Have you ever faced an urgent expense and considered a cash advance, only to wonder if it might hurt your credit score? It can feel like a quick solution in the moment, but the long-term impact is not always clear.

As per RBI insights, household borrowing in India has been rising, which makes it even more important to understand how short-term credit decisions affect your credit score.

For many young professionals, students, and self-employed individuals in India, access to instant funds has become easier than ever. But not all forms of borrowing work the same way when it comes to your credit profile.

A cash advance may seem convenient, but how you use it can directly affect your CIBIL score, a three-digit rating used by lenders to judge your credit reliability. In this blog, you will understand when cash advances can hurt your credit score, when they may not, and how to handle short-term cash needs more responsibly.

Key Takeaways

-

Using cash advances often or missing repayments can lower your credit score because it signals a higher risk to lenders.

-

High usage increases your credit utilisation, which may indicate dependency on credit and affect your overall profile.

-

Repayment behaviour matters more than the type of borrowing, since lenders focus on how consistently you manage dues.

-

Unplanned withdrawals can become expensive and harder to manage, increasing the chances of delayed repayment.

-

Structured short-term options with clear repayment terms can help you handle urgent needs more predictably.

What Is a Cash Advance in India

A cash advance typically refers to two common ways of accessing quick funds:

-

Credit card cash withdrawal from an ATM.

-

Instant short-term loans are offered through digital platforms.

While both provide immediate access to money, they work differently from regular loans. Credit card cash withdrawals often carry higher interest charges and lack a fixed repayment structure, which can make them difficult to manage if not planned properly.

For example, withdrawing cash using a credit card may require you to repay it quickly with added charges, whereas a small short-term loan may come with a defined repayment schedule, making it easier to plan.

How Cash Advances Work

Cash advances are designed for speed and convenience, but that often comes with trade-offs that are easy to overlook.

-

Funds are available instantly, without a detailed approval process.

-

Interest starts accruing immediately, especially for credit card withdrawals.

-

There is usually no interest-free period, unlike regular card spending.

-

Repayment does not follow a fixed EMI structure, making it harder to plan.

This means what feels like a quick solution can become expensive quickly. Without a clear repayment plan, even a small amount can create pressure in the next billing cycle.

Also Read: Applying for an Instant Personal Credit Line Online

Do Cash Advances Hurt Your Credit Score

Yes, cash advances can hurt your credit score, but the impact depends on how you use them.

They do not reduce your score simply because you take one. However, they can influence key factors like your credit utilisation, repayment behaviour, and borrowing patterns, all of which affect your CIBIL score.

For example, withdrawing a large portion of your credit limit or delaying repayment can signal higher risk to lenders, even if the amount itself is small.

When Cash Advances Can Hurt Your Credit Score

The real impact of cash advances shows up in how they are used over time, especially when certain patterns begin to affect your credit behaviour.

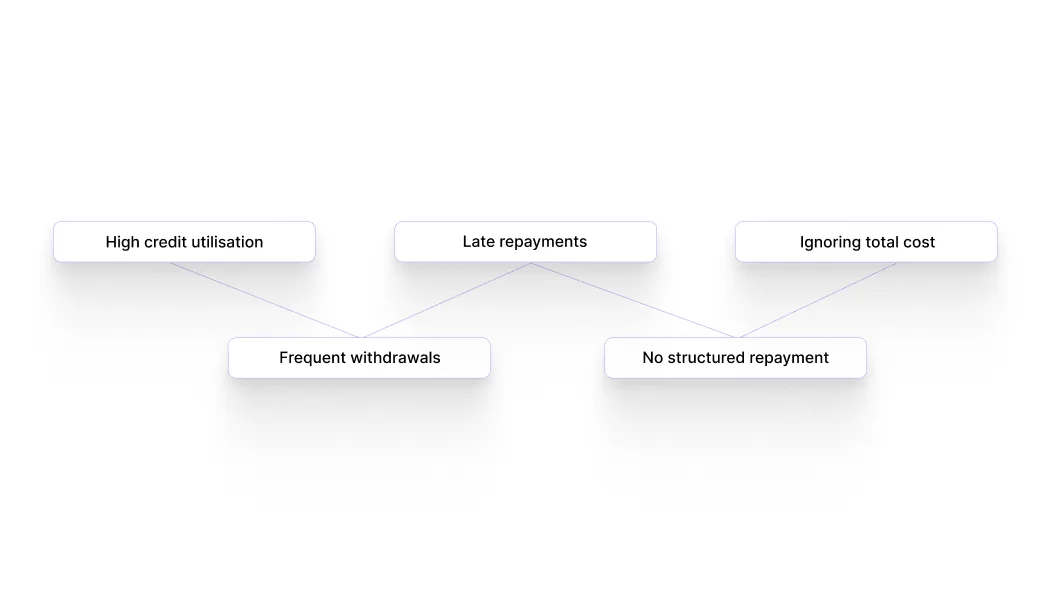

1. High Credit Utilisation

Using a large share of your credit limit for a cash advance pushes your credit utilisation higher. This signals a higher risk to lenders. For example, withdrawing a significant amount from your credit card limit can make it appear that you are heavily dependent on credit.

2. Frequent Withdrawals

Taking multiple cash advances in a short period suggests financial pressure. A salaried professional withdrawing cash several times in a month may appear to be relying on credit to manage regular expenses, which can affect credibility.

3. Late or Delayed Repayments

Repayment history has the strongest impact on your credit score. Even a small delay can have consequences. If you miss the due date or delay repayment due to other expenses, it may get reported and affect your credit profile.

4. Lack of Structured Repayment

Unlike EMIs, cash advances often do not follow a clear repayment structure. Without a defined plan, it becomes easier to delay repayment, which increases the risk of a negative credit impact.

5. Ignoring the Total Cost

Cash advances often come with higher interest and additional charges. A common situation is taking a small amount without checking the full repayment obligation, which later creates pressure and increases the chance of delays.

Before using any cash advance, reviewing the total cost and repayment timeline can help you avoid unnecessary credit impact. Platforms like Pocketly can help manage urgent expenses without collateral commitments.

When Cash Advances May Not Hurt Your Credit Score

Cash advances do not always harm your credit score, but the margin for error is small. The impact depends on how quickly and carefully you manage the repayment.

1. Repaid Quickly

If the amount is repaid within a short period, the impact can be limited because it reduces the chances of high outstanding balances being reported.

For example, if you withdraw ₹4,000 using your credit card a few days before your statement is generated and repay it before the due date, it is less likely to show as a high outstanding balance or significantly affect your credit utilisation.

2. Used Occasionally

Using a cash advance only in genuine emergencies does not automatically signal risk. Lenders typically look for patterns, not isolated decisions.

A one-time withdrawal for an urgent expense is less concerning than repeated use within a short period.

3. Small Amounts

Borrowing a limited amount helps keep your credit utilisation under control and reduces repayment pressure.

For instance, withdrawing a small portion of your available credit limit is less likely to impact your score compared to using a large percentage of it.

4. Important to Keep in Mind

Even in these situations, cash advances are not completely risk-free. High costs and immediate interest can still create repayment pressure if not managed carefully.

How Short-Term Loans Affect Your Credit Score

Your credit score is influenced by patterns, not just one decision. The difference between improvement and damage often comes down to how you handle similar situations over time.

|

Situation |

Impact on Credit Score |

Why It Matters |

|

Quick repayment |

Positive |

Builds repayment history |

|

Small, controlled borrowing |

Positive |

Easier to manage |

|

Occasional usage |

Positive |

Shows disciplined behaviour |

|

High utilisation |

Negative |

Signals credit dependency |

|

Frequent borrowing |

Negative |

Indicates financial stress |

|

Late repayment |

Negative |

Directly affects the CIBIL score |

These patterns are often shaped by small, repeated decisions, which is why certain mistakes tend to impact your credit score more than expected.

Common Mistakes That Increase Credit Risk

Even small decisions can create long-term consequences, especially when they become repeated habits.

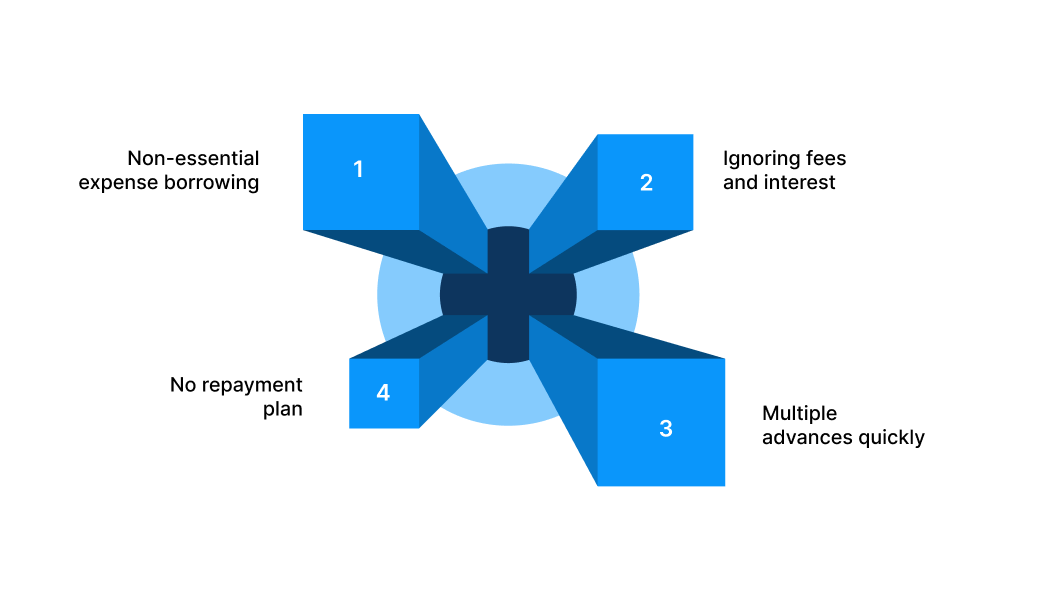

-

Using cash advances for non-essential expenses: This often turns short-term borrowing into a routine. Keeping it limited to genuine needs helps avoid unnecessary dependency.

-

Ignoring fees and interest rates: Overlooking the total cost can lead to repayment pressure later. Checking the full repayment amount before borrowing makes it easier to plan.

-

Taking multiple advances within a short time: Frequent withdrawals can signal financial stress. Spacing out borrowing and relying on income where possible improves credit perception.

-

Not planning repayment in advance: Without a clear repayment plan, delays become more likely. Knowing how you will repay before borrowing reduces the risk of missed deadlines.

Over time, these patterns affect how lenders assess your reliability and can make future borrowing more difficult. Once you understand what creates risk, the next step is to look at more structured ways to manage short-term cash needs without affecting your financial stability.

Also Read: The Ultimate Guide to Small Business Loans in India (2026)

A Structured Way to Handle Short-Term Cash Needs with Pocketly

Not every short-term financial need requires a long-term commitment. The goal is to manage it in a way that keeps your finances stable.

Pocketly is a fintech platform designed to foster financial independence among young Indians, offering simple and transparent access to small, short-term credit when it is needed most. It operates as a digital lending platform, working with RBI-registered NBFCs ike Fairassets Technologies India Private Limited, NDX Financial Services Private Limited, and Speel Finance Company Private Limited to provide structured options without collateral.

Here's how Pocketly supports short-term borrowing in a more structured way:

-

Borrow only what fits your requirement: Loan amounts range from ₹1,000 to ₹25,000, helping you avoid unnecessary borrowing with no hidden charges.

-

No collateral or guarantor required: Apply easily without pledging assets.

-

Quick approval process: Digital KYC enables faster decisions.

-

Direct bank transfer: Funds are credited to your account after approval.

-

Flexible repayment options: Plans are designed to match your income cycle.

-

Transparent pricing: Interest starts from 2% per month, with processing fees between 1% and 8%.

-

24/7 access and customer support: Manage everything through the mobile app.

How to Apply

-

Step 1: Download the app or visit the website.

-

Step 2: Complete a quick digital KYC.

-

Step 3: Select your loan amount.

-

Step 4: Receive approval and funds.

Check your eligibility on Pocketly in a few minutes and manage urgent needs like rent gaps, repairs, or medical expenses without long-term commitments.

How to Stay in Control Going Forward

Short-term credit is likely to remain a part of everyday financial decisions, especially as access to quick funds continues to grow. What will matter more over time is not just access, but how consciously you use it.

Building a strong credit profile comes down to recognising patterns early and making decisions that support long-term flexibility, not just immediate convenience. Small choices around borrowing, timing, and repayment can shape how lenders view your financial reliability in the future.

When short-term needs do arise, approaching them with clarity and structure can make a significant difference in how they impact your overall financial health.

You can explore structured short-term options like Pocketly to better understand what fits your needs before making a borrowing decision. Download Pocketly on iOS or Android to access funds when you need them and stay in control of your finances.

FAQs

1. Does a cash advance affect your CIBIL score in India?

Yes, it can affect your CIBIL score if it increases your credit utilisation or leads to delayed repayment.

2. Does a cash advance show on your credit report?

Yes, it is reflected as part of your credit card usage or borrowing activity, which lenders can review when assessing your profile.

3. Is a cash advance worse than regular credit card usage?

In most cases, yes. Cash advances usually have higher costs and no interest-free period, making them riskier if not managed carefully.

4. How quickly can a cash advance impact your credit score?

The impact depends on your usage and repayment behaviour, and it can reflect within a billing cycle.

5. Can frequent small cash advances affect your creditworthiness?

Yes, repeated usage can signal dependency on credit, even if the amounts are small, which may affect lender perception.

6. What is a more manageable alternative to cash advances?

Structured short-term loans with clear repayment terms can be easier to plan and may reduce financial pressure.