Money gaps do not announce themselves. A surprise bill, a sudden trip, or a week-long salary delay can instantly disturb your financial balance. In that moment, you need quick clarity, not complicated financial jargon.

The problem is that when you search for solutions, you are flooded with options like cash advances and loans, often presented as if they are the same thing. They are not. The costs, repayment structures, and long-term impact can vary significantly. Choosing the wrong one can quietly increase your debt burden or strain your next few months of income.

That is where most people make expensive mistakes.

This blog simplifies cash advances and loans, explains how each works, compares their real costs, and helps you confidently choose the right option based on your urgency and repayment ability.

TL;DR

- Cash advances and loans are not the same. Cash advances solve short-term cash gaps quickly, while loans are better for larger, planned expenses with structured EMIs.

- The real difference lies in cost and repayment pressure. Cash advances are faster but usually more expensive per day. Loans take longer to process, but often cost less over time.

- Choose based on urgency, amount needed, and repayment visibility. If you can repay in your next salary cycle, a cash advance may work. For bigger expenses, a loan is safer and more sustainable.

- Always evaluate total repayment cost, not just interest rate. Processing fees, penalties, and tenure significantly impact how much you actually pay.

- Used responsibly, credit can protect your financial stability. For short-term gaps, platforms like Pocketly offer small-ticket, transparent loans without long-term EMI stress.

What Is a Cash Advance?

A cash advance is a short-term borrowing option that gives you quick access to a small amount of money, typically through a credit card, digital lending app, or salary advance platform. It is designed for urgent and temporary cash gaps.

Key features

- Fast approval, often within minutes

- Minimal documentation and quick KYC

- Smaller loan amounts

- Short repayment tenure

- Interest may start accruing immediately.

- Higher effective cost compared to structured loans

Example: If your salary is delayed by a week and you need ₹5,000 to pay rent or utility bills, a cash advance can provide instant funds that you repay once your salary is credited.

Note: Cash advances are convenient but usually more expensive per day of borrowing. They should be used for short-term emergencies, not ongoing expenses.

What Is a Loan?

A loan is a structured borrowing arrangement where you receive a fixed amount and repay it over a defined period through EMIs. Loans can be personal, secured, or unsecured, depending on the lender and purpose.

Key features

- Fixed loan amount approved upfront

- Defined repayment tenure

- EMI-based repayment structure

- Interest calculated over the full tenure

- Processing fees and documentation are involved

- Often lower interest compared to short-term advances

Example: If you need ₹1,50,000 for home renovation or medical treatment, a personal loan with a 12- to 24-month tenure allows you to repay in manageable monthly instalments.

Note: Loans are better suited for planned, larger expenses where repayment needs to be spread over time in a structured and predictable manner.

Cash Advance vs Loan: Detailed Comparison

At first glance, cash advances and loans may seem like similar borrowing options. In reality, they differ significantly in terms of cost, flexibility, repayment pressure, and overall financial impact.

Choosing the wrong option for your situation can increase your repayment burden or create unnecessary stress in the coming months.

Before making a decision, compare them across the factors that truly matter to your budget and cash flow.

Here is a clear, practical breakdown to help you evaluate both options with confidence.

| Criteria | Cash Advance | Loan |

| Purpose | Meant for urgent, short-term cash gaps | Designed for planned or larger financial needs |

| Approval Time | Usually instant or within a few hours | Ranges from same day to a few days |

| Borrowing Amount | Small amounts, typically lower limits | Higher amounts depending on eligibility |

| Repayment Period | Very short tenure or single repayment | Fixed tenure spread across months or years |

| Repayment Method | Lump sum or short-term instalments | Structured EMIs |

| Interest Cost | Higher effective cost; interest often starts immediately | Lower relative cost spread over the tenure |

| Documentation | Minimal, basic KYC | Income proof and additional documents may be required |

| Financial Impact | Can strain next month’s budget if not planned | Easier to plan monthly repayments |

| Suitable For | Salary delays, emergency bills, and a short cash crunch | Medical expenses, education, renovation, and debt consolidation |

Also Read: Should You Save for an Emergency Fund or Pay Off Debt?

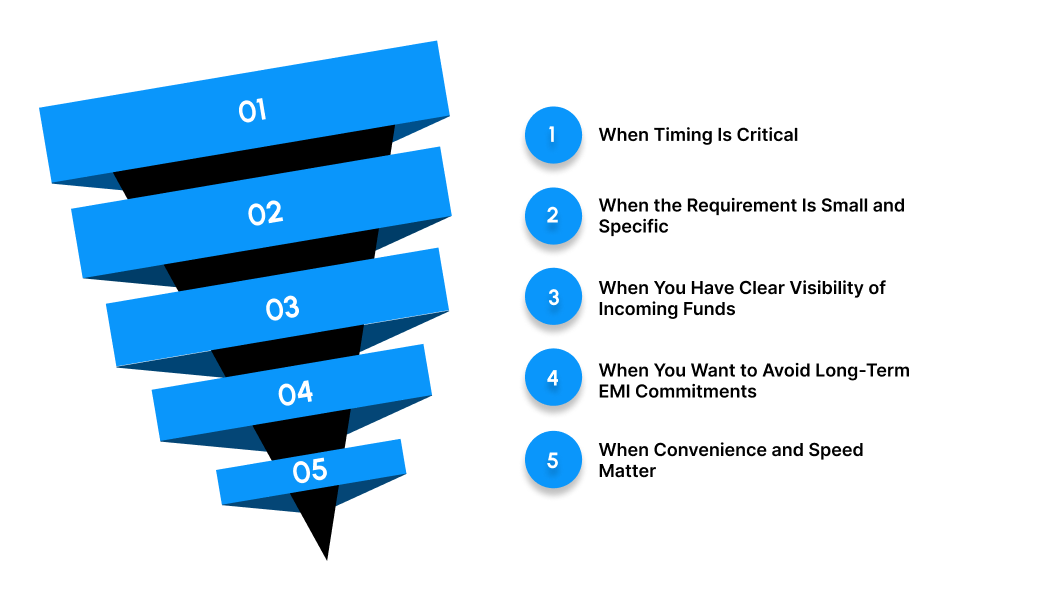

When Should You Choose a Cash Advance?

A cash advance is not just about speed. It is about solving a short-term liquidity gap without entering a long repayment cycle. It works best when the problem is temporary, and the repayment timeline is clear.

1. When Timing Is Critical, and Delays Have Consequences

Some expenses cannot wait without creating additional costs or stress. Late rent, overdue utility bills, or urgent travel bookings often come with penalties or price increases if delayed. In such cases, access to immediate funds matters more than negotiating a lower interest rate over months.

For example, if your landlord charges a late fee after the due date, paying on time with a small advance may actually cost less than missing the deadline and paying penalties later.

2. When the Requirement Is Small and Specific

One of the biggest borrowing mistakes is taking a large loan for a minor expense. A structured loan may offer lower interest, but spreading a small requirement over months increases your total repayment burden and keeps you in debt longer than necessary.

For instance, if you need ₹5,000 for a medical consultation and medicines, committing to a six-month EMI plan would extend the obligation far beyond the actual need. A short-term advance keeps the borrowing proportional to the problem.

3. When You Have Clear Visibility of Incoming Funds

Cash advances are most effective when you already know how and when you will repay them. They are meant to bridge a confirmed inflow, not uncertain income.

For example, if your salary is credited in five days or a client payment is due next week, a cash advance can temporarily support your expenses without affecting your long-term financial structure.

4. When You Want to Avoid Long-Term EMI Commitments

Taking a personal loan creates a fixed EMI obligation that reduces your monthly flexibility. If the expense does not justify months of repayment, a short-term solution may be more practical.

For example, instead of locking yourself into a twelve-month EMI for a one-time urgent bill, a short advance allows you to resolve the issue and move on without a prolonged financial commitment.

5. When Convenience and Speed Matter More Than Negotiation

Traditional loans may require proof of income, verification calls, or waiting periods. In situations where you need funds outside banking hours or within minutes, digital cash advances provide operational convenience.

For example, if an emergency repair is required at night and you cannot wait until the next business day, a digital advance can help you act immediately.

When Is a Loan a Better Option?

A loan becomes the smarter choice when the financial need is substantial, planned, or requires repayment flexibility over time. Unlike cash advances, loans are structured to distribute financial pressure evenly instead of concentrating it in the short term.

1. When the Financial Requirement Is Significant

Larger expenses require a repayment strategy, not just quick access to funds. Using short-term borrowing for high amounts can create repayment pressure within weeks. A loan spreads the burden across months or years, reducing immediate strain on your income.

For example, if you need ₹2,00,000 for surgery, education fees, or major home repairs, structured EMIs allow you to manage the cost gradually rather than scrambling to repay a large sum quickly.

2. When You Need Long-Term Financial Stability

Loans provide defined repayment schedules with fixed EMIs. This predictability allows you to integrate repayments into your monthly budget without uncertainty. You know exactly how much you owe and for how long.

For instance, committing to a 24-month EMI plan of ₹9,000 per month makes it easier to plan your savings and lifestyle spending than facing a large lump sum repayment deadline.

3. When Lower Total Borrowing Cost Is a Priority

Although loans may involve processing time and documentation, they often come with lower effective interest rates compared to short-term advances. Over a longer tenure, this can significantly reduce the overall repayment amount.

For example, funding a professional certification through a structured loan may cost less in total interest than repeatedly using short-term borrowing to cover instalments.

4. When You Want to Build or Strengthen Your Credit Profile

Timely EMI payments contribute positively to your credit history. Lenders view structured repayment behaviour as a sign of financial discipline. Over time, this can improve your eligibility for larger loans or better interest rates.

For instance, maintaining consistent repayment on a personal loan can enhance your creditworthiness, making future borrowing more affordable.

5. When the Expense Is Planned Rather Than Reactive

If you are preparing for a known milestone such as higher education, a wedding, relocation, or business investment, applying for a loan in advance allows you to compare offers, negotiate terms, and choose a suitable tenure.

For example, planning a home renovation loan months ahead gives you the opportunity to align EMIs with your income cycle instead of rushing into expensive short-term borrowing.

Risks of Cash Advances and Loans (And How to Avoid Debt Traps)

Borrowing can be helpful when managed responsibly, but it also comes with risks that are often underestimated. Understanding these risks before you apply allows you to make informed decisions and avoid long-term financial strain.

Below are the most common pitfalls of cash advances and loans, along with practical ways to protect yourself.

1. High Interest Costs

Risk: Cash advances and short-term loans usually carry higher interest rates than traditional personal loans. In many cases, interest starts accruing immediately, and shorter repayment windows increase financial pressure. If repayment is delayed, even by a few days, the total payable amount can rise quickly, making the loan far more expensive than expected.

Mitigation: Focus on the total repayment amount, not just the interest rate. Ask: how much will I repay in absolute rupees? Compare options using total cost, not speed of approval. If the expense is not urgent, consider adjusting your budget or using partial savings to reduce the borrowed amount and overall interest burden.

2. Hidden Fees and Charges

Risk: Processing fees, late payment penalties, GST, convenience fees, and prepayment charges can significantly increase the real cost of borrowing. Many borrowers only look at the advertised interest rate and overlook how deductions reduce the amount actually received.

Mitigation: Check three numbers before accepting any offer: the amount disbursed, the total repayment amount, and the exact due date. Review the full fee structure in writing. Transparent lenders clearly show these figures upfront, allowing you to make an informed decision.

3. Overborrowing

Risk: Higher eligibility limits can create a misleading sense of affordability. Borrowing more than necessary increases repayment stress and can disrupt essential monthly expenses like rent, groceries, or EMIs. This often leads to dependency on new loans to manage existing ones, creating a debt cycle.

Mitigation: Borrow based on need, not eligibility. Calculate how much you can comfortably repay from your next income cycle without affecting essentials or savings. Treat short-term credit as a temporary bridge, not an extension of your income.

4. Impact on Credit Score

Risk: Missed payments, frequent loan applications, or loan stacking can negatively affect your credit score. A lower score reduces your chances of securing larger loans at favourable interest rates in the future and may increase borrowing costs.

Mitigation: Pay on or before the due date and avoid applying for multiple loans within a short period. Track your credit activity regularly to ensure accuracy. Responsible usage strengthens your credit profile and improves access to better financial options over time.

5. Short Repayment Cycles

Risk: Many cash advances and short-term loans require repayment within a few weeks or a single billing cycle. If your cash flow is already tight, short tenures can strain your finances and increase the likelihood of missed payments or rollover borrowing.

Mitigation: Choose a repayment tenure that realistically aligns with your income schedule. Before borrowing, evaluate whether the repayment date matches your salary or revenue cycle to avoid unnecessary financial stress.

Also Read: Applying for an Instant Personal Credit Line Online

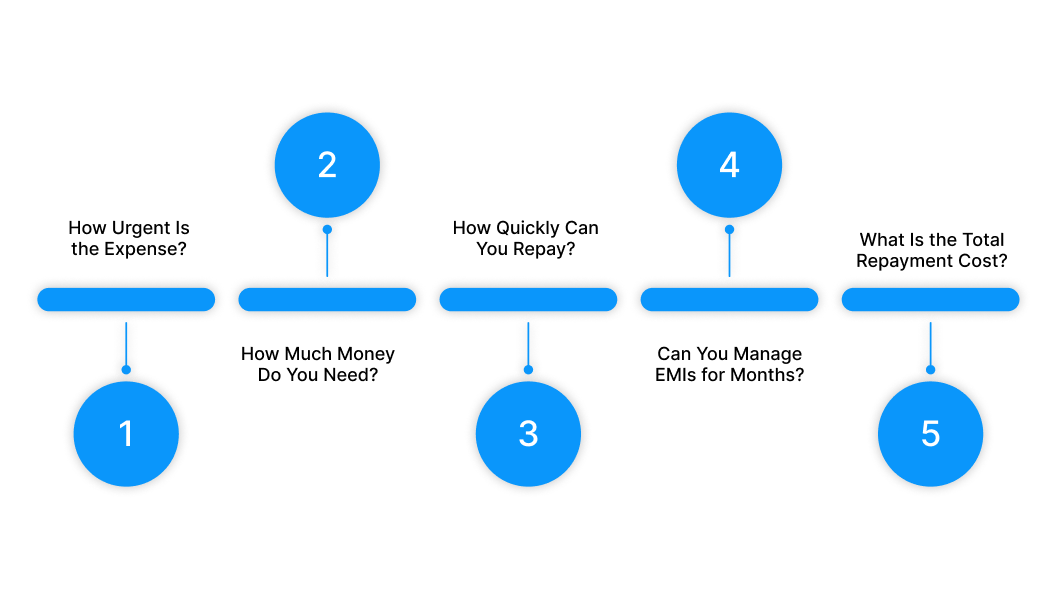

How to Choose Between a Cash Advance and a Loan?

Before you borrow, pause and evaluate your situation logically. The right choice depends less on preference and more on urgency, amount, repayment capacity, and total cost. Use this practical scorecard to guide your decision.

1. How Urgent Is the Expense?

If the money is needed within hours or the same day, speed becomes the priority. Cash advances are typically processed faster, often with minimal documentation.

If the expense can wait a few days and you can complete verification steps, a structured loan may offer better terms.

What to consider: Is this an emergency, or can it wait 2 to 3 days?

2. How Much Money Do You Need?

Cash advances usually work best for small amounts meant to cover temporary gaps. Loans are more suitable when the requirement is larger and needs a structured repayment.

What to consider: Is this a short-term cash shortfall or a bigger financial commitment?

3. How Quickly Can You Repay?

Cash advances often require repayment within a short cycle. If you are confident about clearing the amount within weeks, this can work.

Loans spread repayment over months through EMIs, reducing short-term pressure but increasing total repayment duration.

What to consider: Will your next salary comfortably cover repayment?

4. Can You Manage EMIs for Months?

A loan creates a monthly financial obligation. If your income is stable and predictable, EMIs can be manageable.

If your income fluctuates or you want to avoid long-term commitments, a short-term advance may feel less restrictive.

What to consider: Do you want a one-time short settlement or a structured monthly plan?

5. What Is the Total Repayment Cost?

Never compare just interest rates. Look at total repayment, including processing fees, daily interest, penalties, and late charges.

Cash advances may appear small, but they can carry higher effective costs. Loans may offer lower rates but accumulate interest over a longer tenure.

What to consider: How much will you repay in total, not just per month?

Simple Decision Matrix

| Situation | Better Option |

| Urgent expense, need money today | Cash Advance |

| Small amount for short-term gap | Cash Advance |

| Large planned expense | Loan |

| Stable income, comfortable with EMIs | Loan |

| Can repay fully in the next salary cycle | Cash Advance |

| Need a lower interest over a longer tenure | Loan |

Need Quick Cash Without Long-Term EMI Stress? Pocketly Makes It Simple

When sudden expenses hit, whether it’s an urgent bill, travel booking, medical cost, or an unexpected gap before payday, you don’t always need a large, long-term loan. Sometimes, you just need quick, manageable support to stay on track.

That’s where Pocketly steps in.

Here’s why Pocketly works well for short-term cash needs:

- Borrow only what you need: Loan amounts range from ₹1,000 to ₹25,000, so you don’t take on more debt than necessary.

- No collateral required: There’s no need to pledge gold, property, or arrange a guarantor. The process is completely unsecured and simple.

- Quick approval process: With fast KYC verification, loan decisions are made quickly without complicated paperwork.

- Instant bank transfer: Once approved, funds are credited directly to your bank account, helping you handle urgent expenses without delay.

- Flexible repayment options: Choose a tenure that fits your budget so repayment feels manageable instead of overwhelming.

- Transparent pricing: Interest rates start from 2% per month, with processing fees between 1% and 8% depending on your profile and loan amount. No hidden charges.

- Available anytime: The entire process happens through the Pocketly mobile app, which means you can apply, track, and manage your loan 24/7.

Pocketly partners with regulated NBFCs to provide secure, short-term loans with clear terms and responsible lending practices. When your cash flow falls short temporarily, Pocketly helps you bridge the gap without locking you into long-term financial strain.

Conclusion

In 2026, access to credit is easier than ever, but smart borrowing is what protects your financial stability. Cash advances and loans serve different purposes, and the right choice depends on urgency, the amount required, and your repayment capacity.

Cash advances can help manage short-term gaps quickly. Loans are better suited for larger expenses that need structured repayment. The key is to evaluate total repayment cost, affordability, and how the borrowing fits into your monthly budget before making a decision.

When used thoughtfully, credit can support your financial goals instead of creating stress.

If an unexpected expense stretches your budget, Pocketly offers small-ticket loans with transparent pricing, quick approvals, and flexible repayment options. Download the Pocketly app today on [Android] or [iOS] to access funds when you need them and stay in control of your finances.

FAQs

1. What is the difference between a cash advance and a loan?

A cash advance is usually a small, short-term amount borrowed quickly, often through a credit card or instant lending app, and repaid within a short period. A loan is typically a larger amount repaid in structured EMIs over several months or years.

2. Are cash advances more expensive than personal loans?

In many cases, yes. Cash advances often carry higher interest rates and may start accruing interest immediately. Personal loans generally offer lower interest rates and longer repayment tenures, which can make them more cost-effective for bigger financial needs.

3. Does taking a cash advance affect your credit score?

It can. If the lender reports to credit bureaus, timely repayment may help build your credit history, while missed or delayed payments can reduce your credit score. Frequent borrowing may also signal financial strain to future lenders.

4. When should I choose a cash advance instead of a loan?

A cash advance may be suitable for urgent, small-ticket expenses like medical bills, emergency travel, or temporary cash flow gaps. If you need a larger amount or more time to repay, a structured loan may be the better option.

5. What are the typical interest rates for cash advances and loans in India?

Interest rates vary depending on the lender and your credit profile. Cash advances often charge higher monthly rates, while personal loans usually have lower annualised interest rates. Always review the total repayment cost, including processing fees and penalties.