Managing money wisely as a student can be one of the most important skills you’ll develop in college. In fact, with the right strategies in place, you can start building solid financial habits that will serve you well beyond college. Sometimes, the hardest part is simply getting started, especially when the demands of tuition, books, and living costs seem never-ending. But with the right tips and mindset, you can take control of your finances and make smarter decisions every day.

In this blog, we’ll share practical tips on how to manage money wisely as a student in 2025, helping you take control of your finances and set yourself up for success, without the stress.

Key Takeaways

- Create a Realistic Budget: Track all income sources and fixed expenses to avoid overspending; use apps to stay on top of your finances.

- Utilize Student Discounts: Leverage student-specific discounts and cashback offers on everyday purchases to reduce costs.

- Create an Emergency Fund: Set aside small amounts regularly to ensure you have a financial cushion for unexpected expenses.

- Minimize Credit Card Debt: Pay off balances in full each month to avoid interest charges and maintain a healthy credit score.

- Compounding Interest: Start saving early to benefit from compounding interest, turning small investments into substantial savings over time.

What is Money Management?

The term "money management" is a process of budgeting, saving, investing, and spending money in a way that allows individuals to meet their financial goals while maintaining control over their finances.

It involves creating a clear plan to track income and expenses, monitoring that resources are used efficiently to minimize debt and maximize savings. Effective money management allows individuals to build financial security, plan for the future, and avoid unnecessary financial stress.

Top 15 Money Management Tips for College Students

With tuition fees, rent, daily expenses, and social life costs, it’s easy to feel overwhelmed managing finances. But learning how to manage money wisely as a student can help you reduce debt and even save for long-term goals.

Let’s take a look at the top 15 practical money management tips for college students.

Create a Realistic Budget and Stick to It

Challenge: Many students face difficulty budgeting because their expenses are irregular and often tied to fluctuating income sources like part-time jobs or allowances.

Solution: The first step to managing money wisely as a student is creating a realistic budget. Start by listing all your income sources (part-time job, allowance, etc.) and fixed expenses (rent, groceries, tuition). Use a budgeting app like Mint to track your expenses daily and categorize them, so you can see exactly where your money is going.

Additional Tip: Use the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings. This helps students prioritize savings and ensure they aren’t overspending on non-essentials. You can also automate your savings to go directly into a separate savings account right after receiving funds.

Student Discounts and Rewards

Challenge: Students often feel the pressure of maintaining a social life while also managing financial commitments, leading to impulse purchases that derail their budgets.

Solution: Use student discounts and rewards programs wherever possible. Websites like Unidays provide access to discounts on everything from clothing to tech. Also, use cashback apps for online shopping or Groupon for local deals.

Additional Tip: Get a student credit card that offers cashback or rewards on everyday purchases like groceries and books. You should pay your credit card balance in full every month in order to avoid interest charges and improve your credit score.

Suppose you ever find yourself in need of quick cash for unplanned expenses. Then, Pocketly offers instant loans up to ₹25,000 with no hidden fees, flexible repayment options, and a completely digital application process.

Build an Emergency Fund, Even if It’s Small

Challenge: College students often prioritize immediate expenses and fail to save for unexpected situations like a sudden medical bill, an emergency trip home, or car repairs.

Solution: Start small by setting aside a portion of any income into a dedicated emergency fund. Even if you can only save ₹500 a month, over time it will add up. Make sure your savings are easily accessible but separate from your everyday spending accounts, perhaps using a high-yield savings account.

Additional Tip: For students with a tight budget, micro-savings apps can round up your purchases to the nearest rupee and save the difference automatically, helping you build an emergency fund without feeling it.

Minimize Credit Card Debt

Challenge: Many students are tempted to use credit cards to cover short-term expenses, which can lead to significant debt if not managed properly. The challenge is understanding how interest works and how it can quickly increase the debt.

Solution: If you have a credit card, use it responsibly. Pay off your balance in full every month to avoid interest charges. Set up automatic payments to make sure you never miss a payment. If you’re carrying a balance, prioritize paying off the card with the highest interest rate first.

Additional Tip: Build your credit score by using a credit card wisely. A good credit score will help you get lower interest rates on future loans. Avoid making late payments and keep your utilization rate below 30% to boost your score.

Track Your Spending and Identify Areas to Cut Back

Challenge: College life often comes with multiple social events, dining out, and spontaneous purchases that are hard to track, leading to unnecessary overspending.

Solution: Keep track of every penny. Use expense trackers like Expensify to categorize and monitor your spending habits. Regularly check if you’re sticking to your budget, and identify areas where you can cut back, whether it’s on food delivery, entertainment subscriptions, or clothes.

Additional Tip: Challenge yourself to avoid unnecessary spending for a month. A simple challenge like a “no-spend week” can help reset habits and encourage smarter financial choices. Use this time to cook at home more, explore free campus events, or limit online shopping.

Lower Campus Living Costs

Challenge: Campus living can be expensive, especially when you factor in transportation, health coverage, and technology needs. These expenses can add up and drain your budget.

Solution: Opt for campus shuttles, bicycles, or simply walking to get around, rather than relying on cars or taxis. For health coverage, take advantage of the affordable health plans offered by your university. If needed, compare these with private options to ensure you’re getting the best deal. When it comes to technology, instead of buying new gadgets, consider purchasing used devices or exploring student discounts available for essential electronics.

Additional Tip: Track your monthly campus living costs in an Excel sheet or app to spot areas where you can cut back and redirect those savings to more important goals.

Discover Types of Free Money

Challenge: In the process of worrying about how to manage money wisely as a student and miss out on opportunities for free money, such as scholarships or grants, due to a lack of awareness.

Solution: Research scholarships, grants, and fellowships available for your field of study. Use websites like Fastweb or Scholarships.com to find these opportunities. Be sure to check your school's financial aid office for additional local grants and awards.

Additional Tip: Keep an eye on local community programs or contests that offer cash prizes. Often, smaller scholarships are less competitive and easier to win.

Get Organized

Challenge: College students often struggle with keeping track of bills, important documents, and deadlines, leading to missed payments and unnecessary stress.

Solution: Invest in a simple accordion file or a small filing cabinet for important documents. Separate your documents into folders for school, bank, and service providers. Set reminders for any upcoming deadlines and payment due dates on your phone.

Additional Tip: Consider using digital tools like Google Calendar or a reminder app to stay on top of deadlines and manage bills efficiently.

Set SMART Financial Goals

Challenge: Daily expenses can easily distract you from long-term goals, like saving for healthcare, vacation, or building for any other emergency fund.

Solution: Set SMART goals (Specific, Measurable, Achievable, Relevant, Time-bound) for your finances. Write them down and incorporate them into your monthly spending plan. For example, “Save ₹5,000 by the end of the semester for emergencies.”

Additional Tip: Break larger financial goals into smaller monthly or weekly targets. Track your progress regularly and celebrate small victories to stay motivated.

Select Housing Mindfully

Challenge: Deciding where to live—on-campus or off-campus—can impact your finances significantly. It’s easy to overlook all associated costs.

Solution: When deciding where to live, carefully weigh the pros and cons of on-campus vs. off-campus housing. On-campus housing may include utilities and meals, but off-campus housing might offer more flexibility and potential savings. Compare all costs, including rent, utilities, and transportation.

Additional Tip: Consider sharing an apartment with roommates to split costs. Ensure that you factor in hidden costs like internet, groceries, and transportation when comparing your options.

Get the Lowdown on Student Loans

Challenge: Many students rush into taking loans without fully understanding the long-term impact of the interest they’ll be paying, leading to financial strain post-graduation.

Solution: Understand that when you take out a student loan, you're not only borrowing the principal amount but also the interest that compounds over time. Before taking any loan, always check the interest rates, repayment terms, and the potential total cost over time.

Additional Tip: For students seeking more affordable loan options, Pocketly offers low-interest personal loans starting at 2% per month, with instant approval. With Pocketly, you don’t have to worry about complex paperwork, and you get access to easy loan repayment modes without breaking the bank.

Earn Extra with a Part-Time Job

Challenge: While managing college expenses, it can be hard to make ends meet, especially when living on a tight budget.

Solution: Look for part-time jobs both on-campus and off-campus to boost your income. On-campus jobs often offer flexible hours that work around your class schedule, such as working at the library or in dining services. Off-campus jobs can provide extra income, but be mindful of your work-life balance.

Additional Tip: Explore roles that offer weekend availability or short shifts, so you can make time for your studies while still earning. Websites like Indeed or LinkedIn often list local student-friendly job opportunities.

Build a Good Credit History

Challenge: Students often underestimate the value of building credit early, which can impact their ability to secure loans or obtain favorable terms in the future.

Solution: Start by applying for a student credit card and make small purchases each month. Always pay on time to avoid penalties and build a positive credit history. A good credit score in the range of 300 to 850 is essential for future loans, such as car loans or mortgages.

Additional Tip: Use your credit responsibly, avoid maxing out your limit, and ensure timely payments. This will help you build a strong credit history, which is essential for managing larger financial responsibilities later in life.

The Power of Compounding Interest

Challenge: Many students struggle to understand how saving or investing early can have a significant impact due to compounding interest.

Solution: Compounding interest means that the money you earn in interest starts to earn interest itself. For example, if you invest ₹5,000 at 5% interest annually, you will earn ₹250 the first year. The next year, you’ll earn 5% on ₹5,250, making your interest ₹262.50. Over time, this exponential growth can significantly increase your savings.

Additional Tip: Open a high-yield savings account or start investing in mutual funds that offer compounding benefits. You will have more success with your money if you start earlier

Know How Credit Cards Work

Challenge: College students are often bombarded with credit card offers, leading to confusion and mistakes that can hurt their financial health.

Solution: Credit cards are a great tool when used responsibly. They help you build credit, but can also lead to debt if not managed carefully. Understand that credit cards have interest rates that apply if you don’t pay off your balance in full each month.

Additional Tip: Always pay your balance in full to avoid interest charges. If you’re new to credit cards, start with a low-limit card to ensure you don’t overuse it. Be sure to keep track of your spending and deadlines to avoid late fees.

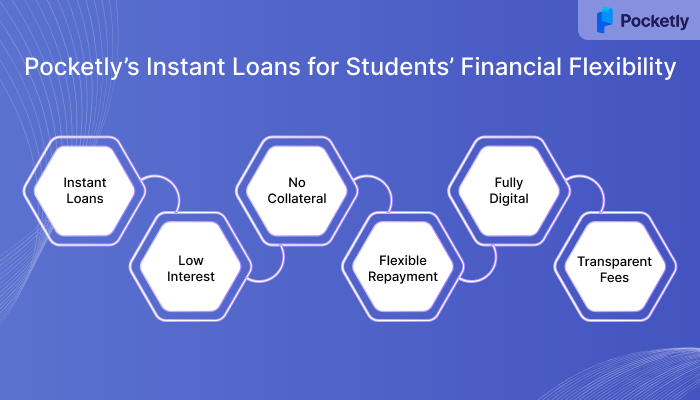

How Pocketly Provides Instant Personal Loans for Students' Financial Flexibility

Pocketly is a digital lending platform that provides instant, unsecured personal loans for students, offering an easy, hassle-free way to manage urgent financial needs. With no collateral required and a fully digital process, Pocketly helps students get quick access to funds without the stress of lengthy paperwork.

- Instant Loans: Borrow up to ₹25,000 with instant approval and no paperwork.

- Low Interest: Starting at 2% per month, with 1%-8% processing fees of the loan amount, it offers affordable repayment options.

- No Collateral: Get loans without the need for assets or security.

- Flexible Repayment: Choose repayment plans that fit your budget and timeline.

- Fully Digital: Apply, get approved, and receive funds directly in your bank account, all online.

- Transparent Fees: No hidden charges, ensuring clear and honest lending.

Conclusion

Effective money management is essential for students, and while it can be challenging, implementing the right strategies can make a significant difference. By budgeting wisely, utilizing discounts, building an emergency fund, and managing credit responsibly, you’ll set yourself up for financial success. Remember, it's all about making small, consistent choices that add up over time.

For those times when unexpected expenses arise, Pocketly offers instant personal loans. If you need quick financial support, download the Pocketly app on Android or iOS to get started today.

FAQs

1. How Much Money Does a College Student Need Per Month?

College student expenses can vary greatly depending on factors like location, lifestyle, and personal spending habits. On average, students may spend anywhere between ₹50,000 to ₹1,50,000 monthly, covering essentials like rent, groceries, transport, and leisure activities. It's important to create a budget that suits individual needs and helps control these costs.

2. What is the 7-Day Rule for Money Management?

The 7-Day Rule is a strategy to prevent impulsive spending. Before making a non-essential purchase, you wait for seven days. This pause allows you to reflect and decide whether the item is truly needed or just an impulse, encouraging smarter spending decisions.

3. What is the 80/20 Rule in Money Control?

The 80/20 Rule, also known as the Pareto Principle, asserts that 80% of your financial results come from 20% of your efforts. In terms of managing money, this means focusing on the key habits that make the most impact, like saving and budgeting, to see the biggest improvements in your financial health.

4. What is the Zero-Based Budget Method?

In zero-based budgeting, every rupee you earn is assigned a specific role, whether for expenses, savings, or debt repayment. This method ensures that at the end of the month, your income minus all expenses equals zero, ensuring that every penny is accounted for and used purposefully.

5. What is the Golden Rule of Money?

The golden rule of money management is simple: spend less than you earn. This fundamental approach helps individuals live within their means, avoid accumulating unnecessary debt, and save for future financial security, ensuring a solid foundation for long-term financial stability.