Debt Consolidation Method

Selecting the right debt consolidation method is key to making your repayments easier without adding unnecessary costs. Here’s what you should consider before deciding:

| Factor | Personal Loan | Balance Transfer Card | Home Equity Loan |

| Interest Rate | Medium (depends on credit) | Low short-term, higher later | Low to medium |

| Fees | 1–3% processing | 1–5% transfer fee | Varies, may include legal fees |

| Repayment Flexibility | Medium | Medium | High |

| Collateral Required | No | No | Yes |

| Credit Score Needed | Good | Good–Excellent | Excellent |

| Overall Cost | Medium | Variable | Medium–Low |

Tips for Successful Debt Consolidation

Consolidating your debt can be a smart financial move, but only if you approach it carefully. Follow these tips to make consolidation effective and avoid common pitfalls:

Consolidating your debt can be a smart financial move, but only if you approach it carefully. Follow these tips to make consolidation effective and avoid common pitfalls:

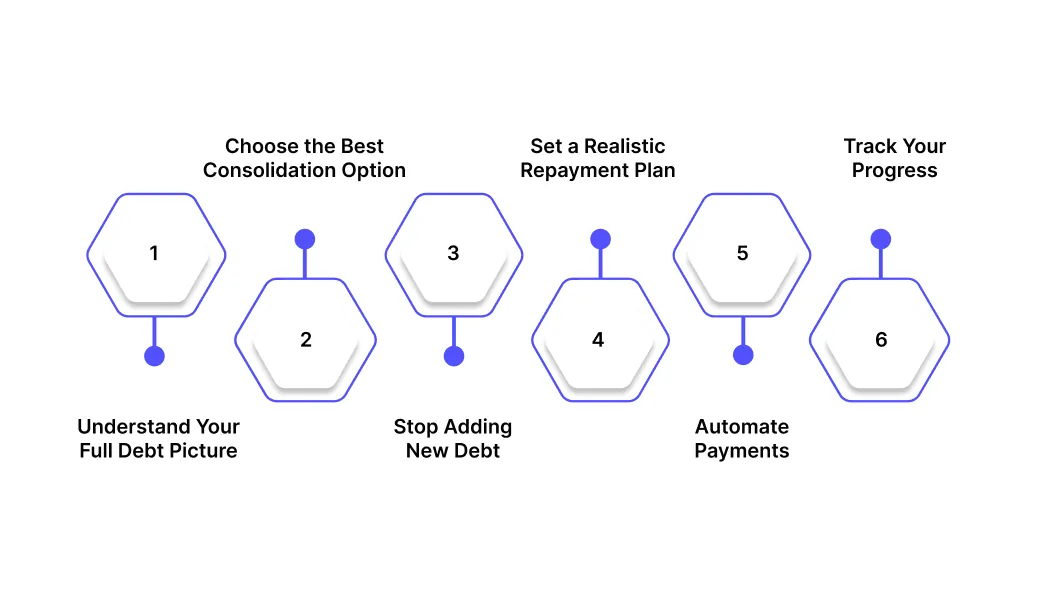

1. Understand Your Full Debt Picture

Start by listing every debt you owe: credit cards, personal loans, EMIs, and any other liabilities, along with balances, interest rates, and minimum monthly payments. Having a clear overview ensures you know exactly what you’re consolidating and prevents surprises. Missing even small debts can cost you more in interest and reduce the benefits of consolidation.

Example: You owe ₹50,000 on Credit Card A at 18%, ₹30,000 on Credit Card B at 20%, and a ₹70,000 personal loan at 12%. Knowing the full ₹1,50,000 total helps you compare consolidation options effectively.

2. Choose the Best Consolidation Option

Explore all available options: personal loans, balance transfer cards, home equity loans, or debt management programmes. Compare interest rates, fees, repayment terms, and eligibility criteria before deciding. Picking the wrong method could increase costs or extend your repayment period unnecessarily.

Example: A balance transfer card with 0% APR can save interest in the short term, but if not cleared before the promo ends, rates may spike. A personal loan at 10% APR could be more cost-effective over time.

3. Stop Adding New Debt

Paying off debt through consolidation only works if you avoid accumulating new liabilities. Adding new credit cards or loans while repaying your consolidation loan can undo progress. Consolidation reorganises debt but does not remove poor spending habits.

Example: Consolidating ₹1,50,000 but charging an additional ₹30,000 on new cards increases total liability, nullifying the benefits.

4. Set a Realistic Repayment Plan

Align monthly payments with your actual budget, accounting for essentials, discretionary spending, and emergency savings. Overestimating what you can pay leads to missed payments, while underestimating extends your repayment period unnecessarily.

Example: If your EMI is ₹15,000 but only ₹13,000 is realistically available, adjust your plan or reduce other non-essential expenses to maintain consistency.

5. Automate Payments

Set up automatic debits for your consolidated loan to avoid late payments and protect your credit score. Late payments lead to additional fees and higher interest rates and can damage your credit profile, making future borrowing difficult.

Example: Automating a ₹15,000 EMI ensures timely repayment even during busy workweeks or travel.

6. Track Your Progress

Monitor your balances, interest savings, and repayment timeline regularly. Tracking progress motivates consistency and reveals opportunities to pay extra toward the principal. Awareness allows for better financial decisions and can help you repay debt faster.

Example: An extra ₹3,000 available mid-month could reduce principal and overall interest, shortening your repayment period.

How Pocketly Helps You Stay on Top of Your Debt

Juggling multiple loans, credit cards, or EMIs can be stressful, especially when unexpected expenses hit. Even with a debt consolidation plan, temporary cash shortfalls can disrupt your progress. Pocketly provides quick, short-term loans that help you bridge these gaps and keep your financial strategy on track.

Here’s how Pocketly supports you:

- Borrow Exactly What You Need: Loans from ₹1,000 to ₹25,000 ensure you cover urgent payments without taking on extra debt.

- Fast, Hassle-Free Approval: A simple KYC process means approval in minutes and instant transfer to your bank account.

- Transparent Pricing: Interest rates start at 2% per month, with processing fees between 1% and 8% no hidden charges.

- Avoid Missed Payments: Use Pocketly to cover EMIs, credit card bills, or other short-term obligations without penalty.

- Anytime, Anywhere Access: Manage your loan entirely through the Pocketly mobile app, 24/7.

With Pocketly, short-term financial gaps don’t have to derail your debt management plan.

Conclusion

Debt can feel like a heavy burden, especially when multiple payments, high interest rates, and due dates start to pile up.

Debt consolidation offers a way to lighten that load by combining your debts into a single, manageable payment. But it’s more than just convenience; it’s a strategy to take control, save on interest, and create a clear path toward financial freedom.

The real benefit of consolidation comes when it’s paired with mindful money habits. Tracking your spending, sticking to a realistic repayment plan, and avoiding new debt are what turn consolidation from a temporary fix into a long-term solution.

Ultimately, debt consolidation is about transforming confusion into clarity. It simplifies your finances, reduces stress, and gives you a roadmap to not just pay off debt but to regain confidence, plan for the future, and take charge of your financial life.

Download the Pocketly app today on [Android] or [iOS] to access funds instantly and keep your finances steady, no matter what comes your way.

FAQs

1. What does debt consolidation mean?

Debt consolidation is the process of combining multiple debts into a single loan or repayment plan. This simplifies payments, may reduce interest rates, and helps you manage your finances more effectively.

2. Will debt consolidation affect my credit score?

Initially, applying for a consolidation loan may cause a small dip in your credit score due to a hard inquiry. However, if you make timely payments on your consolidated loan, your score can improve over time.

3. Can I consolidate all types of debt?

Most unsecured debts, like credit cards, personal loans, and medical bills, can be consolidated. Secured debts, such as home or auto loans, usually require specific options like home equity loans.

4. How long does it take to pay off consolidated debt?

The repayment period depends on the type of consolidation method you choose. Personal loans and balance transfer cards usually have 1–5 year terms, while home equity loans may have longer terms.

5. Is debt consolidation worth it in India?

Yes, if you have multiple high-interest debts, debt consolidation can reduce your monthly payments, lower interest costs, and simplify finances. Always compare interest rates, fees, and repayment terms before proceeding.