Have you ever taken a small loan and wondered whether it will actually help your credit score or quietly work against you? It can feel unclear, especially when you are trying to build your credit for the first time.

As per RBI insights, India's household debt has risen to around 41% of GDP, with a significant portion driven by consumption needs. This reflects how more people are relying on short-term borrowing, making it important to understand how these decisions affect your credit score.

For many young professionals, students, and self-employed individuals, these loans are a common way to handle urgent expenses. However, a loan itself does not improve your credit score. What matters is how you use it.

In this blog, you will understand when short-term loans can improve your credit score, when they can hurt it, and how to use them responsibly.

Key Takeaways

-

Short-term loans can improve your credit score when repaid on time, as they build a consistent repayment history.

-

Late payments or frequent borrowing can lower your score, as lenders may see it as a sign of financial stress.

-

Your credit behaviour matters more than the loan itself, since lenders focus on how you manage repayments over time.

-

Small, controlled borrowing can help build your credit profile, especially if you are new to credit.

-

Planning your repayment in advance helps you avoid delays and manage short-term loans without affecting your credit score.

What Is a Short-Term Loan and Who Uses It

Short-term loans are small amounts borrowed for a limited period, usually to handle immediate financial needs. In India, these typically range between ₹1,000 and ₹25,000 and are used for short-duration gaps.

Students may use them for exam fees or repairs. Salaried professionals often rely on them during month-end shortages. Small entrepreneurs may use them to manage quick working capital needs.

The purpose is to solve an immediate problem without committing to a long repayment cycle.

How Your Credit Score Actually Works in India

Your credit score reflects how you manage borrowed money over time. In India, this is commonly referred to as your CIBIL score. It is a three-digit score that reflects how you manage credit and helps lenders assess your eligibility for loans.

It is not based on the type of loan you take, but on how you handle it.

Key factors include:

-

Repayment history: Whether you pay on time.

-

Credit utilisation: How much credit you use.

-

Credit mix: The range of credit products in your profile.

-

Borrowing behaviour: How frequently you take loans.

Among these, repayment history has the highest impact. Even one missed payment can negatively impact your CIBIL score and affect your chances of getting approved for future credit.

Read More: How to Achieve a Perfect 900 CIBIL Score?

When Short-Term Loans Can Improve Your Credit Score in India

Short-term loans can improve your credit score, but only when they are used responsibly. They do not automatically increase your score. Instead, they give you an opportunity to demonstrate how well you manage borrowed money.

When handled correctly, they can strengthen your credit profile over time.

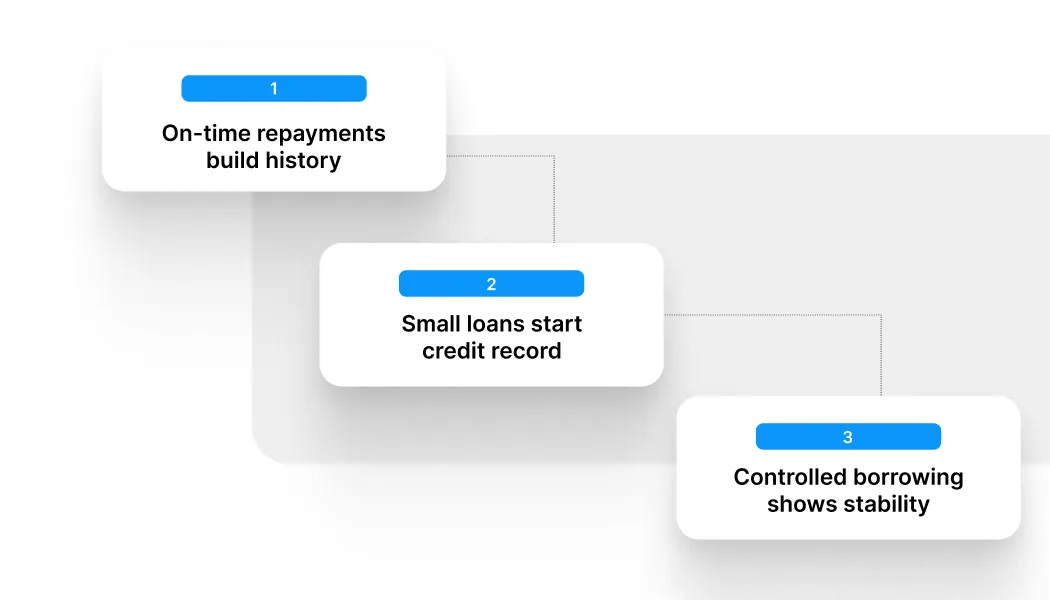

1. On-Time Repayments Build Credit History

Paying your loan on or before the due date shows lenders that you are reliable. If you take a ₹5,000 loan and repay it on time every month, it creates a positive repayment record that strengthens your credit profile.

2. Small Loans Help You Start Building Credit

If you are new to credit, even a small loan can help establish your history. For instance, a student taking a short-term loan for exam fees and repaying it on time begins building a credit track record from scratch.

3. Controlled Borrowing Reflects Financial Stability

Borrowing only when necessary and managing repayments well signals discipline. Someone who takes one loan occasionally and clears it properly is seen as lower risk compared to someone who borrows frequently.

If you are planning to take a small loan, checking repayment timelines in advance can help you avoid unnecessary credit impact.

When Short-Term Loans Can Hurt Your Credit Score

Short-term loans can reduce your credit score if they are not managed carefully. It is not the loan itself, but the pattern of behaviour around borrowing and repayment that lenders assess.

1. Late or Missed Payments

Even a single delayed payment can negatively affect your credit score because repayment history carries the highest weight in your CIBIL score. Lenders track consistency, not just intent.

A common situation is when someone takes a small loan, thinking it will be easy to repay, but forgets the due date or delays it by a few days due to other expenses. Even this short delay can get reported and stay on your credit record.

Over time, frequent delays make lenders more cautious, which can lower your chances of approval or result in stricter borrowing terms.

2. Borrowing Too Frequently in a Short Period

Taking multiple loans within a short time can signal financial instability. It suggests that you are relying on credit repeatedly instead of managing expenses through income.

For example, a salaried professional might take a small loan mid-month, then apply for another one before the first is fully repaid. From a lender's perspective, this pattern indicates increasing dependence on credit.

Frequent applications also create multiple credit inquiries, which can further impact your score and reduce your credibility.

3. High Dependence on Short-Term Credit

Using loans regularly for routine expenses can indicate that your income is not sufficient to support your lifestyle. This reduces your overall financial reliability in the eyes of lenders.

A relatable example is someone who takes a loan almost every month to cover rent, groceries, or bills. While each loan may be small, the pattern shows ongoing dependency rather than occasional need.

This kind of behaviour can lower your creditworthiness over time, even if you are repaying each loan, because it reflects limited financial flexibility.

4. Taking More Than You Can Comfortably Repay

Borrowing beyond your repayment capacity increases the risk of delays or missed payments. Even if approval is quick, repayment pressure builds up later.

For instance, taking a ₹15,000 loan when you only needed ₹7,000 may seem convenient at the moment. But the higher repayment amount can strain your budget, especially if other expenses come up.

This often leads to partial payments, delays, or rolling over the loan, all of which can negatively impact your credit score.

5. Ignoring the Total Cost of Borrowing

Focusing only on the amount received and not the total repayment obligation can lead to poor financial decisions. Interest and fees add up, especially if repayment is delayed.

A typical situation is when someone takes a small loan without checking the full repayment amount and later struggles to adjust their monthly budget to cover it.

Your credit score is influenced by patterns, not just one decision. The difference between improvement and damage often comes down to how you handle similar situations over time.

|

Situation |

Impact on Credit Score |

Why It Matters |

|

On-time repayment |

Positive |

Builds a strong repayment history |

|

Borrowing small amounts |

Positive |

Easier to manage and repay |

|

Occasional borrowing |

Positive |

Shows controlled credit usage |

|

Late payments |

Negative |

Directly affects repayment history |

|

Frequent borrowing |

Negative |

Signals financial stress |

|

High dependency on loans |

Negative |

Reduces financial credibility |

These patterns are often shaped by small, repeated decisions, which is why certain mistakes tend to impact your credit score more than expected.

Common Mistakes That Lower Your Credit Score

Even small decisions can create long-term impact if not managed carefully.

-

Taking more than you actually need.

-

Not planning repayment before borrowing.

-

Using multiple lending platforms at the same time.

-

Ignoring due dates or reminders.

Over time, these patterns reduce your creditworthiness and make future borrowing harder.

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

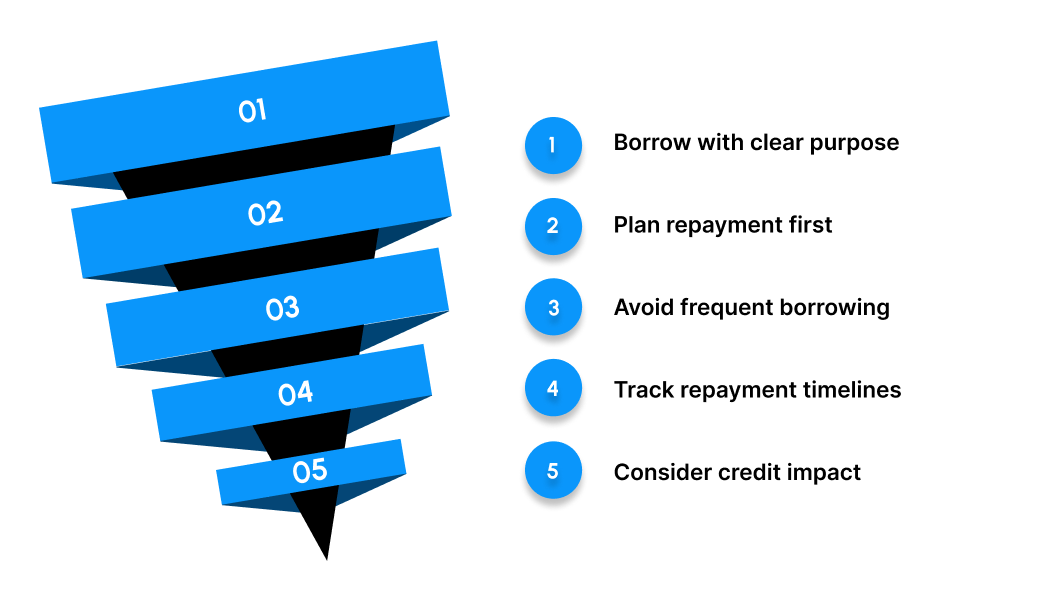

How to Use Short-Term Loans Without Hurting Your Credit Score

Short-term loans can either strengthen or weaken your credit profile. The difference comes down to how you use them in real situations.

-

Borrow with a clear purpose, not convenience: Taking a loan only when necessary helps you avoid unnecessary financial pressure later.

-

Commit to repayment before you borrow: Knowing exactly how you will repay the amount reduces the risk of delays and missed payments.

-

Keep your borrowing occasional, not routine: Using loans too frequently can signal dependency, even if the amounts are small.

-

Stay aware of your repayment timeline: A missed due date, even by a few days, can impact your credit history.

-

Think beyond approval and focus on impact: Getting a loan easily does not mean it is always the right decision for your financial profile.

Building a strong credit profile is important, but it does not eliminate short-term financial needs. There will still be moments when your expenses and income do not align perfectly.

Managing Short-Term Cash Gaps Without Long-Term Stress

When a short-term cash gap comes up, the goal is to handle it without adding long-term financial pressure. Unstructured options can solve the problem quickly, but often make repayment harder later.

Structured, short-term solutions designed for smaller amounts can help bridge this gap more predictably. Platforms like Pocketly, a digital lending platform, offer access to such options with clear terms and a fully digital process.

A Structured Way to Manage Short-Term Cash Needs with Pocketly

Not every short-term financial need requires a long-term commitment. The key is to handle it in a way that solves the immediate problem without creating additional pressure later.

This is where structured short-term options become useful. Instead of relying on unplanned borrowing, having clarity on the amount, repayment, and overall cost can make a significant difference.

Pocketly is a fintech platform designed specifically for young Indians, focusing on providing simple and transparent access to small, short-term credit when it is needed most.

Here's how Pocketly supports short-term borrowing in a more structured way:

-

Borrow only what fits your requirement: Loan amounts range from ₹1,000 to ₹25,000, helping you avoid unnecessary borrowing with no hidden charges.

-

No collateral or guarantor needed: You can apply without pledging assets or involving another person.

-

Quick approval process: A digital KYC-based system helps you make decisions faster.

-

Direct transfer to your bank account: Once approved, the amount is credited to your account for immediate use.

-

Flexible repayment options: Plans are designed to align with your income cycle.

-

Clear and transparent pricing: Interest starts from 2% per month, with processing fees between 1% and 8%.

-

24/7 access through the app and online customer support: You can apply and manage everything digitally at your convenience.

How to Apply

-

Download the app or visit the website.

-

Complete a quick digital KYC.

-

Select the loan amount.

-

Receive approval and funds.

What to Keep in Mind Before Taking Any Short-Term Loan

Before you decide, it helps to look at the full picture:

-

Understand the total cost, including interest and fees.

-

Check if the repayment timeline fits your income cycle.

-

Borrow only what you actually need.

-

Be clear about how you will repay it.

Taking a moment to review these points can help you avoid unnecessary financial pressure later.

If you need a small amount for an urgent expense, you can check your eligibility on Pocketly in a few minutes. Download Pocketly on iOS or Android to access funds when you need them and stay in control of your finances.

FAQs

1. Does taking a short-term loan increase your CIBIL score immediately?

No, your CIBIL score does not increase instantly. It improves gradually based on consistent, on-time repayments over time.

2. How many points can a loan add to your credit score?

There is no fixed number. The impact depends on your repayment behaviour, existing credit history, and overall borrowing pattern.

3. Does missing one EMI affect your credit score significantly?

Yes, even a single missed payment can reduce your score and remain on your credit report, affecting future loan approvals.

4. Is taking a loan only to build credit a good strategy?

It is better to take loans only when needed. Responsible usage improves your score, but unnecessary borrowing can create financial pressure.

5. Can frequent small loans affect your creditworthiness?

Yes, multiple loans in a short period can signal dependency on credit and may lower your credibility with lenders.

6. What matters more for your credit score, loan amount, or repayment behaviour?

Repayment behaviour matters more. Even a small loan can improve your score if managed well, while poor repayment can reduce it.