Have you ever assumed a loan was affordable just because the interest rate looked low, only to realise the total cost was much higher later? That’s the reality for many borrowers in India, especially with flat interest rates, where the way interest is calculated can quietly inflate what you end up paying.

This matters more than ever: India’s household debt climbed to 41.3% of GDP by March 2025, driven largely by consumption loans such as personal and consumer credit.

Flat interest rates may sound simple and predictable, but they often cost more than reducing rates in practice, especially for everyday borrowers. In this blog, we’ll strip away the confusing math and show you exactly how flat rates work.

By the end of this blog, you’ll know why they can be expensive and how to choose smarter loan options so you don’t pay more than you should.

Key Takeaways

-

Flat interest rates charge interest on the full loan amount, which can make even “low” rates surprisingly expensive over time.

-

Reducing interest rates calculates interest on the remaining balance, so your payments gradually cost less as you repay, saving you significant money on long-term loans.

-

Flat rates work best for short-term, small loans with fixed EMIs, making budgeting simple and predictable for students and salaried employees.

-

Hidden costs like prepayment penalties, processing fees, and low initial EMIs can make flat loans misleading if you don’t check the total repayment carefully.

-

Understanding how each method affects your EMI, total interest, and tax benefits helps you choose smarter loans and avoid paying more than necessary.

What is a Flat Interest Rate?

A flat interest rate is a method of calculating interest where the interest is charged on the entire original loan amount (principal) for the full tenure, regardless of the monthly repayments you make.

Formula for Total Interest: Total Interest = Principal × Rate of Interest × Tenure (in years)

Formula for EMI (Flat Rate): EMI = (Principal + Total Interest) ÷ Number of Months

Example:

-

Loan Amount (Principal) = ₹5,00,000

-

Flat Interest Rate = 10% per year

-

Loan Tenure = 3 years

Step 1: Calculate Total Interest

Total Interest = 5,00,000 × 10% × 3 = 1,50,000

Step 2: Total Repayment

Total Repayment = 5,00,000 + 1,50,000 = 6,50,000

Step 3: Monthly EMI

EMI = 6,50,000 ÷ 36 ≈ 18,056

What is a Reducing Interest Rate?

A reducing interest rate (also called diminishing balance interest) is a method where interest is calculated only on the outstanding loan balance, not the original principal. This means that as you repay the loan, the interest portion decreases over time, making it cheaper than a flat rate loan.

Formula for EMI (Reducing Balance Method / Standard EMI Formula):

EMI = [P × R × (1+R)^N] ÷ [(1+R)^N – 1]

Where:

-

P = Principal (loan amount)

-

R = Monthly interest rate (annual rate ÷ 12 ÷ 100)

-

N = Total number of monthly instalments

Example:

-

Loan Amount (Principal) = ₹5,00,000

-

Reducing Interest Rate = 10% per year

-

Loan Tenure = 3 years (36 months)

Step 1: Convert the annual rate to a monthly rate

R = 10 ÷ 12 ÷ 100 ≈ 0.00833

Step 2: Apply the EMI formula

EMI = [5,00,000 × 0.00833 × (1+0.00833)^36] ÷ [(1+0.00833)^36 – 1] ≈ 16,134

Flat vs Reducing Rate: Which One Actually Saves You Money?

To compare flat and reducing rates effectively, focus on total interest paid, EMI stability, and the rate at which your principal decreases. These metrics reveal which loan truly costs less and fits your repayment capacity.

Here’s how to compare both methods so you can clearly see which one actually saves you money:

|

Feature / Factor |

Flat Interest Rate |

Reducing (Diminishing) Interest Rate |

|

Interest Calculation |

Calculated on the full principal for the entire loan tenure |

Calculated on outstanding principal, decreases as the principal reduces |

|

EMI Structure |

Fixed EMIs for principal + interest |

EMI reduces slightly over time, or fixed EMI with a changing principal-interest ratio |

|

Total Interest Paid |

Based on the entire principal regardless of repayment progress |

Based on outstanding balance → decreases over time |

|

Predictability |

High → EMI remains constant throughout tenure |

Moderate → EMI may remain fixed, but the interest portion reduces over time |

|

Impact of Prepayment |

Prepayment may not significantly reduce interest (depends on lender rules) |

Prepayment reduces outstanding principal → lowers total interest substantially |

|

Common Loan Types in India |

Personal loans, car loans, and some small business loans |

Home loans, large personal loans, and education loans |

|

Transparency |

Can be misleading → actual borrowing cost higher than flat rate suggests |

Reflects the true cost of borrowing → easier to compare across lenders |

|

Best Suited For |

Short-term loans with simple repayment |

Long-term loans or higher principal amounts where interest savings matter |

Also Read: Applying for an Online Personal Loan in India

When a Flat Rate Loan Makes Sense for Indians

Not all flat rate loans are traps. In fact, under the right circumstances, they can actually be convenient and predictable. Here’s when a flat rate loan might work in your favour:

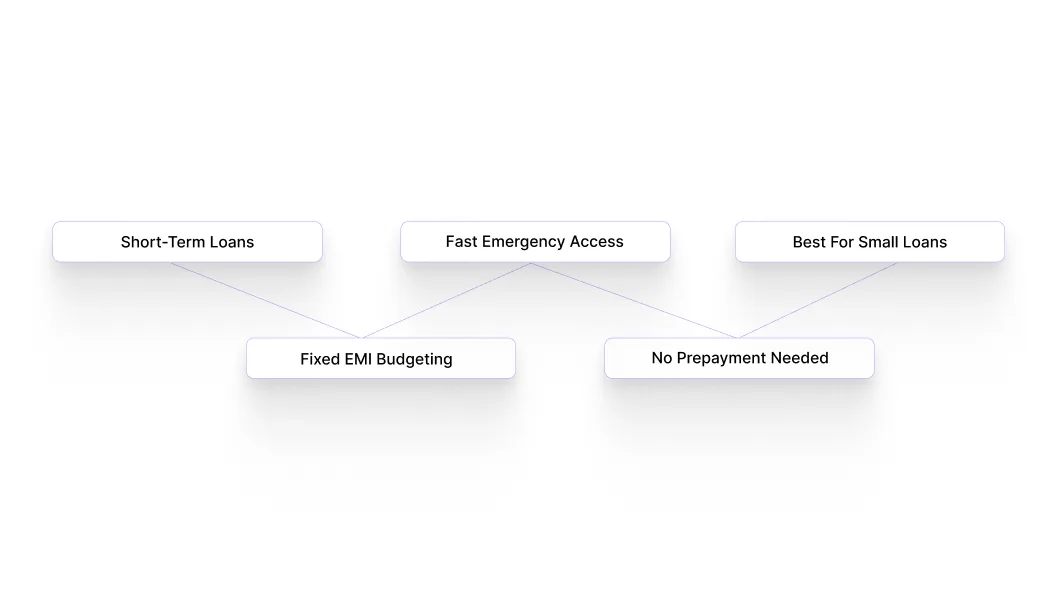

-

Short-Term Loans Are Easier to Manage: Flat rate loans work best for small loans with short tenures, like 12–24 months. The difference in interest compared to a reducing balance loan is minimal, so the convenience of fixed EMIs often outweighs the extra cost.

-

Fixed EMIs Help With Budgeting: Since your EMI stays the same from start to finish, you know exactly how much leaves your account each month. This makes household budgeting simpler and avoids surprises.

-

Quick Access During Emergencies: Flat rate loans are generally faster and easier to process. For urgent needs like medical bills, travel, or personal emergencies, fixed EMIs make repayment predictable and stress-free.

-

No Prepayment Planning Needed: If you don’t plan to prepay or partially repay early, flat rate loans are simple. Reducing balance loans save interest only when you prepay, so a flat rate can be more convenient for straightforward repayment.

-

Ideal for Small Vehicle or Consumer Loans: Auto loans, two-wheeler loans, or electronics loans often use flat rates. For smaller amounts and shorter tenures, the slightly higher interest is negligible, while approval and repayment remain easy.

Example: Suppose you take a 12-month personal loan of ₹50,000 at a flat rate of 12%. Your EMI is fixed at ₹4,666 every month. You don’t have to calculate reducing balance interest or worry about fluctuating EMIs. For a short-term, small loan like this, the convenience outweighs the slightly higher interest.

Make short-term cash gaps easy to manage. Pocketly gives ₹1,000–₹25,000 instantly, helping you pay on time. Apply in minutes and cover urgent payments without hassle.

When a Reducing Rate Loan Makes Sense for Indians

Reducing balance loans can save you a lot of interest, but they’re not always necessary. Knowing when they truly benefit you is key.

-

Long-Term Loans Benefit the Most: For big-ticket loans like home loans or large personal loans spanning several years, reducing the balance interest ensures you pay less overall. The longer the tenure, the bigger the interest savings compared to flat rate loans.

-

Early Prepayment Saves More: If you plan to prepay part of your loan or make extra EMIs, reducing the balance loans rewards you by lowering interest on the remaining principal. This flexibility isn’t available in flat rate loans.

-

Better for Large Loan Amounts: When borrowing ₹5 lakh or more, the difference between flat and reducing balance rates becomes significant. Choosing a reducing rate loan can save thousands or even lakhs over the loan tenure.

-

Interest Decreases As You Pay: Since interest is calculated on the outstanding principal, it reduces every month. This means your EMI gradually shifts more towards principal repayment, helping you build equity faster.

-

Smart Choice for Planned Borrowers: If you’re disciplined and want to minimise total interest, reducing-balance loans give you a clear advantage. They’re ideal for salaried professionals, small business owners, or anyone planning repayment carefully.

Example: Take a ₹10 lakh home loan at 10% reducing balance interest for 20 years. Early in the loan, interest dominates your EMI, but as principal reduces, interest payments fall. Compare this with a flat rate loan at 9%, where the total interest over 20 years would actually be higher despite the slightly lower rate.

Read More: Quick NBFC Personal Loans for People with Bad Credit Score in India

5 Misconceptions Indians Often Have About Flat and Reducing Interest Rates

Many borrowers assume flat interest rates are always worse and that reducing rates is always better. But here’s what lenders don’t often make obvious, and most borrowers miss:

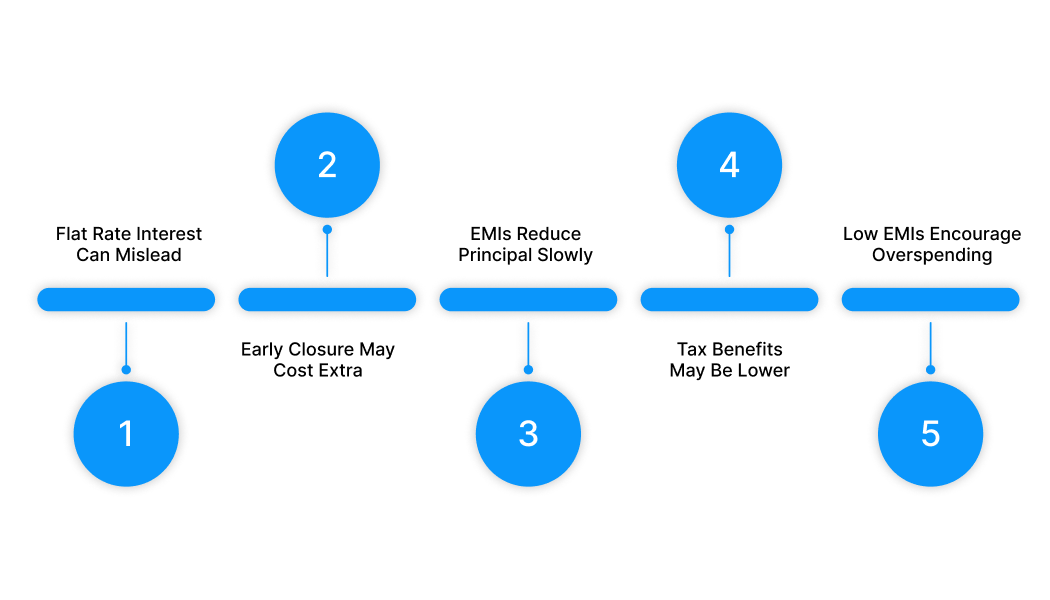

1. Flat Rate Numbers Can Be Tricky

Banks often show a flat interest rate because it makes your monthly payment look smaller. But here’s the catch: this number doesn’t show how interest really works over time. In flat rate loans, interest is calculated on the total loan amount for the full term, not on the reducing balance.

Example: You take a ₹10 lakh personal loan at 10% flat rate. It may look cheaper than a 9% reducing rate loan, but in the end, you could pay more in total because flat rate interest doesn’t go down as you pay off the loan. Always check the total interest payable before deciding.

2. Early Loan Payments Can Cost You

Many people think paying off a loan early saves money. With flat rate loans, some banks charge prepayment fees, which can reduce your savings.

Example: Paying off a ₹5 lakh flat-rate loan after a year may attract a 2–5% fee on the remaining loan. That’s ₹10,000–₹25,000 extra you could’ve avoided if you read the terms carefully.

3. Most Early Payments Are Interest, Not Loan

In a flat rate loan, your first few months’ EMIs mostly go towards interest, not the actual loan amount. That means your total debt doesn’t shrink much at the start.

Example: On a ₹10 lakh flat-rate home loan, after 6 months, your loan might barely go down. A reducing rate loan works differently; it reduces your loan faster, saving you interest in the long run.

4. Tax Benefits Can Be Smaller Than You Think

For home loans, tax benefits under Section 24 are calculated on the actual interest you pay using the reducing balance method, not the flat interest rate. Since flat rate loans calculate interest differently, the eligible tax deduction may be lower than expected. (Note: Personal loans don’t qualify for this tax deduction.)

Example: If you take a ₹10 lakh home loan at 10% flat rate, the interest calculated for tax purposes could be ₹80,000 instead of ₹90,000 under a reducing rate loan, reducing your tax benefit.

5. Small EMIs Can Make Spending Tempting

Flat rate loans feel cheaper because EMIs are smaller. This can trick people into spending more on non-essentials instead of paying off the loan faster.

Example: If your flat-rate EMI is ₹7,500, you might continue spending ₹5,000 on coffee, snacks, or online shopping. A reducing-rate EMI of ₹10,000 encourages you to budget carefully, which saves interest in the long run.

Short on Cash? How Pocketly Can Be Your Saviour

When you’re managing loans with flat or reducing interest rates, even small miscalculations can throw your monthly budget off balance. A sudden EMI, an unexpected bill, or a misaligned salary can create short-term cash gaps that make even a “planned” loan feel stressful.

This is where Pocketly comes in. It acts as a financial safety net, letting you bridge these gaps instantly so you never miss a payment, whether it’s a flat-rate EMI that feels heavy upfront or a reducing-rate loan with fluctuating interest components.

Here’s how Pocketly helps you stay in control:

-

Pay on time, every time: Avoid late fees or credit score hits, even during tight months.

-

Borrow smart, not more: Access ₹1,000–₹25,000 instantly, just enough to cover urgent expenses.

-

Lightning-fast digital access: Approval and direct bank transfer happen in minutes, no paperwork, no waiting.

-

No credit hurdles: No need for a strong credit history, collateral, or guarantor.

-

Flexible repayment: Pick a schedule that aligns with your income cycle.

-

Transparent, upfront costs: Interest starts at 2%/month; processing fees are 1%–8%, always clear.

-

Stress-free financial control: Cover urgent bills or EMIs without disturbing your planned savings or investments.

-

All-in-one app convenience: Apply, track, and repay, all from one simple app interface.

Think of Pocketly as your instant loan companion, especially useful for loans with fluctuating interest rates. Used wisely, it helps you handle urgent payments, maintain your credit health, and reduce financial anxiety, even when unexpected costs pop up.

Download Pocketly on iOS or Android and never let short-term cash gaps derail your loan or budget plans.

FAQs

1. What exactly is a flat interest rate?

A flat interest rate is calculated on the entire loan principal for the full tenure, regardless of how much you have repaid. This makes EMIs predictable every month, but the total interest ends up higher than a reducing rate loan because the outstanding principal is not considered while calculating interest.

2. How does it differ from a reducing or diminishing interest rate?

In a reducing rate loan, interest is charged only on the remaining principal, so your interest payments decrease over time. A flat rate loan keeps interest fixed on the original amount, which makes it simpler to understand but more expensive in total.

3. Which loans in India usually come with flat interest rates?

Flat rate loans are commonly used for short-term, small-ticket borrowing like personal loans, car loans, two-wheeler loans, and loans for consumer durables such as electronics or appliances. They are easy to manage for a few months or years, but are generally not ideal for long-term or high-value borrowing, like home loans.

4. How is EMI calculated for a flat interest rate loan?

The total interest is calculated upfront using the formula: principal × rate × tenure. This total interest is then added to the principal and divided by the number of months to get a fixed EMI. While simple, this can hide the true cost of borrowing, which is why comparing it with the reduced rate EMI is important before taking a loan.

5. Can prepayment save money on a flat rate loan?

Prepaying a flat rate loan usually doesn’t reduce the interest much because it is already calculated on the full principal. Some lenders may allow partial savings, but always check the prepayment terms first. Planning your loan tenure carefully can be more effective than relying on prepayment to save interest.

6. Is a flat rate loan suitable for everyone?

Flat rate loans work best for short-term or small-value borrowing due to their simplicity and predictable EMIs. For long-term or large loans, like home loans, reducing rate loans are usually cheaper and a smarter choice.

7. Are there hidden costs in flat rate loans?

Yes, processing fees, insurance add-ons, or late payment penalties can increase the overall cost. Since flat rates are calculated on the principal, they may mask the effective interest rate, which can be significantly higher than advertised. Always check the APR and additional charges before committing.

8. Should I choose a flat rate or reducing rate?

Flat rate loans offer simplicity and predictable EMIs, which are useful for short-term needs. Reducing the loan rate reduces the total interest and is better for long-term borrowing. In India, for car or personal loans under 3–5 years, flat rates are common, but for home loans or large personal loans, reducing rate loans save money in the long run.