For many students, taking out a loan for higher education can seem like a challenging step, but it doesn’t have to be clouded by misconceptions. While student loans are often seen as a burden, the reality is much more straightforward than the myths suggest.

Misunderstandings about the terms, repayment options, and the long-term impact on your financial future can leave you feeling hesitant or misinformed. The truth is, student loans, when used wisely, can open doors to opportunities without the weight of confusion.

In this blog, we’ll separate fact from fiction, offering a clear perspective on what student loan myths are and how the actual things work, and also how they can fit into your educational journey.

Key Takeaways

- Student Loans Are Manageable: With flexible repayment terms and subsidized interest rates, student loans are easier to manage than many think.

- Loans Cover More Than Tuition: Education loans often cover books, living expenses, and travel, not just tuition.

- No Collateral Needed: Many loans don’t require collateral, especially for amounts up to ₹7.5 lakh.

- Good Grades Aren’t Mandatory: You don’t need top scores to get a loan; financial stability matters more.

- Moratorium Period Isn’t Interest-Free: Interest accrues during the moratorium, so plan for the total repayment amount.

Top 10 Common Myths and Facts About Student Loans

There are many myths surrounding student loans, which can lead to confusion and unnecessary anxiety. From misconceptions about interest rates to the eligibility criteria, it's important to separate fact from fiction. Let’s look at the top 10 myths and the facts that debunk them.

Myth 1: Student Loans Are Impossible to Pay Back

One of the most persistent myths about student loans is that they are impossible to pay off, leading many potential borrowers to believe they will be burdened with debt for decades. The concern often stems from the size of student loans, particularly for higher education, where loans can range from ₹1 lakh to ₹30 lakhs or more. With the average loan size increasing, especially at prestigious universities, this myth feels all too real for many students.

Fact: Although the loan amounts may seem substantial, loan repayment and modes are not as challenging as they are often portrayed. In India, government-backed education loans have a repayment period of 5 to 15 years, with the flexibility of lower interest rates, sometimes as low as 9%.

The actual repayment amount depends on your income after graduation, as there are income-driven repayment plans designed to make payments more manageable. Additionally, options like moratorium periods (the time between graduation and when repayments begin) give students time to secure employment before payments start.

For example, if a student graduates with a loan of ₹10 lakh at a 10% interest rate, their monthly payment could be around ₹10,000 to ₹12,000 for a 10-year loan term, which is totally manageable if the student secures a job with an entry-level salary of ₹3–5 lakh per annum.

Myth 2: Student Loans Have High Interest Rates That Will Always Keep Rising

Many students and parents believe that student loans come with high-interest rates that will continue to increase over time, leaving borrowers to face ever-growing debt. This misconception is often tied to the fear of private lenders charging high-interest rates compared to government loans, leading to the assumption that student loans are designed to trap borrowers in rising debt cycles.

Fact: While interest rates on private loans can be higher than those of government loans, most student loans in India, particularly those offered by government-backed schemes like SBI Student Loans or PNB’s Education Loan Scheme, come with low fixed interest rates.

For example, SBI offers education loans at rates ranging from 9.5% to 10%, which are lower than other types of consumer credit. Importantly, these rates are fixed for the duration of the loan, meaning they do not increase after disbursal.

Additionally, interest subsidy schemes exist for students from lower-income backgrounds. For example, under the Central Sector Interest Subsidy Scheme (CSIS), the government pays the interest on educational loans for students from economically weaker sections during the course period and for 1 year after graduation, easing the burden.

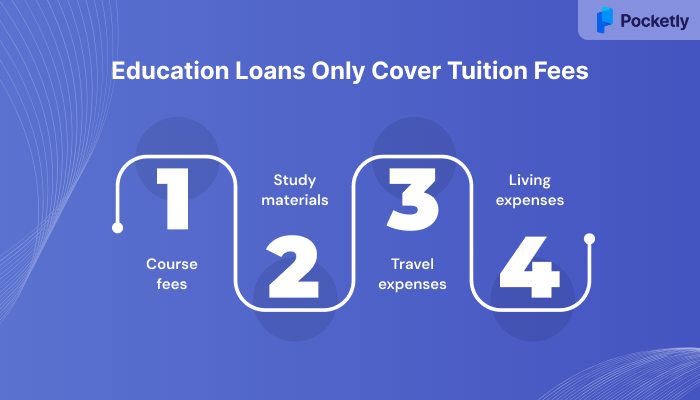

Myth 3: Education Loans Only Cover Tuition Fees

A common myth surrounding education loans is that they are exclusively for covering tuition fees, leaving students to cover other expenses, such as books, accommodation, travel, or living expenses. This misconception causes financial stress, as students believe they need to secure additional loans or funds for these ancillary costs.

Fact: Most education loans in India, especially those provided by public sector banks and financial institutions, cover not only tuition fees but also a variety of additional educational expenses. Under schemes like the SBI Student Loan Scheme or PNB Education Loans, eligible expenses include:

- Course fees (tuition, lab fees, exam fees, etc.)

- Books and study materials

- Travel expenses (for study abroad programs)

- Living expenses (accommodation, food, etc.)

For example, if you're studying abroad and your total expenses include ₹15 lakh for tuition and ₹5 lakh for living expenses, you can get a loan for the entire ₹20 lakh under most schemes.

Also Read: Applying for Instant Student Loan Online in India

Myth 4: Collateral is Required for Student Loans

Another prevalent myth is that student loans always require collateral, which deters many potential borrowers from applying for a loan in the first place. This leads to the misconception that securing a loan for higher education requires personal property or assets to be pledged as security.

Fact: While some student loans, especially for higher amounts or non-govt backed loans, may require collateral, this is not always the case. Most financial institutions offer collateral-free loans for students, particularly for those pursuing UG and PG courses at recognised institutions.

For example, the State Bank of India (SBI) offers collateral-free loans up to ₹50 lakh for Indian students enrolling in premier institutions. Banks usually look for the borrower to have a co-applicant (usually a parent) and ensure that the loan amount is within the permissible limit for unsecured loans.

Myth 5: Student Loans Are Only for Prestigious or Overseas Universities

A common misconception is that student loans are only available for studies at prestigious or international universities, leaving students at local or lesser-known institutions feeling excluded from accessing financial aid. This myth discourages students from pursuing education at universities that may be equally good but don’t have the same international recognition.

Fact: Student loans in India are available for a wide range of courses at various institutions, both within India and abroad. Financial institutions, including public sector banks like PNB, and private lenders, offer education loans for studies at accredited institutions, regardless of their ranking.

For example, if you're studying at a recognised college or university in India, you can still secure a loan for tuition, books, and living expenses. Even if the university isn't in the top 100 globally, as long as bodies like AICTE or UGC approve it, you're eligible for financial aid.

Myth 6: Only Students with Excellent Academics or Top Scores Can Get Loans

Many students believe they need exceptional academic performance or top scores to be eligible for an education loan. This myth stems from the idea that banks only approve loans for students attending top-tier universities or who have outstanding academic records. This belief can make students with average grades feel they don't have access to financial aid.

Fact: In reality, most student loan schemes do not have strict academic performance criteria for loan approval. Banks and financial institutions primarily focus on factors such as the course, institution, co-applicant's financial stability, and the student’s potential to repay the loan. While a good academic record may help show a student's seriousness about education, it is not a mandatory requirement for securing a loan.

For example, Bank of Baroda’s Educational Loan Scheme provides loans without requiring exceptional academic performance. While they may ask about the course or university you plan to attend, they are more concerned with your loan repayment capability, ensured through a co-signer (usually a parent or guardian).

Myth 7: Misconceptions About the Loan Application Process

One common myth that circulates among students is that the loan application process is long, complicated, and filled with excessive paperwork. Many believe that applying for a student loan involves hours at the bank, piles of documents, and a complicated approval process, leading to unnecessary stress and confusion.

Fact: The application process for most student loans has become much simpler and more streamlined in recent years. Banks like SBI and HDFC have digitized the loan application process, making it faster and more accessible. In many cases, online loan applications can be completed from the comfort of the student's home, saving both time and effort.

The documents required for most student loan applications are basic and usually include:

- Proof of identity (Aadhaar, passport, or voter ID)

- Proof of admission to an accredited institution

- Course fee structure

- Academic records or mark sheets (though excellent grades are not always a requirement)

- Income proof of the co-applicant (usually a parent or guardian)

The process usually involves an online application, followed by document submission and a quick verification. Many institutions offer Instant loan approval. Additionally, government-backed schemes like PMEAC provide students from economically weaker sections with lower interest rates, further simplifying the process.

Must Read: Instant ₹10000 Personal Loan for Students in India

Myth 8: You Need a High Credit Score or Existing Credit History to Qualify

It’s often believed that you need an excellent credit score or an existing credit history to qualify for a student loan, especially for young borrowers with no prior financial history. This myth causes many students to hesitate in applying for loans, fearing that their lack of credit history will be a barrier.

Fact: In India, student loans, especially those offered by government-backed schemes, do not require a credit score or an existing credit history. The primary focus is on the course of study, the institution, and the repayment capacity of the borrower, usually ensured through a co-applicant.

For example, Lenders like Bank of Baroda or Indian Bank do not consider the student’s credit score for loans up to ₹4 lakh, focusing instead on the financial standing of the co-applicant. Government schemes often offer subsidized interest rates for students from weaker financial backgrounds, where the creditworthiness of the co-applicant becomes the key factor.

Myth 9: It’s Better to Empty Family Savings Than Take a Student Loan

Many families believe it’s better to use personal savings for educational expenses rather than take on a student loan, thinking that student loans add unnecessary debt. This myth suggests that draining savings is a safer, debt-free option and avoids the burden of interest and repayments.

Fact: While using family savings may seem like a short-term solution, it can be detrimental to your long-term financial security. Family savings are reserved for unexpected expenses; depleting these savings for education can leave families financially vulnerable, especially in emergencies.

Student loans, on the other hand, come with several benefits that using savings doesn’t provide. For example, education loans from Indian banks like SBI, PNB, or HDFC have low-interest rates ranging from 9% to 11%, lesser than the interest rates on cards or personal loans.

Additionally, interest subsidies are available under schemes like CSIS for students from lower-income backgrounds, which means the government will pay the interest during your course and for one year after graduation.

Also Read: Top 30 Instant Loan Apps for Students in India

Myth 10: Moratorium Period is Interest-Free

A common misconception about education loans is that the moratorium period—the time between receiving the loan and starting repayments- is interest-free. Many borrowers believe that during this period, they are not liable for any interest charges, which makes the loan seem less burdensome initially.

Fact: The moratorium period is provided to give students time to complete their studies and find a job before they begin repaying the loan. However, this period is not interest-free in most cases. Interest on the loan starts accumulating from the day the loan is disbursed, even during the moratorium period. The only difference is that repayments do not begin until the moratorium ends.

For example, if you take out a loan for ₹10 lakh with an interest rate of 10% per annum, interest will accumulate during the moratorium, which may last anywhere from 6 months to 1 year after your course finishes. This means that when repayments begin, you’ll be required to pay the principal amount plus the interest that accumulated during the moratorium period.

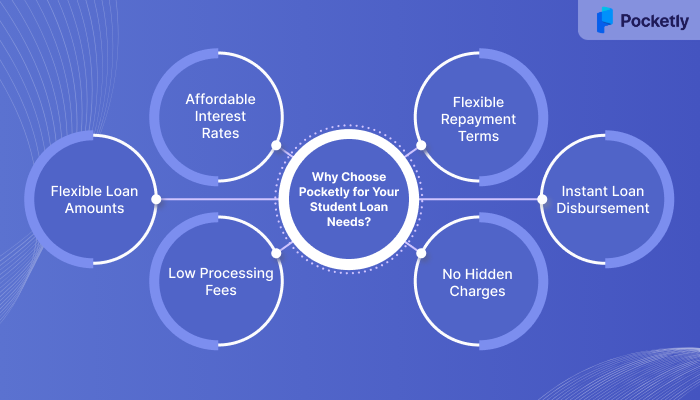

Why Choose Pocketly for Your Student Loan Needs?

Pocketly is a digital lending platform designed to help young adults manage their financial needs, especially when it comes to education and personal expenses. With a focus on speed and transparency, Pocketly offers self-employed loans, salaried loans, catering to students and entrepreneurs.

Here’s why Pocketly could be the right choice for your education loan:

- Affordable Interest Rates: Starting at just 2% per month, making borrowing more manageable.

- Flexible Loan Amounts: Loans ranging from ₹1,000 to ₹25,000 to suit your financial needs.

- Low Processing Fees: Processing fees between 1%-8%, keeping costs transparent.

- Flexible Repayment Terms: Convenient repayment options with flexible EMIs.

- Instant Loan Disbursement: Quick loan approval and funds transferred directly to your account.

- No Hidden Charges: No annual fees, joining fees, or surprise charges.

Conclusion

In conclusion, student loans are often misunderstood, with many myths clouding the real benefits they offer. From misconceptions about high interest rates to fears about complicated application processes, the reality is far simpler than expected. When managed well, student loans can provide financial flexibility, help pay for a wide range of educational expenses, and set students up for a solid financial future.

If you're looking to manage your educational expenses without the confusion, Pocketly offers an easy, transparent lending option with low interest rates, no hidden charges, and flexible repayment terms. Download Pocketly now on iOS or Android to get instant access to funds with flexible EMIs and clear terms.

FAQs

1. What are the social issues of student loans?

Student loans contribute to financial inequality, especially for lower-income students who struggle to repay loans after graduation. High debt levels can delay homeownership, savings, and career progress, leading to long-term economic stress.

2. How to best handle student loans?

To manage student loans effectively, focus on making timely payments, keeping your debt-to-income ratio low, and exploring options like income-driven repayment plans or refinancing for better rates. Regularly review your financial situation and adjust your budget accordingly.

3. Which gender has the highest student loan debt?

In many countries, women tend to have more student loan debt than men, mainly due to higher borrowing amounts for graduate programs and lower average salaries upon entering the workforce. This gender gap in debt is a growing issue.

4. What is the largest source of student loans?

In the U.S., federal student loans are the largest source, providing the majority of student loans through programs like Direct Subsidized and Unsubsidized Loans. In India, public sector banks and government schemes are the primary sources.

5. What is the smartest way to pay off student loans?

The smartest approach is to prioritize loans with higher interest rates first while making minimum payments on others. Consider consolidating or refinancing your loans for lower interest rates, and explore automatic payments to reduce your overall debt faster.